BSTR Holdings, the bitcoin treasury company led by Blockstream co-founder Adam Back, will not complete its merger with special purpose acquisition company Cantor Equity Partners I under the original deal terms. The PIPE financing tied to the transaction is also no longer required to close.

In an 8-K filed with the U.S. Securities and Exchange Commission on July 8, Cantor Equity Partners I, which trades on Nasdaq under the ticker CEPO, said it is discussing a revised transaction structure and terms with BSTR Holdings to better reflect current market conditions. The filing states that the parties will not consummate the deal under the merger agreement signed on July 16, 2025.

A company announcement released the same day added two more changes: the shareholder meeting scheduled for July 10 has been postponed indefinitely, and public shares that had submitted redemption requests will be returned and not redeemed.

Original structure called for 30,021 BTC at listing

According to a company release filed with the SEC in July 2025, BSTR had expected to go public with 30,021 BTC on its balance sheet. The original package also included up to $1.5 billion in fiat PIPE financing, a 5,021 BTC in-kind PIPE, 25,000 BTC from founding shareholders, and up to about $200 million in cash from Cantor Equity Partners I, depending on shareholder redemptions.

More detailed merger documents broke the 30,021 BTC figure into three parts: 25,000 BTC contributed by the seller, 4,156.11 BTC from the CEPO bitcoin equity PIPE, and 865 BTC from the Newco equity PIPE. The structure also included cash equity, convertible notes, preferred stock, and bitcoin-denominated subscription commitments, all contingent on the transaction closing.

Back is serving as BSTR’s chief executive officer. The deal was framed around “bitcoin per share,” not simply passive bitcoin ownership.

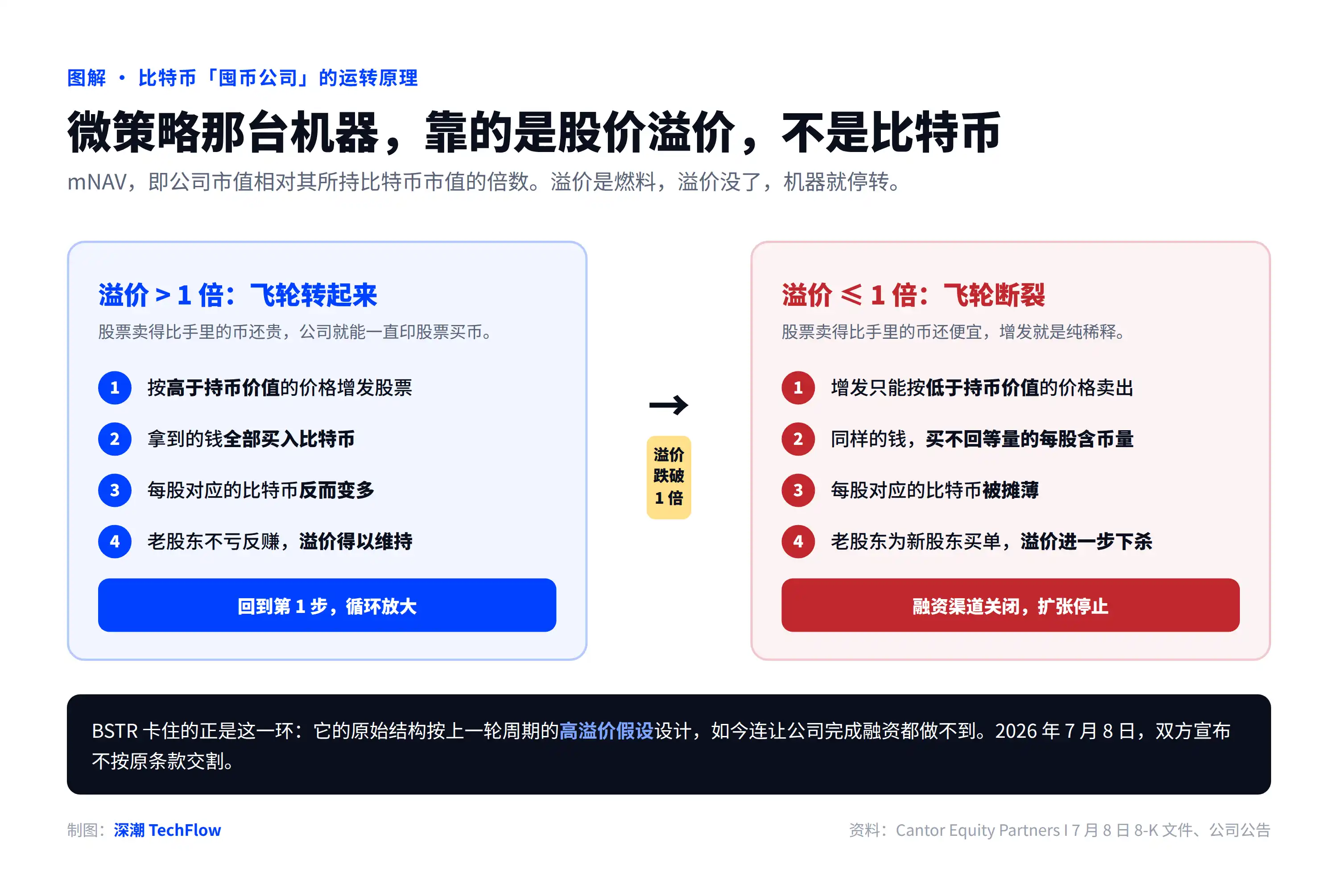

The stress point is the financing model

The report argues that the bitcoin treasury company model depends on something different from bitcoin’s spot price alone. A key metric is mNAV, the multiple of a company’s equity market value relative to the market value of the bitcoin it holds. If a company is valued at twice the worth of its bitcoin holdings, its mNAV is 2.

That premium is what allows the model to run. A company can issue stock above net asset value, use the proceeds to buy more bitcoin, and still increase bitcoin per share. Strategy, formerly MicroStrategy, is cited as the best-known example of that cycle.

Once the premium compresses to 1x or falls below it, the loop breaks. New share issuance no longer adds to bitcoin per share and can instead dilute existing holders. In BSTR’s case, the problem is that the original structure was built on valuation assumptions from the prior cycle, and investors are no longer willing to fund it on those terms.

Pressure is showing across the sector

As of July 12, bitcoin was trading around $64,000, with a market capitalization of about $1.27 trillion and roughly 58% share of the crypto market, according to the report. That price was down about 49% from the record high of $126,200 set on Oct. 6 last year, and down about 19.5% over the past 60 days.

The report points to several other developments from the same week. American Bitcoin, which involves Eric Trump, carried out a 1-for-15 reverse stock split to maintain Nasdaq’s minimum share price requirement and holds about 8,000 BTC. Strategy’s preferred shares briefly traded below par in June. Metaplanet’s share price has fallen below the value of its bitcoin holdings. Earlier in July, another U.S. bitcoin treasury company sold all of its bitcoin under debt pressure and Nasdaq compliance pressure.

At the same time, capital has been moving elsewhere. AI computing company CoreWeave recently completed a $20 billion financing round.

Next SEC filing is the key document

Cantor and BSTR are still negotiating, but the original terms are no longer in force. If the two sides reach a new agreement, a new SEC filing would revise or supplement the registration statement and proxy materials.

That filing is expected to show three things: how much of the 30,021 BTC scale remains, how much of the original PIPE commitments survive, and what price investors now require to put in fresh money.

According to market data cited by TFTC, CEPO shares are trading near $10.5, close to trust value. The report treats that as a sign that the market is assigning no meaningful premium to the transaction.

The July 8 filing also listed risks that are likely to shape the talks ahead: shareholder redemptions, public float, liquidity, exchange listing, bitcoin price volatility, competition, regulatory uncertainty, and the difficulty of expanding bitcoin accumulation and treasury operations.

For investors in bitcoin treasury stocks, the revised terms will show whether the model can still function in a low-premium market. If the new agreement preserves a treasury close to 30,000 BTC, keeps meaningful investor commitments, and avoids pushing a large share of the cost onto new shareholders, the structure may still be repriced rather than abandoned. If the deal comes back with a smaller bitcoin position, higher funding costs, weaker investor protections, or heavier reliance on dilution, that would point to a very different setup for the next wave of treasury companies.