Crypto venture capital is still deploying large sums of money, but into far fewer companies. That is the central finding of a report from Tiger Research and RootData, which reviewed 9,416 investment deals recorded between 2018 and the first half of 2026. In H1 2026, total capital inflows reached $13.3 billion, nearly equal to the $13.2 billion raised during all of 2024. Yet the number of funding rounds fell to just 435, down 78% from the 2022 peak of 1,978 deals.

The report says the old spray-and-pray model has largely broken down. Capital is concentrating in a small group of companies that can show mature business models, auditable revenue structures, and regulatory licenses. Traditional financial institutions, meanwhile, took part in 54.5% of investment deals in H1 2026, a level the report describes as evidence that they now hold a dominant position in the market.

A market with more money and fewer checks

The divergence between capital volume and deal count runs through the entire report. H1 2026 produced $13.3 billion in capital inflows, while the 435 deals completed during the period represented only 22% of the 1,978 deals recorded in 2022, the market’s peak year for transaction count.

Large transactions are taking a bigger share of the market. Deals worth $100 million or more totaled 32 in H1 2026, accounting for 7.4% of all transactions, up from 1.1% in 2024. Average deal size climbed from $11.7 million in 2024 to $47.4 million in the first half of 2026.

According to the report, this shift is happening from both ends. Big deals are becoming more common, while smaller financings, including seed rounds, are disappearing. A limited pool of surviving projects is absorbing a larger share of total capital as the long tail of small bets drops out.

What the market looked like in 2021

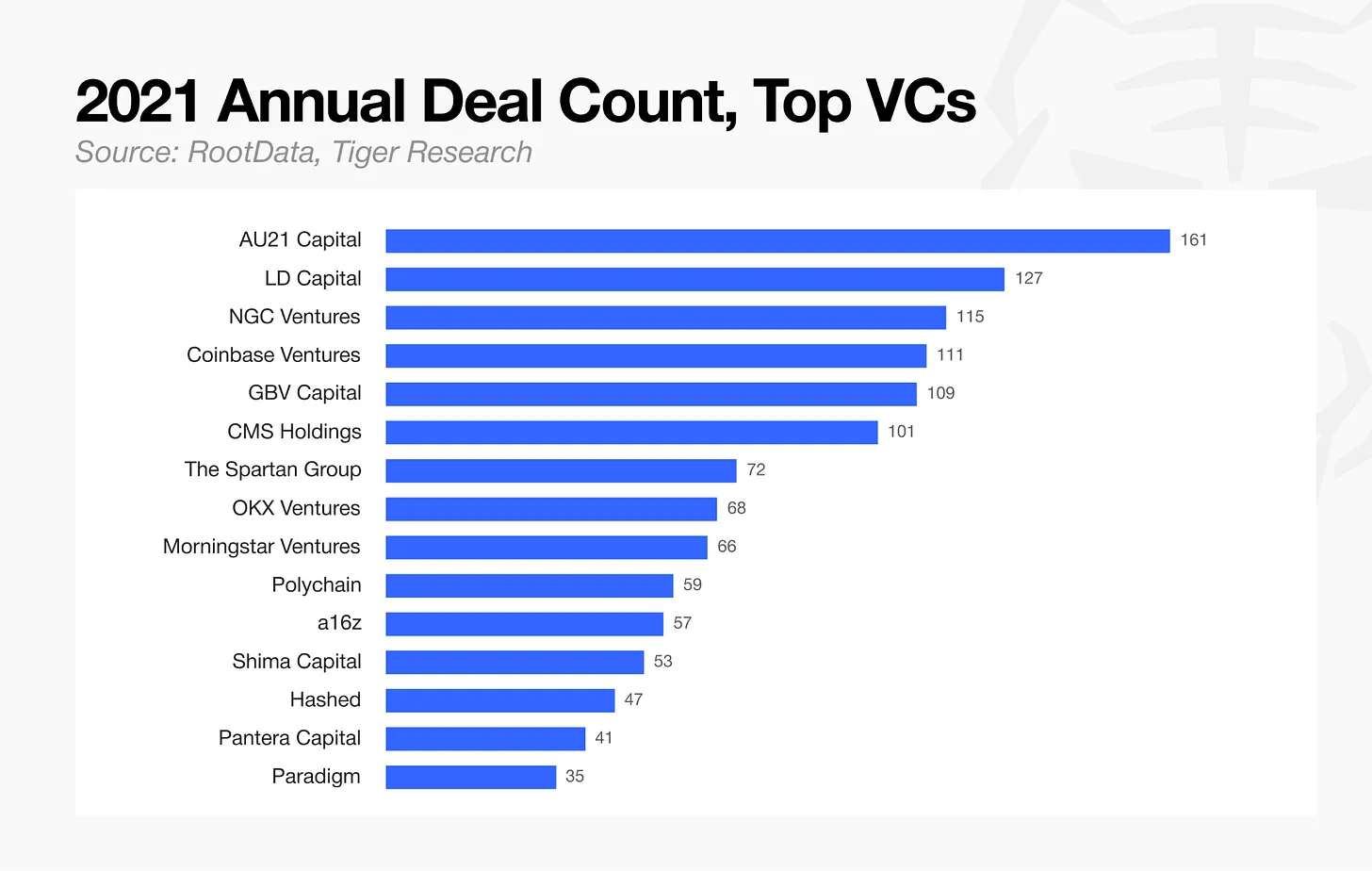

The report contrasts the current environment with 2021, when speed and diversification defined crypto investing. Investors completed 1,750 deals that year, including seed rounds, and competition to move first was intense. AU21 Capital alone averaged more than 13 deals a month.

At the time, investment decisions were often reduced to basic checks such as token generation event schedules and tokenomics. Since token issuance alone could generate returns without requiring a finished product, venture firms spread capital across dozens or even hundreds of projects, often regardless of valuation.

Execution speed outweighed full diligence. New rounds closed quickly, and firms that missed one round often chased the next at a higher price. The report describes that behavior as a recurring FOMO cycle. Many of the funds built around that model did not make it through the following bear market, and those that survived changed their approach at a structural level.

Who survived and how the VC market split

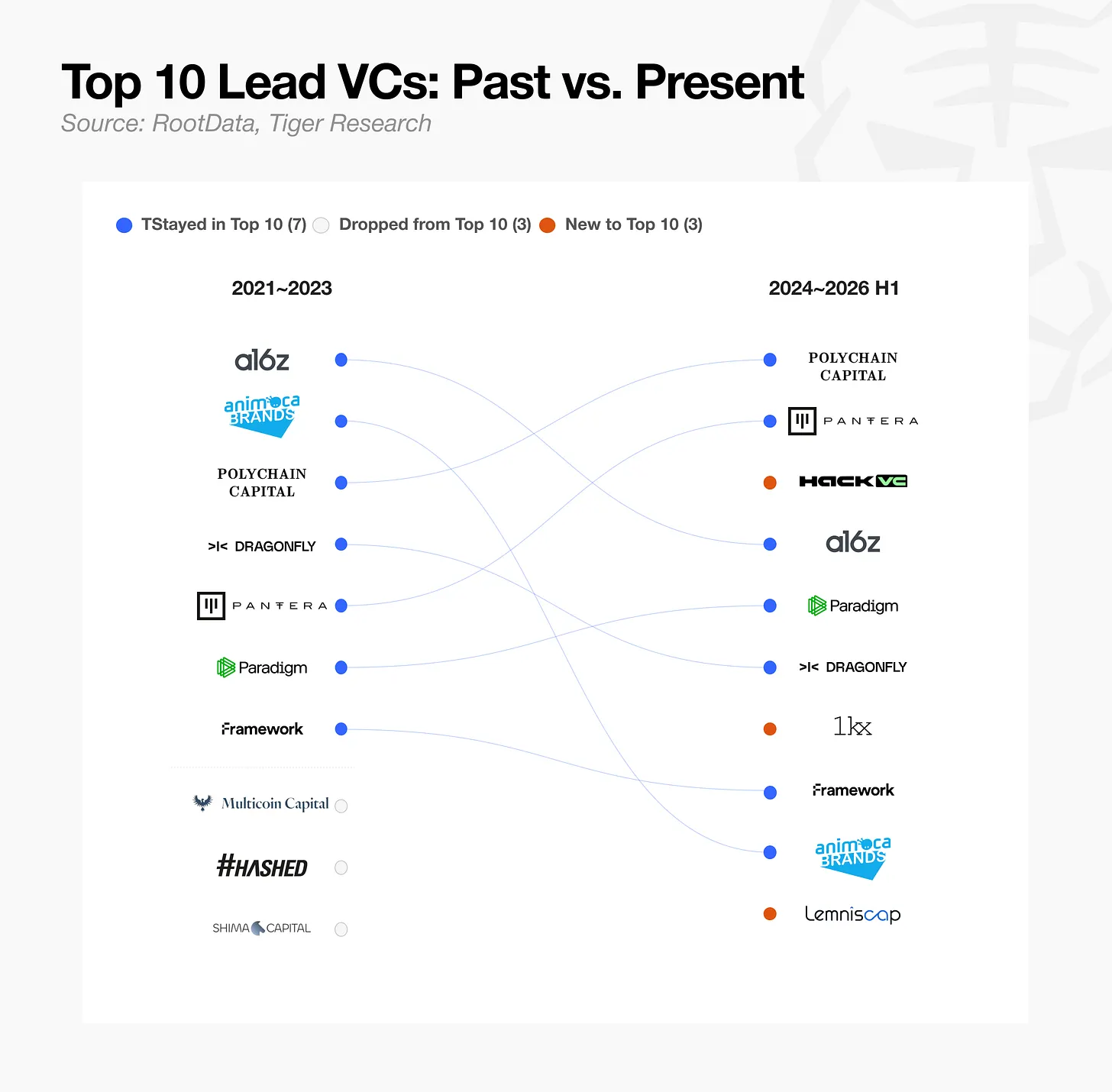

Lead investors retained their edge

The report first looks at lead investing as a way to test durability. Leading a round has historically required the reputation and capital base that only the largest venture firms can offer. As a result, many of the firms that led major rounds in earlier cycles still remain active and continue to appear near the top of the rankings.

The survivors did not all evolve the same way

From 2024 through H1 2026, crypto-native VCs and established large firms increasingly concentrated resources on leading rounds and getting deeper involvement in each deal. They cut the total number of investments, raised diligence standards, and pursued board seats and greater influence over governance.

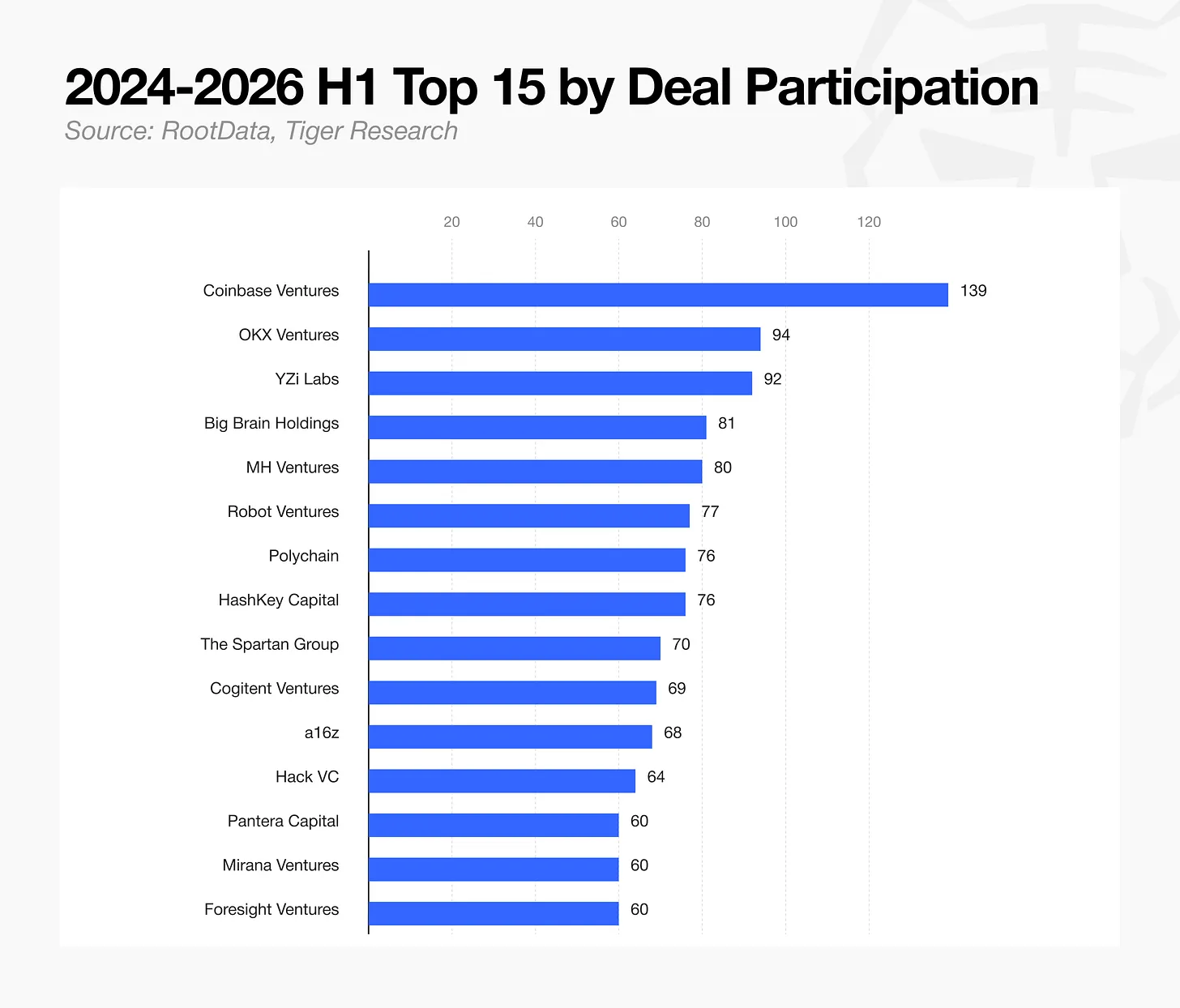

Outside lead roles, though, a different pattern appeared. Among the top 15 firms ranked by total participation count from 2024 through H1 2026, exchange-backed investors held a large share. Coinbase Ventures ranked first with 140 deals, followed by OKX Ventures with 94 and YZi Labs with 92. The report notes that YZi Labs is the organization created after Binance Labs was renamed in January 2025.

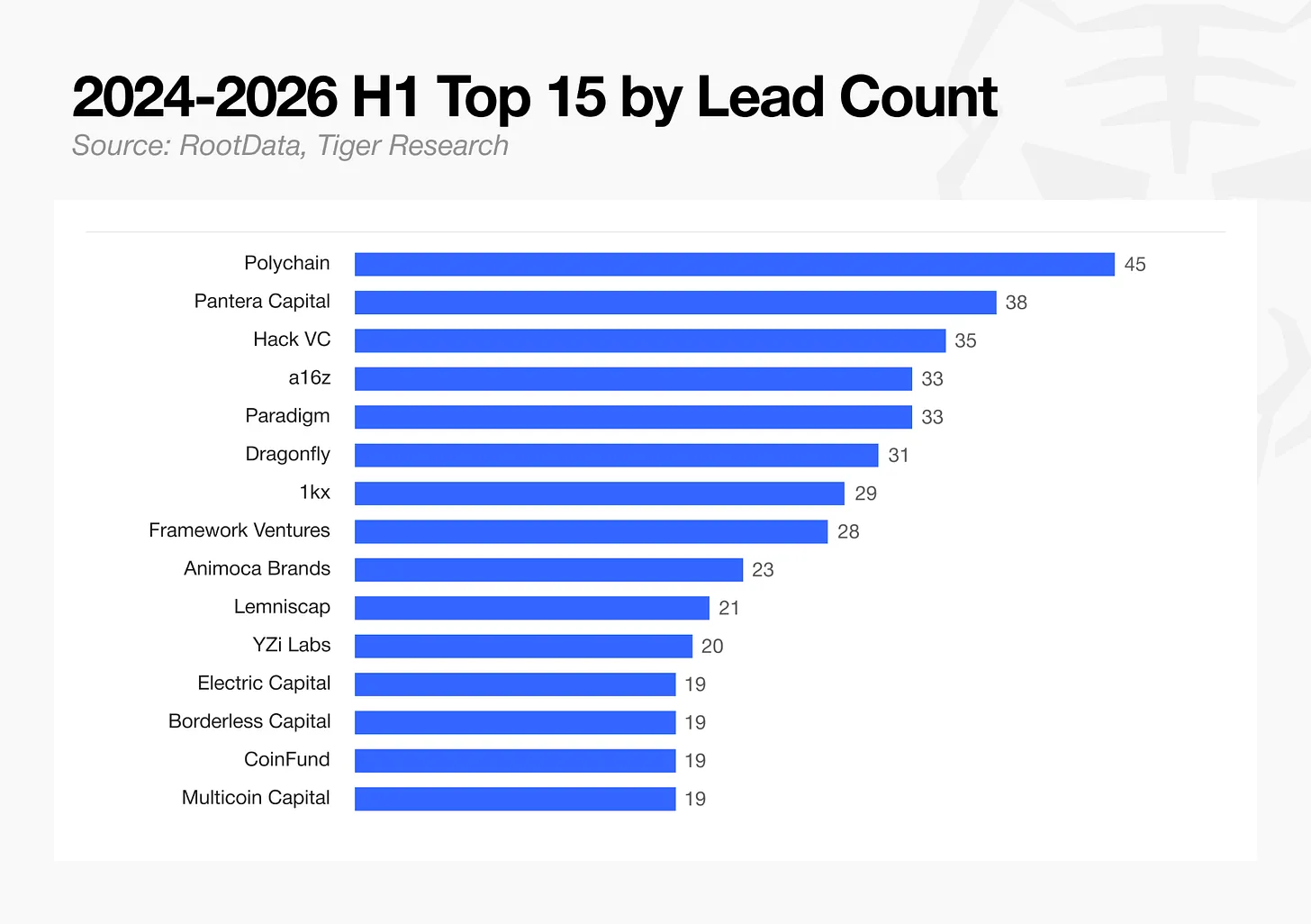

HashKey Capital, the venture arm of Hong Kong exchange HashKey Exchange, ranked seventh. Mirana Ventures, the venture arm of Bybit, ranked fourteenth. Counting only their venture units, five major exchanges appeared in the top 15. Large funds such as Polychain and Pantera Capital, which focus more heavily on leading rounds, ranked lower on overall participation count.

The report argues that exchange-affiliated investors have secured a central place in funding rounds by offering liquidity and marketing support through their platforms. Mid-sized firms without a clear defensible advantage, whether through scale, brand recognition, or exchange-level liquidity, are being pushed out quickly under pressure from failed exits and tighter capital conditions.

The exit of the spray-and-pray funds

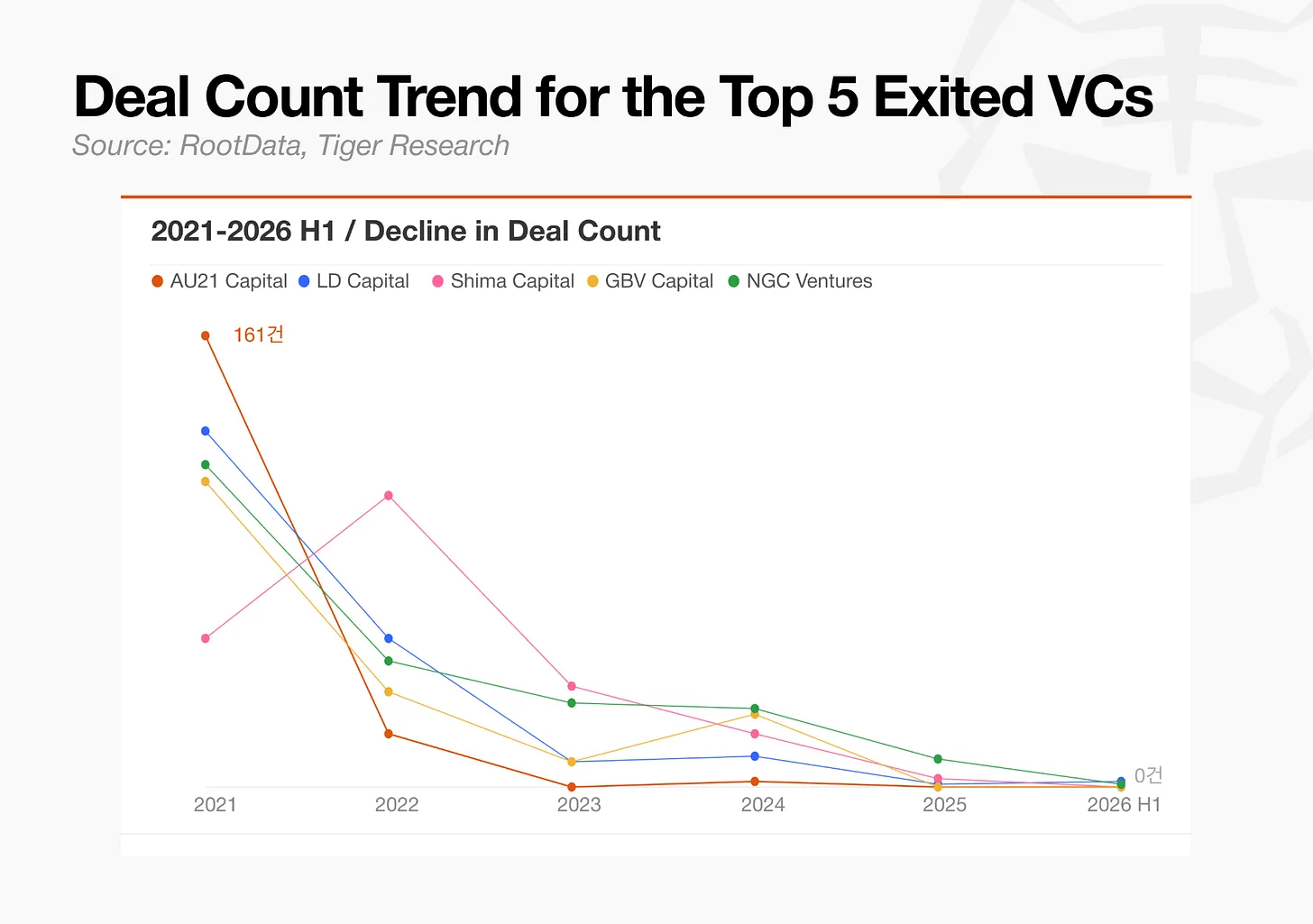

Many of the funds that built broad portfolios during the previous bull market by monetizing token positions quickly have faded from the market. AU21 Capital, LD Capital, and Shima Capital saw deal counts fall by as much as 98.9%, effectively losing market influence, according to the report.

The study points to two reasons. One is a lack of real differentiation. The other is that capital has shifted toward companies that have already reached a degree of maturity, leaving fewer opportunities for the kinds of early-stage bets that once supported those funds.

Funding rounds moved later in the company lifecycle

Seed rounds collapsed

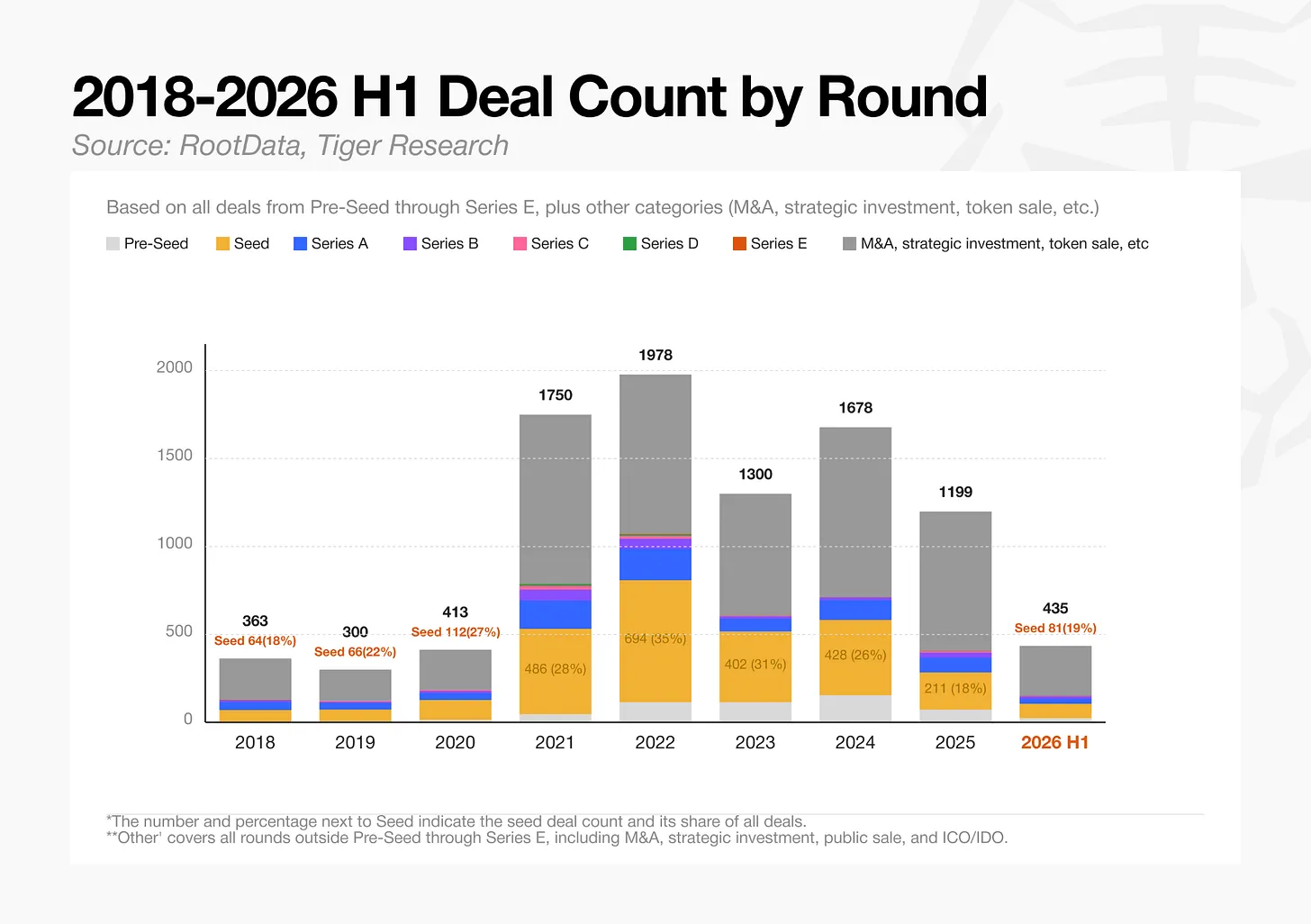

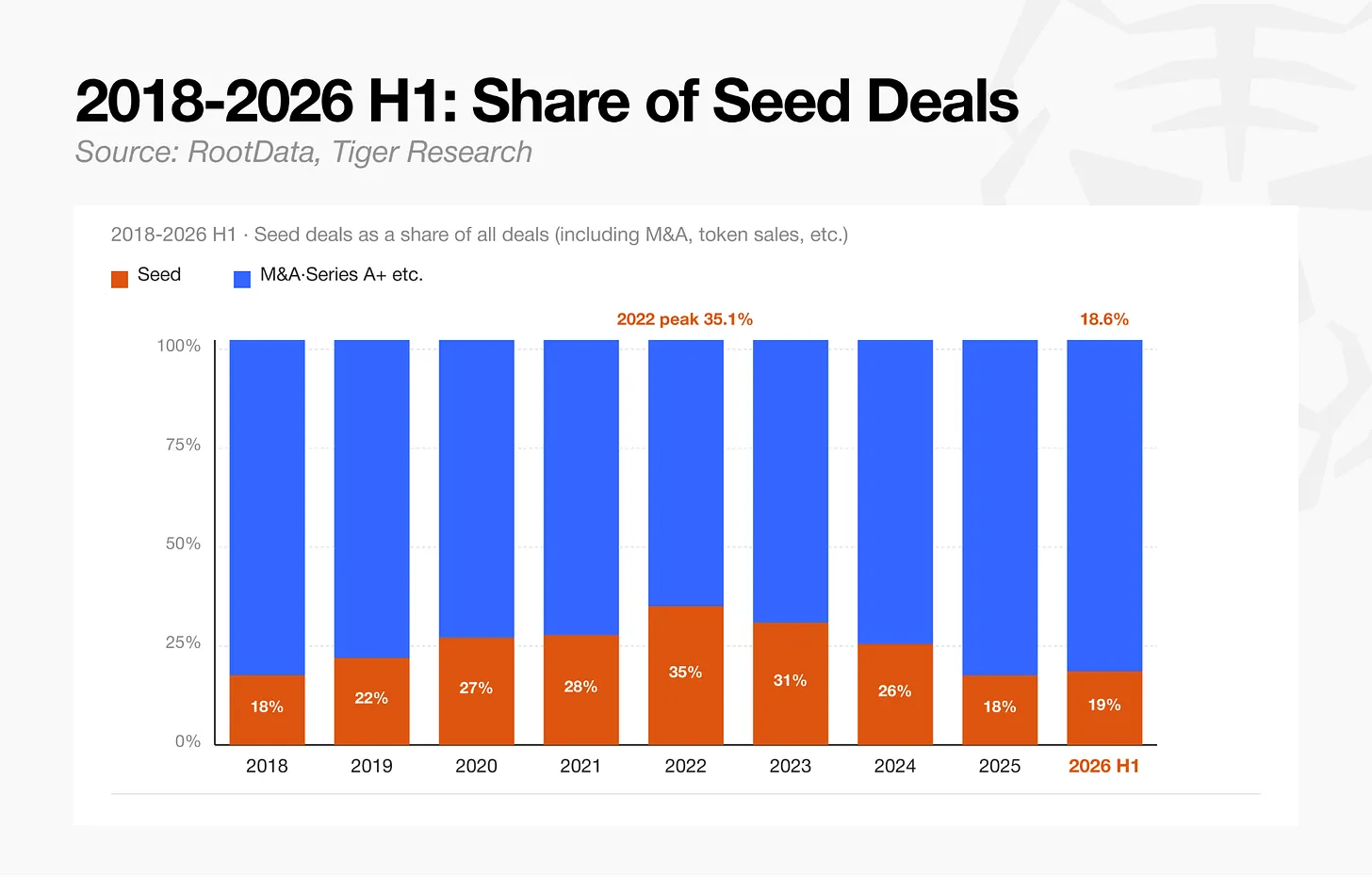

Seed-stage deals totaled 81 in H1 2026, down 88% from 694 in 2022. Seed’s share of all transactions fell from 35.3% in 2022 to 18.7% in the first half of 2026.

The report says this reflects both investor aversion to riskier companies with unproven business models and a basic shortage of new projects seeking seed financing. In that sense, seed contraction captures both market shrinkage and market maturation.

Later stages took most of the capital

By capital allocation, Series A and later rounds accounted for 75.2% of all investment. Seed briefly held a larger share during the 2023 bear market, but capital shifted back toward better-capitalized companies once the market recovered.

In H1 2026, total Series A funding reached $745 million, exceeding the $423 million raised across all seed rounds and making it the largest category among all stages.

Average check sizes rose sharply by stage: $5.4 million for seed, $22.4 million for Series A, $127 million for Series C, and $202 million for Series E. Sample sizes get smaller in later rounds, the report says, but the companies that reach those stages tend to have higher revenue and valuations, which translates into larger capital requirements per deal.

Traditional finance deepened its direct role

The share of investment deals involving traditional financial institutions rose from 29.2% in 2018 to 53.9% in 2021, the first year it moved above half. That participation rate fell to 45.2% in 2023, rebounded to 54.4% in 2024, eased to 50.9% in 2025, and returned to 54.5% in H1 2026. Since crossing the majority threshold in 2021, it has remained near that level.

The report gives one example: a16z led the $355 million financing round for Digital Asset, the developer of Canton Network, but core participants also included BNP Paribas, HSBC, S&P Global, and Hanwha Investment Securities. Those institutions invested directly rather than through venture subsidiaries.

That pattern marks a broader shift. Crypto VCs and traditional institutions are now directing more money to companies that have already reached operational maturity. The report says investors are no longer screening deals around token listing timelines or short-term narratives. They are screening for auditable revenue structures and the regulatory licenses needed to operate.

Sector rotation reshaped the market

The report uses 2024 as the baseline year for sector comparisons because it combined spot Bitcoin ETF approval with a more favorable regulatory backdrop, producing the first clear post-bear-market sector rotation.

In 2024, infrastructure represented 50.9% of total invested capital. By H1 2026, that share had dropped to 14.8%. Payments and stablecoins took the lead with 25.3%, followed by centralized exchanges at 18.2% and prediction markets at 17.5%.

In the report’s view, this shows that blockchain infrastructure is no longer being treated primarily as a standalone investment theme. It is becoming the utility layer for institution-facing businesses. The examples cited include Robinhood running its own layer on Arbitrum, and Securitize using Solana and Avalanche as settlement layers before and after its New York Stock Exchange listing. The core demand in capital markets, the report says, has shifted from building new protocol infrastructure from scratch to operating real-world financial services on top of existing infrastructure.

Gaming, NFTs, and social lost momentum

Three sectors saw especially steep declines: gaming, NFTs, and social and entertainment. Gaming deal count fell from 141 in 2024 to just 5 in H1 2026, a 96% drop. NFT deals fell from 27 to 2. Social and entertainment dropped from 74 to 11.

Capital inflows followed the same direction. Gaming funding fell from $758.6 million to $44.8 million. NFT funding declined from $114.9 million to $14.7 million. Social and entertainment dropped from $512.1 million to $70.1 million.

The report says gaming saw the sharpest deterioration because early GameFi models tied gameplay to token rewards and often depended more on token issuance than on sustainable game design. Once user growth slowed, those systems entered what the report describes as a death spiral, where falling token prices and user attrition reinforced one another. As a result, user traffic metrics that had once been central to diligence lost credibility, and capital largely stopped flowing into the sector.

DeFi stayed active, but in fewer and larger rounds

DeFi deal count dropped 71% from 2024 levels, but total investment fell only about 34%. Average deal size actually increased from $4.5 million in 2024 to $10.4 million in H1 2026, pointing to capital concentration in a smaller number of larger transactions.

The main driver was Morpho. The lending protocol raised $175 million in a token round led by a16z crypto, Paradigm, and Ribbit Capital on June 9, 2026. The report says Morpho used its modular lending protocol to open DeFi vault markets to institutions and redefine DeFi risk standards. That single financing accounted for 17.7% of all DeFi investment in H1 2026.

The implication is that DeFi capital has moved away from broad ecosystem expansion and toward a narrower set of protocols that the market has already validated.

Payments and stablecoins became the fastest-growing segment

Payments and stablecoins posted the fastest growth in the report. Deal count accelerated on a monthly average basis, while total investment surged from $143.9 million to $2.85 billion in H1 2026, almost a twentyfold increase. Still, the report says that jump was driven largely by a few major M&A transactions.

The biggest deal in the segment during H1 2026 was Mastercard’s $1.8 billion acquisition of BVNK in March. The second largest was Payward, Kraken’s parent company, acquiring Reap for $600 million in May. Together, those two transactions accounted for about 84% of the sector’s total investment in the period.

Other fundraising rounds, including Rain at $250 million and KAST at $80 million, also supported growth among cross-border payments and crypto card issuers.

The report interprets those deals as a sign that traditional payment companies and major Web3 firms have moved beyond partnership models and are now acquiring and directly controlling stablecoin infrastructure. Stripe is presented as the clearest case, beginning with its acquisition of Bridge in October 2024.

After that deal, Stripe worked with Paradigm to build Tempo, a blockchain dedicated to stablecoin payments, and launched mainnet in March 2026. In June of that year, Bridge co-founder Zach Abrams became interim head of the entity operating Open USD, or OUSD, a global consortium stablecoin project with more than 140 participating companies.

According to the report, OUSD adopted both Bridge, which Stripe acquired and continued to develop, and Tempo, which Stripe is building, as core initial infrastructure. The result is that the technology and talent Stripe obtained through acquisition now sit at the center of both its proprietary platform and a broader alliance attempting to define industry standards. The report says stablecoin competition has moved beyond company-level acquisitions into a contest over global standards.

CEX capital rose, but the story was consolidation

Centralized exchanges increased their share of total investment from 3.0% in 2024 to 18.2% in H1 2026. Even so, the report says this should not be read as a wave of classic venture expansion into new exchanges. M&A alone accounted for 75.5% of all CEX investment recorded from 2024 through H1 2026. That share rose from 58.8% in 2024 to 78.9% in 2025.

Total capital inflows were lower than the previous year’s $19.4 billion peak, when large M&A transactions were especially concentrated, but still more than six times the 2024 level of $340 million. Deal count also held up. The 23 transactions recorded in H1 2026 worked out to 3.8 deals a month, faster than the monthly pace of 2.8 in 2024 and 3.0 in 2025.

The report describes the CEX market as a reshuffling centered on a small number of large operators. The biggest announced deal during the period was Naver’s acquisition of a stake in Dunamu, which remains under regulatory review. It was followed by Coinbase’s $2.9 billion acquisition of Deribit and Kraken’s $1.5 billion acquisition of NinjaTrader.

MGX, the Abu Dhabi sovereign wealth fund, also made a $2 billion strategic investment in Binance. At the same time, exchange venture arms including OKX Ventures and HashKey Capital became more active in participating in rounds and acquisitions tied to their own ecosystems. In that structure, CEX players increasingly act as both investment targets and strategic investors.

Prediction markets entered the regulated mainstream

Prediction markets emerged as a new sector for providing liquidity around macro indicators such as economic data, elections, and policy decisions. The report identifies a formal regulatory approval by the Commodity Futures Trading Commission in May 2025 as the trigger that opened the door to large inflows from hedge funds and asset managers.

Kalshi’s cumulative trading volume passed $100 billion in June 2026. The company had already raised $1 billion in a round led by Paradigm in December 2025, then raised another $1 billion in a round led by Coatue.

Polymarket, meanwhile, secured backing from Intercontinental Exchange, or ICE, a major operator of traditional exchanges. In October 2025, ICE committed up to $2 billion, deployed $1 billion, and added another $600 million in March 2026, bringing total investment to about $1.6 billion.

The report says this is not a market crowded with many competing startups. Instead, it is forming around a small number of participants that received regulatory approval early and continue to attract repeat large checks from traditional finance and top-tier institutional capital.

Custody expanded quietly but forcefully

Custody grew fifteenfold, from $20.4 million in 2024 to $317.1 million in H1 2026. Anchorage raised a $100 million strategic round in H1 2026 alone, meaning the company represented about one-third of all capital deployed into the custody sector during the period.

The report says custody infrastructure that satisfies regulatory requirements is essential for institutional asset managers that want to hold crypto directly. Growth in the segment has moved in step with rising institutional demand for asset management and crypto custody services.

That same infrastructure logic appears in other sectors that held up well, the report adds. Each has maintained a stable capital base through financings tied to demand created by institutional market entry.

From betting to control

The report’s closing argument is that crypto capital has moved from short-term speculative spreading to ownership and control of infrastructure and protocols.

Before spot Bitcoin ETF approval and the improved regulatory environment of 2024, crypto investing was dominated by small, narrative-driven bets scattered across many projects. In the report’s telling, that model contributed to the collapse of gaming and NFT sectors and to the exit of venture firms that continued to rely on it.

Now the objective is different. Capital is being concentrated into a small number of targets with auditable revenue structures and regulatory licenses, or used directly to acquire equity stakes that secure control of infrastructure.

That also changes the signaling effect of venture activity. In the past, backing an early-stage crypto project could be read as a smart-money signal that helped lift token prices or attract retail interest. Direct infrastructure acquisitions and license-driven strategic capital do not create the same kind of followable signal for retail investors.

The report argues that weaker retail reactions to VC funding headlines are not simply a matter of sentiment. They reflect a deeper structural change in the market’s capital base. The old betting strategy no longer serves either retail investors or venture capital firms.

About RootData

The report notes that RootData launched in early 2022 as a Web3 asset data platform offering a structured investment and financing database for crypto investors and founders. It now processes more than 3.4 million search queries a month and is used by more than 2 million crypto users.

Its data and research have been cited by The Wall Street Journal, Cointelegraph, Binance Research, and The Block, according to the report. The platform focuses on information used for investor decision-making, from project discovery to fundraising tracking and investor analysis.