Crypto venture capital deployed $13.3 billion in the first half of 2026, but it did so across only 435 deals. A report by Tiger Research and RootData, covering 9,416 investment transactions recorded from 2018 through H1 2026, says the market has not returned to broad-based expansion. Instead, money is being concentrated into a far smaller set of companies.

According to the report, written by Tiger Research Reports and translated by TechFlow, funding volume in H1 2026 nearly matched the $13.2 billion recorded in all of 2024. Deal count, however, dropped 78% from the 2022 peak of 1,978. The report says the old “spray-and-pray” approach built around token generation event timing and tokenomics has stopped working, while projects with mature business models, auditable revenue structures, and regulatory licenses are drawing the capital.

The 2021 playbook was speed first

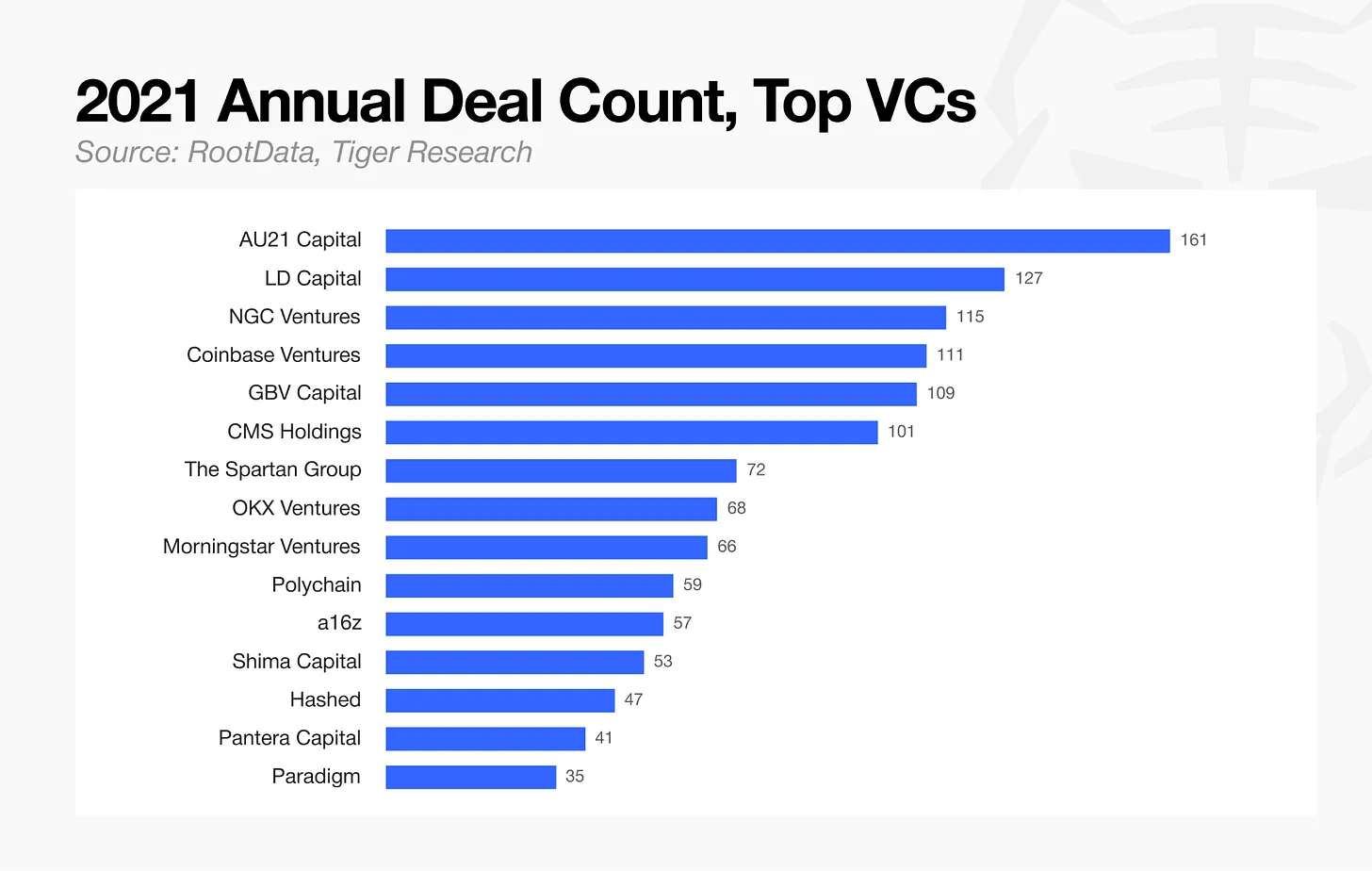

The report uses 2021 as a contrast point. That year, speed and diversification sat at the center of crypto investing. Investors completed 1,750 deals, including seed rounds, and firms competed on how quickly they could get into a round. AU21 Capital alone averaged more than 13 deals a month.

At the time, investment decisions were often reduced to relatively simple benchmarks such as TGE schedules and tokenomics. Because token issuance alone could generate returns without much real product development, many venture firms spread money across dozens or even hundreds of projects regardless of valuation. Thorough diligence mattered less than fast execution. New rounds closed almost instantly, and firms that missed one round often chased the next at a higher valuation. The report describes that pattern as a recurring FOMO cycle across the industry.

Many of the firms that followed that approach did not survive the bear market that followed. Those that did survive changed strategy in a fundamental way, the report says.

Which VCs stayed active

Lead investing remains concentrated among larger firms

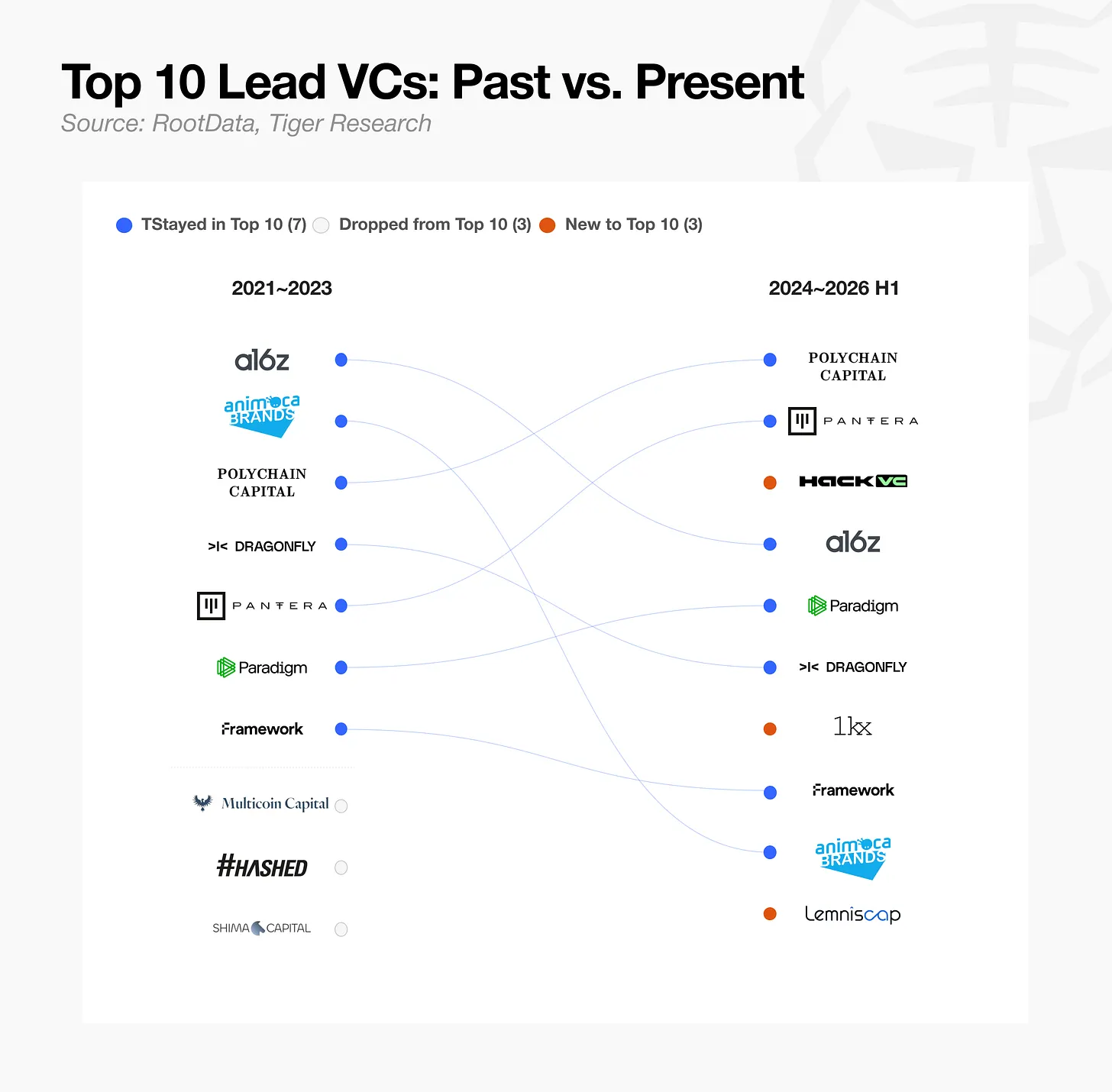

The report treats lead investing as a key measure of resilience. Because leading rounds has long required reputation, capital scale, and the ability to organize major financings, firms that historically led major rounds have generally remained active and still dominate top rankings. Some others have disappeared or only reappeared recently.

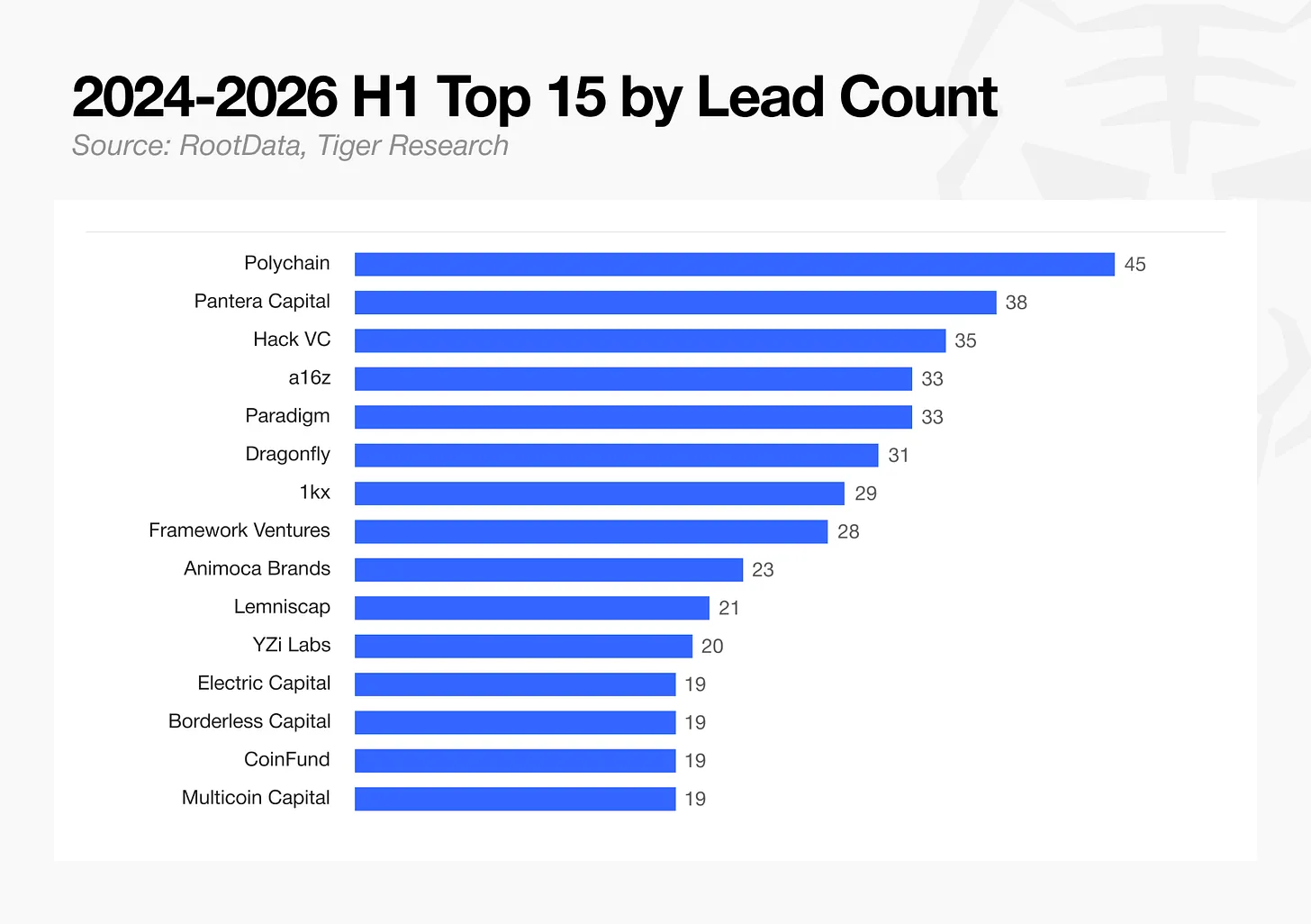

Looking at data from 2024 through H1 2026, crypto-native venture firms and established large institutions are concentrating resources on lead roles and going deeper into each deal. They are doing fewer transactions overall, raising diligence standards, and seeking board seats and greater governance influence. The shift is away from investing first and sorting details later.

Exchange-backed investors dominate by participation count

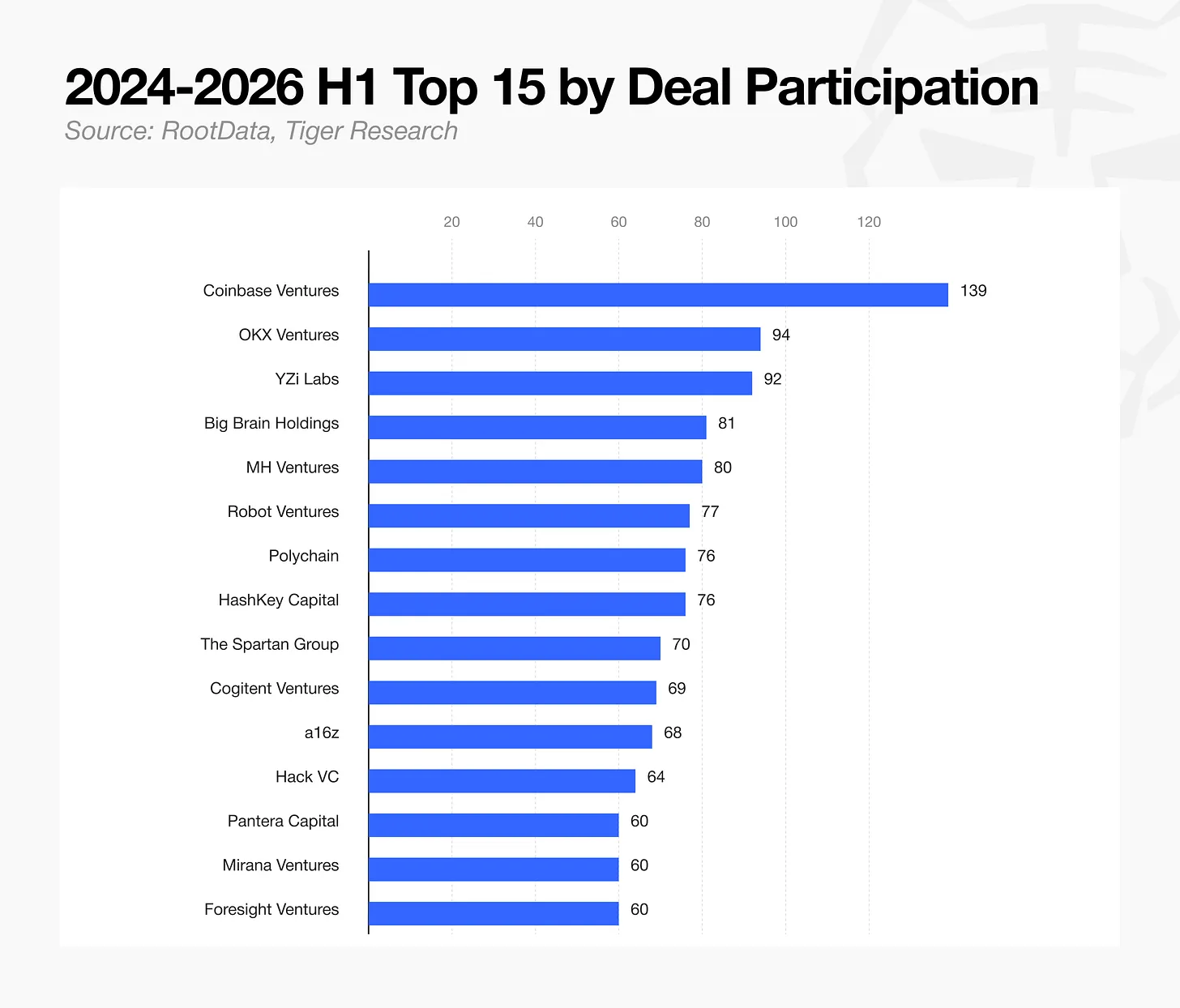

The picture changes when the metric shifts from lead rounds to total participation count. Among the top 15 venture firms ranked by participation from 2024 through H1 2026, exchange-linked investors make up a large share. Coinbase Ventures ranked first with 140 deals, OKX Ventures was second with 94, and YZi Labs was third with 92.

The report notes that YZi Labs is the organization formerly known as Binance Labs, renamed in January 2025. HashKey Capital, ranked seventh, is the venture arm of Hong Kong exchange HashKey Exchange. Mirana Ventures, ranked fourteenth, is the venture arm of Bybit. Five major exchanges appeared in the top 15 through their investment units alone.

By contrast, large firms focused on lead investing, including Polychain and Pantera Capital, ranked lower on overall participation count. The report says exchange-backed investors have carved out a strong position in non-lead participation because they can offer liquidity and marketing support through their platforms.

Mid-sized venture firms without a clear defensive edge are being pushed out quickly. In the report’s framing, they lack economies of scale, brand recognition, or exchange-level liquidity support, while also facing capital pressure and failed exits.

The exit of spray-and-pray investors

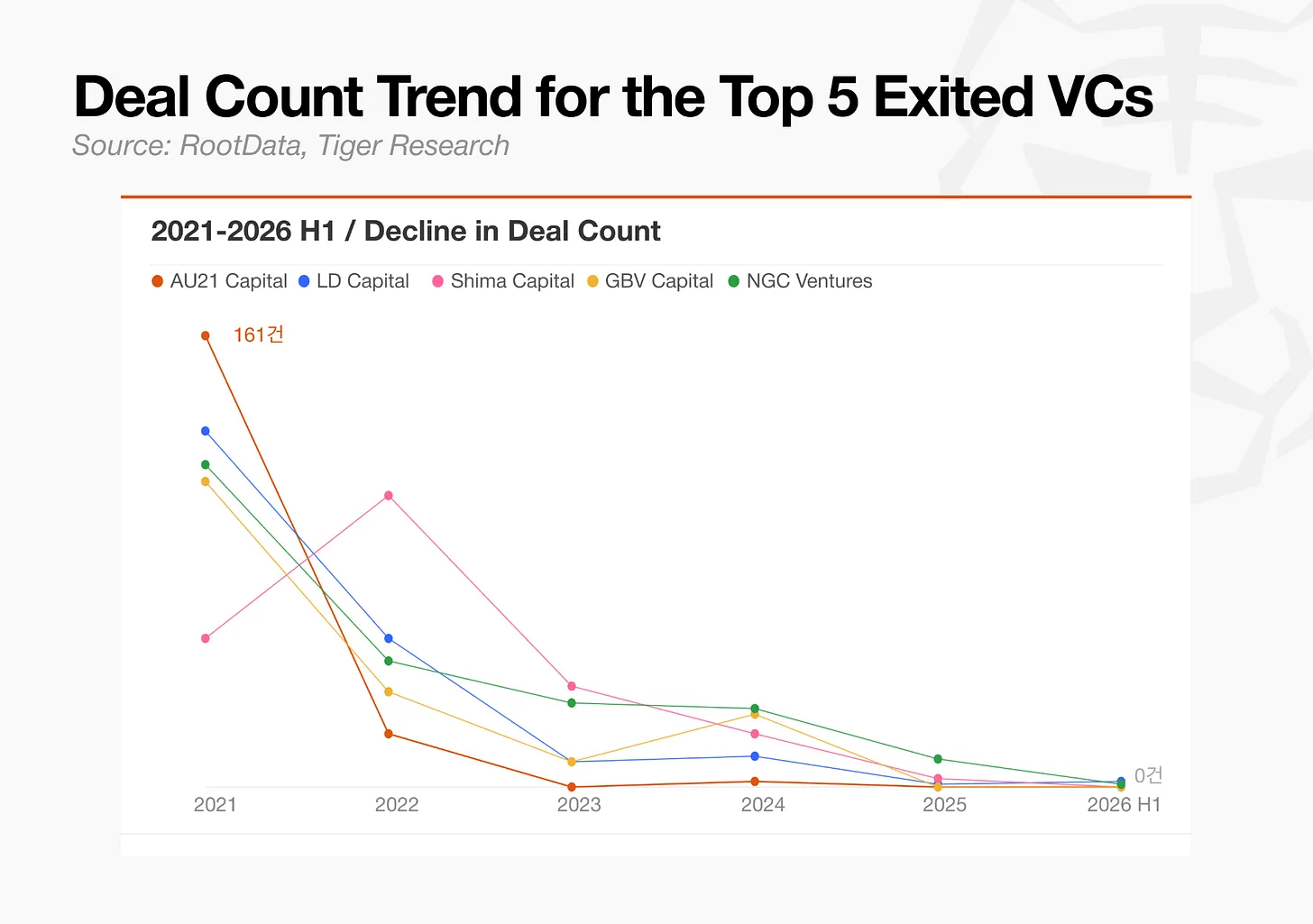

The report specifically points to AU21 Capital, LD Capital, and Shima Capital, saying their deal counts dropped by as much as 98.9%, effectively stripping them of influence in the market. Once the sector entered a prolonged bear phase and tighter regulation, strategies built on short-term narratives and quick token monetization stopped delivering, according to the report.

One reason was the lack of real differentiation. Another was that capital itself had moved on, toward projects that had already reached a higher level of maturity. In that environment, there were simply fewer new early-stage companies looking for seed money. The opportunity set those firms relied on had largely disappeared.

Funding rounds shifted toward later stages

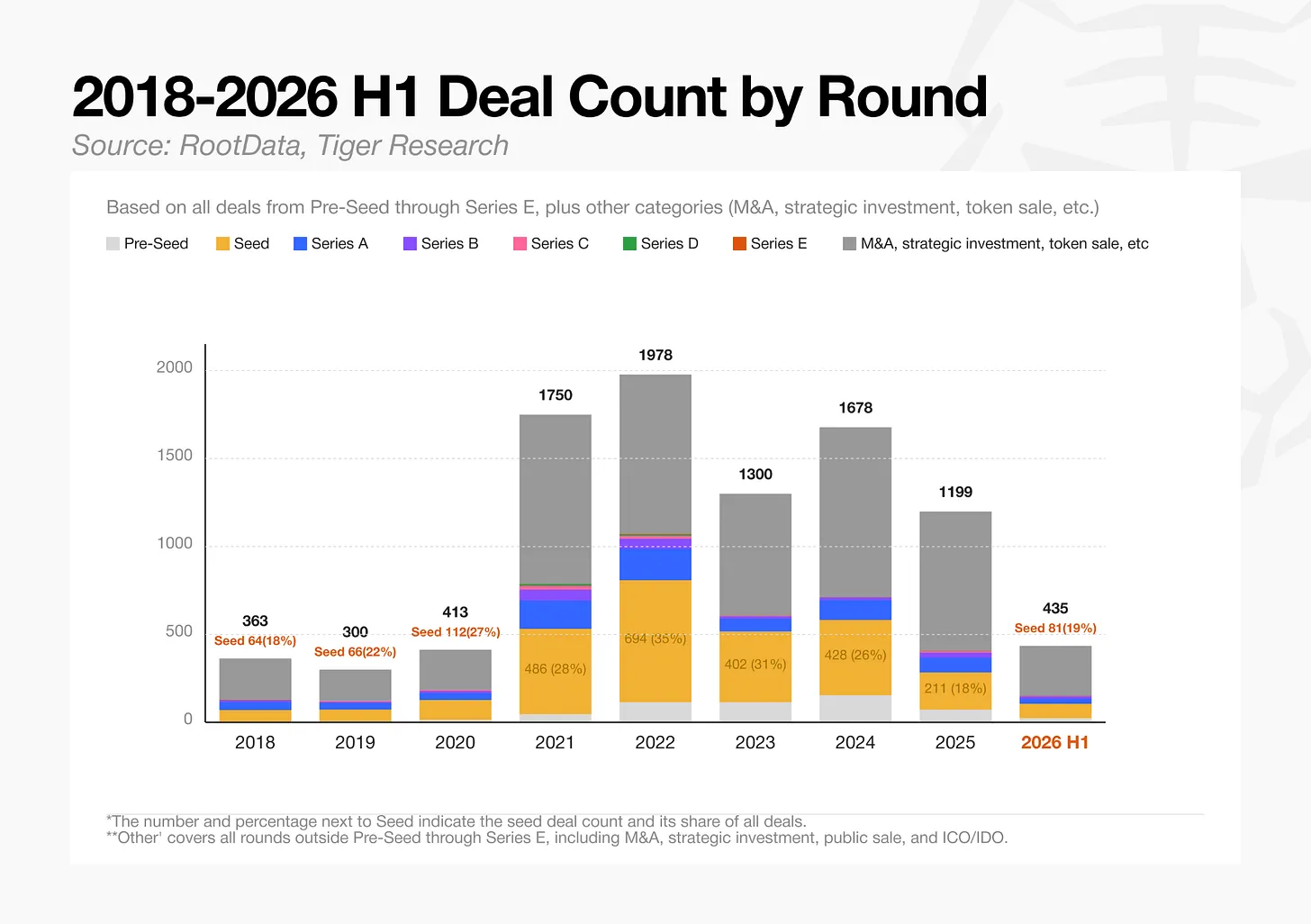

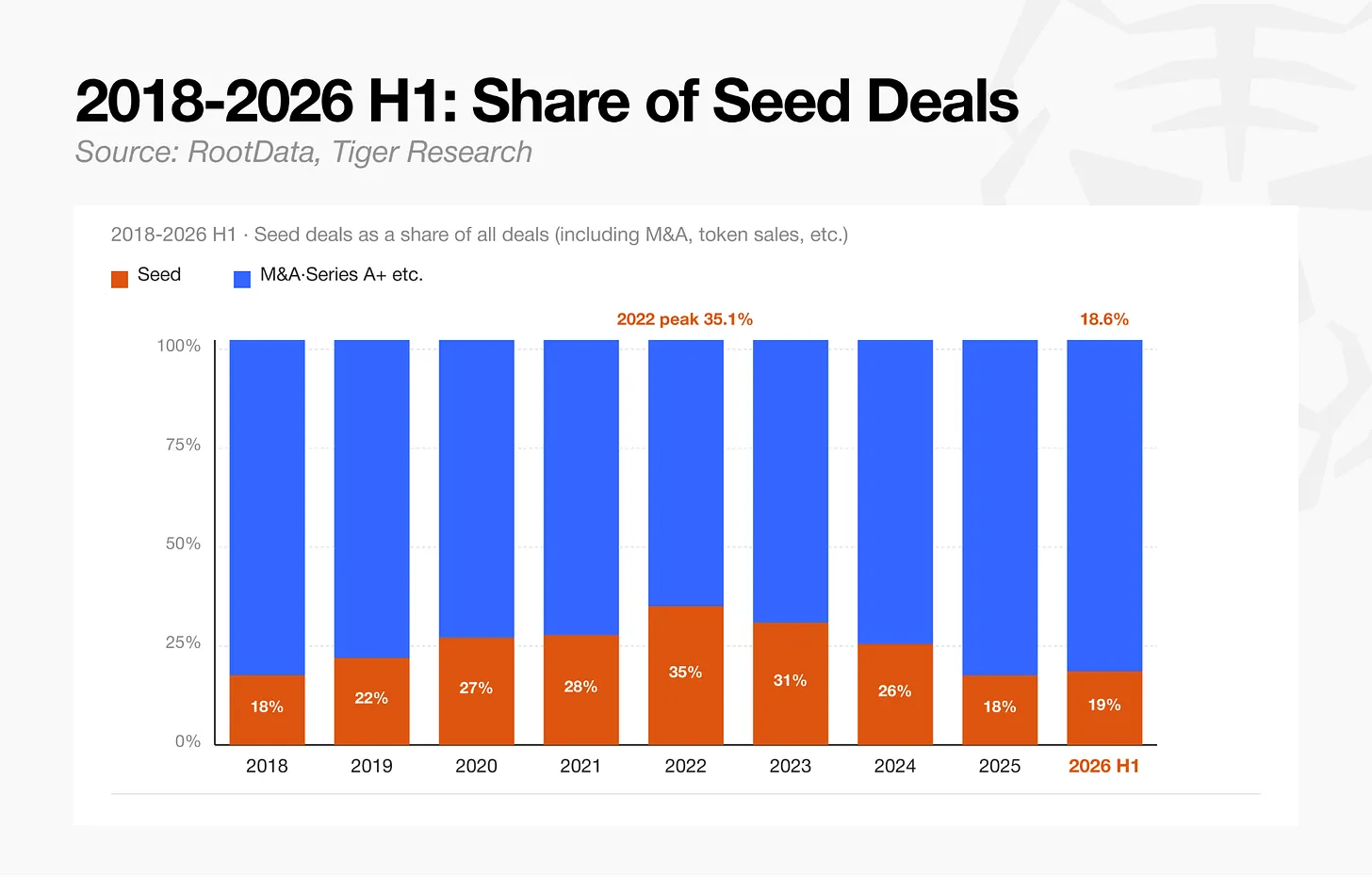

Seed activity fell sharply

In H1 2026, seed-stage transactions totaled 81, down 88% from 694 in 2022. Seed’s share of all deals fell from 35.3% in 2022 to 18.7% in H1 2026. The report reads this as a sign both of investor aversion toward unproven business models and of a smaller pipeline of new projects seeking seed financing.

In other words, the collapse in seed volume reflects both market contraction and market maturity.

Series A and later rounds now take 75.2% of capital

Measured by capital allocation, Series A and later rounds now account for 75.2% of total investment. Seed funding briefly held the majority share during the 2023 bear market, but once the market recovered, capital quickly rotated back into better-capitalized companies.

In H1 2026, total Series A funding reached $745 million, exceeding the $423 million raised by all seed-stage companies combined and making Series A the largest category by round type. The report also gives average deal sizes by stage: $5.4 million for seed, $22.4 million for Series A, $127 million for Series C, and $202 million for Series E. Later-stage sample sizes are smaller, but companies reaching those stages tend to carry higher revenue and valuation, so each round is correspondingly larger.

More capital, fewer transactions

Capital and deal count moved in opposite directions

Total capital inflow reached $13.3 billion in H1 2026, while the 435 recorded deals represented just 22% of the 1,978 deals logged in 2022, the peak year by annual deal count. From 2024 to 2026, capital stayed flat or rose even as it concentrated into fewer transactions.

The report attributes that divergence to a change in the mix of capital. Small, diversified bets aimed at token liquidity events have declined, while large direct checks from traditional financial institutions have increased. Those institutions are not centered on token listing schedules or narrative momentum. They are evaluating whether a company has auditable revenue and the regulatory licenses needed to operate.

There were 32 deals of $100 million or more in H1 2026, accounting for 7.4% of all transactions, up from 1.1% in 2024. Over the same period, average deal size rose from $11.7 million in 2024 to $47.4 million in H1 2026. The report says that concentration is being driven from both directions: more large deals are being done, and many smaller deals, especially seed financings, are disappearing.

Traditional financial institutions joined 54.5% of transactions

The share of investment transactions involving traditional financial institutions rose from 29.2% in 2018 to 54.5% in H1 2026. The ratio first moved above half in 2021 at 53.9%, fell to 45.2% in 2023, rebounded to 54.4% in 2024, slipped to 50.9% in 2025, and returned to 54.5% in the first half of 2026. Since first crossing the majority threshold in 2021, participation has remained near that level.

The report gives Digital Asset, the developer of Canton Network, as an example. Its $355 million round was led by a16z, but core participants included BNP Paribas, HSBC, S&P Global, and Hanwha Investment & Securities. Those institutions invested directly rather than through venture subsidiaries.

The conclusion drawn in the report is that capital is moving toward companies that have already reached a certain level of maturity rather than staying concentrated at the earliest stages.

Sector rotation favored institution-facing categories

The report uses 2024 as the baseline year for sector comparison, describing it as the point when spot Bitcoin ETF approval and a more favorable regulatory environment produced the first clear sector-level capital flows since the bear market.

In 2024, infrastructure took the majority of invested capital at 50.9%. By H1 2026, that share had fallen to 14.8%. Payments and stablecoins moved into the lead at 25.3%, followed by centralized exchanges at 18.2% and prediction markets at 17.5%.

In the report’s view, that change shows that blockchain infrastructure has shifted from being a stand-alone investment target to functioning as a practical platform for institutional business. It cites Robinhood running its own layer on Arbitrum and Securitize using Solana and Avalanche as settlement layers around its New York Stock Exchange listing. The market’s core demand, the report says, has moved from building fresh protocol infrastructure from scratch to operating real-world financial services on top of existing infrastructure.

Gaming, NFTs, and social fell back hard

The report identifies gaming, NFTs, and social and entertainment as the clearest laggards. Deal counts fell from 141 to 5 in gaming, from 27 to 2 in NFTs, and from 74 to 11 in social and entertainment between 2024 and H1 2026.

Capital raised fell along the same path. Gaming declined from $758.6 million to $44.8 million, NFTs from $114.9 million to $14.7 million, and social and entertainment from $512.1 million to $70.1 million.

Gaming saw the sharpest drop of the three. The report says early GameFi models tied gameplay to token rewards and often depended too heavily on token issuance for financial return rather than sustainable gameplay. Once new user growth slowed, token price declines and user losses reinforced one another in what the report calls a death spiral. In that setting, traffic metrics stopped serving as reliable diligence indicators, and capital flow to the category was effectively cut off.

DeFi became smaller and more concentrated

In decentralized finance, deal count fell 71%, but total investment was down only about 34%. Average deal size actually increased from $4.5 million in 2024 to $10.4 million in H1 2026, suggesting that as the overall market shrank, money concentrated into a smaller number of larger rounds.

The report says much of that concentration came from lending protocol Morpho’s token sale to institutions and investment firms. Morpho, which uses its modular lending protocol to open the DeFi vault market to institutions, raised $175 million on June 9, 2026, in a token round led by a16z crypto, Paradigm, and Ribbit Capital. That one financing accounted for 17.7% of all DeFi investment in H1 2026.

The takeaway in the report is that DeFi capital has moved away from broad ecosystem expansion and toward a handful of protocols that the market has already validated.

Payments and stablecoins posted the fastest growth

Payments and stablecoins continued to accelerate on a monthly basis. Total investment surged from $143.9 million to $2.85 billion in H1 2026. The report adds that the rise was driven in large part by a small number of major M&A transactions.

The biggest deal in the category in H1 2026 was Mastercard’s $1.8 billion acquisition of BVNK in March. The second largest was Payward, Kraken’s parent company, acquiring Reap for $600 million in May. Those two deals alone made up about 84% of the sector’s total investment in the first half.

Cross-border payments and crypto card issuers also kept raising money, including Rain at $250 million and KAST at $80 million. The report says those financings helped support the sector’s expansion.

Stripe is presented as one of the clearest examples of the competition to define stablecoin standards. The sequence began with its October 2024 acquisition of Bridge. After that deal, Stripe partnered with Paradigm to build Tempo, a blockchain dedicated to stablecoin payments, and launched its mainnet successfully in March 2026. In June 2026, Bridge co-founder Zach Abrams became interim head of the entity operating Open USD, or OUSD, a global alliance stablecoin project involving more than 140 participating companies.

According to the report, OUSD has adopted Bridge, which Stripe acquired and continued developing, along with Tempo, which Stripe is building, as its core initial infrastructure. The report argues that competition in stablecoin infrastructure has moved beyond company-level acquisitions and into a race to define global standards for the broader market.

CEX investment was largely about consolidation

Centralized exchanges increased their share of total investment from 3.0% in 2024 to 18.2% in H1 2026. The report says that should not be read simply as traditional venture capital expanding into new exchange startups, because M&A alone accounted for 75.5% of all CEX investment recorded from 2024 through H1 2026.

That share rose from 58.8% in 2024 to 78.9% in 2025, showing how concentrated the category became. Total capital inflow was below the prior year’s $19.4 billion peak created by large M&A deals, but it still stood at more than six times the 2024 level of $340 million. Deal count did not slow. H1 2026 logged 23 transactions, or 3.8 per month, above the 2.8 monthly pace in 2024 and 3.0 in 2025.

The report says what the market is showing is a reshuffling around a small number of large operators. The largest announced transaction in the period was Naver’s acquisition of a stake in Dunamu, which remains under regulatory review. It was followed by Coinbase’s $2.9 billion purchase of Deribit and Kraken’s $1.5 billion acquisition of NinjaTrader.

MGX, the Abu Dhabi sovereign wealth fund, also fits the same pattern through its $2 billion strategic investment in Binance. At the same time, venture arms tied to major exchanges, including OKX Ventures and HashKey Capital, have become more active in both funding rounds and acquisitions. In the report’s reading, CEX participants are increasingly acting in two roles at once: investment targets and strategic investors.

Prediction markets drew repeat megachecks

Prediction markets emerged as a distinct growth area. The report says the sector provides liquidity around real-world macro indicators such as economic data, elections, and policy decisions, and that its expansion was triggered by formal approval from the Commodity Futures Trading Commission in May 2025. That regulatory step, it says, opened the door to large-scale capital inflows from hedge funds and asset managers.

Kalshi’s cumulative trading volume surpassed $100 billion in June 2026. The company had already raised $1 billion in December 2025 in a round led by Paradigm, then raised another $1 billion in a round led by Coatue.

Polymarket raised capital from Intercontinental Exchange, or ICE, a major traditional exchange operator. In October 2025, ICE committed up to $2 billion, deployed $1 billion, and added another $600 million in March 2026, bringing cumulative investment to about $1.6 billion.

The report describes the resulting structure as one in which traditional financial institutions and top-tier capital repeatedly back the first two players to receive regulatory approval, rather than a market crowded with many competing startups.

Custody grew with institutional demand

Custody investment climbed fifteenfold, from $20.4 million in 2024 to $317.1 million in H1 2026. Anchorage raised a $100 million strategic investment in the first half alone, meaning that one company represented about one-third of all investment in the category during the period.

The report says custody infrastructure that meets regulatory requirements is essential for institutional asset managers holding crypto directly. As demand for asset management and crypto custody services rises, capital flowing into the category has expanded along with it.

It also notes that the stronger-performing sectors discussed above share a common feature: each is tied to infrastructure demand created by institutional entry into the market.

From betting to control

The report’s final argument is that crypto investment has shifted from scattering small bets across short-term opportunities to acquiring stakes in, and control over, infrastructure and protocols.

Before spot Bitcoin ETF approval and the more favorable regulatory environment of 2024, the market was dominated by small narrative-driven bets spread across many projects. The report says that model ended in the collapse of gaming and NFT finance and in the washout of venture firms that continued to rely on it.

Now, capital is no longer chiefly targeting short-term upside. It is being concentrated into a smaller number of companies with auditable revenue models and regulatory licenses, or deployed directly to acquire equity and control the infrastructure itself. In the past, a VC investment in an early project functioned as a signal to the market, often helping lift token prices or attract retail participation. Structural capital aimed at owning infrastructure and licenses does not create that same follow-on signal.

The report says retail investors no longer react as strongly to venture funding headlines because the structure of market capital has changed. The old betting model, in its view, no longer serves either retail participants or venture firms.