Three long-term forces at the center of Delphi Ventures’ outlook

Delphi Ventures said the next decade will be shaped by three macro forces: AI and automation, global multipolarity, and demographic change tied to aging and longevity. The firm’s argument is that these shifts compound each other. Lower birth rates and older populations increase the incentive to automate. Automation strengthens self-sufficiency. A more fragmented world raises the appeal of domestic production, energy security, and military capacity.

The report says these are structural trends rather than short-lived cycles. Quarterly volatility may be sharp, but on a 10-year view Delphi sees them as persistent tailwinds. Its broader claim is that as capital replaces labor, preserving and growing wealth will depend more heavily on having the right model of how the world works and investing with conviction on that basis.

AI and automation: demand for intelligence keeps expanding

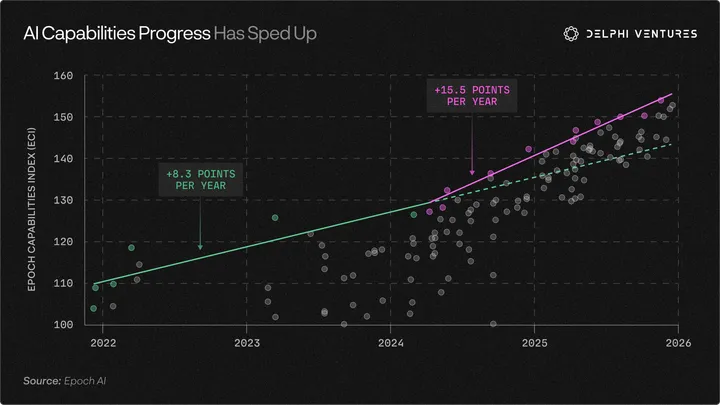

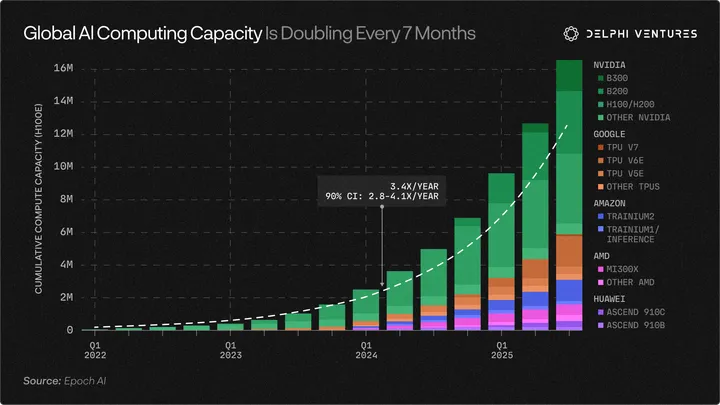

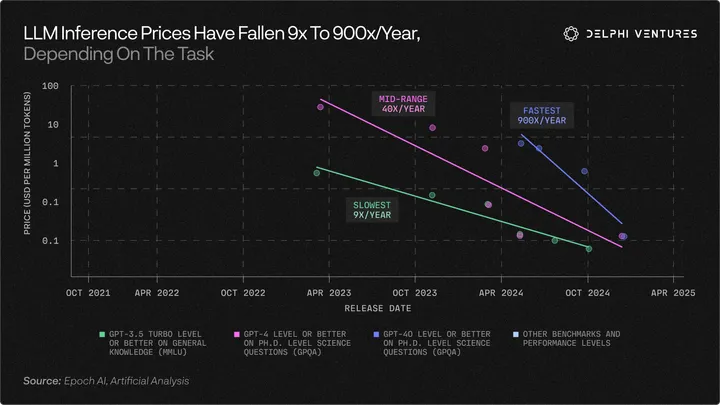

On AI, Delphi’s core point is simple: the market still has not fully priced the scale of future demand for intelligence. The report says silicon and energy can now be turned into intelligence, while bottlenecks in compute, data, and power continue to emerge and then get broken. It lists several trends moving at once: capability is still improving, compute is still rising, inference costs are still falling, and traction is nearing an inflection point.

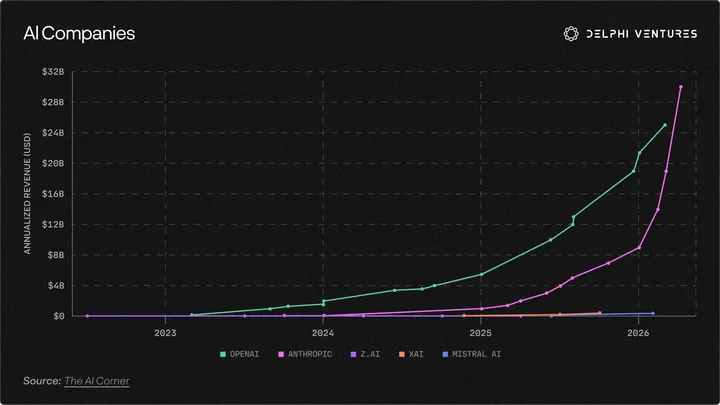

Delphi argues the total addressable market reaches a large share of global white-collar services and may extend into physical labor. It frames the idea in a direct line: demand for intelligence appears to have no clear upper bound. In that context, the firm says every collapse in token cost has expanded the market rather than capped it, bringing previously uneconomic workloads into reach. DeepSeek, in its telling, did not stop the story.

The report also says investment performance increasingly depends on how early allocators become genuinely “AGI-pilled.” It points to a small circle that began to form around San Francisco in 2022 and has since spread outward, including into boardrooms at some of the world’s biggest companies.

Delphi adds that the current wave of digital AI still looks constrained. It is too language-heavy, too digital, and too concentrated in data centers. The next phase, the firm says, should look more like a globally scaled Jarvis: distributed, hybrid networks combining edge and cloud, digital and physical systems, continuous learning, and wider use across the full production chain rather than just office workflows.

Its investment themes follow from that view. Delphi says an agent economy is coming, which means the internet’s indexing, discovery, payments, and commerce rails will be redesigned for agents as major consumers and producers of digital information. It also says the most valuable networks will be those that best coordinate data, compute, and intelligence, whether through vertically integrated companies, fully distributed networks, or mixed models.

The report keeps a strong focus on supply bottlenecks. It highlights memory, power, EUV, manufacturing capacity, photonics, and space-based networks. It also says Taiwan Semiconductor Manufacturing capacity remains an important supply constraint, limiting the kind of excess that defined earlier infrastructure booms.

At the seed stage, Delphi points to vertical data “foundries,” agent compliance, grid upgrades, advanced packaging, chip interconnects, specialty materials, and embodied AI data flywheels.

Macro implications tied to the AI view

- Capital becomes scarce again, with rates staying high in the near term.

- K-shaped divergence deepens.

- Assets levered to service-sector consumer spending, including mortgages, credit, and consumption, warrant caution.

- Politics could move sharply left as inequality and anti-AI sentiment rise, bringing higher taxes, more surveillance, and tighter capital controls.

- Input inflation may come first, followed by broad service deflation and then goods deflation.

- The globalization-era pattern of catch-up growth may reverse, with AI winners pulling away. Delphi says China may be the last emerging economy to reach relative prosperity through a manufacturing-led path.

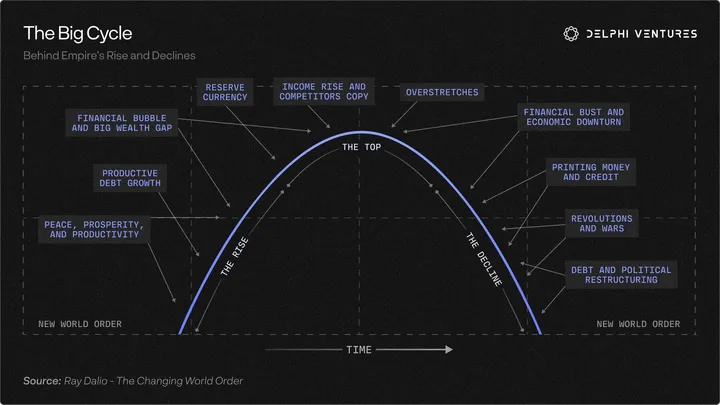

Multipolarity: the US steps back, the rest of the world feels the strain

In the report’s second section, Delphi describes Donald Trump’s second election win in 2024 as a referendum on the existing world order. It traces that order back to 1945, then says it accelerated after 1989 around global supply chains, free capital flows, and a system centered on the US consumer.

Delphi’s view is that the order has now been rejected. It links that shift to tensions between liberalism and national interest, meritocracy and inequality, global capital and domestic labor, and the Triffin dilemma. The report says the relative stagnation of the US middle class and rising national security vulnerability have started the countdown on an 80-year system.

As countries move to shore up redundancy, energy security, technological sovereignty, and military preparedness, Delphi says the setup favors fiscal deficits, commodities, and long-term inflation trades. That is happening at a time when global debt has risen above 300% of GDP.

Citing Peter Zeihan’s framework, the report says globalization is inherently fragile. Optimized supply chains, free energy flows, low insurance costs, and limited military conflict allowed rich countries to keep importing disinflationary goods while poorer countries climbed from agriculture to low-cost manufacturing, urbanization, and services. Delphi argues that system is now being dismantled.

From that angle, it says commodities, energy, and hard money look mispriced on a 10-year view. At the same time, Delphi stresses that the US is in the strongest position to leave the old order with fewer consequences than others. It points to friendly neighbors, military strength, energy independence, food independence, and US leadership in AI.

The burden, in Delphi’s framing, falls more heavily on others. The report references Europe’s natural gas problems after the Ukraine war, energy stress in East and Southeast Asia after the closure of the Strait of Hormuz, and diaspora flight during a prolonged Middle East conflict. It says almost no one, with the possible exception of China, has fully prepared for such a transition.

China, Delphi writes, is in a weaker geographic position and remains dependent on energy, food, and technology in important ways, but that is also why it has spent decades investing in renewables, semiconductors, military buildup, and food security. Other countries have not done the same, the report says.

The firm also argues that labor-rich developing economies may face a sharp reversal. In a world of contested shipping lanes, higher insurance costs, and structurally higher energy prices, capital- and compute-rich states can shift toward automated domestic production. Population dividends then start to look more like population burdens.

For seed investors, Delphi points to onshoring-related processing, software for second-source certification and supply-chain mapping, services around open-weight models, war and political risk insurtech, supply-chain disruption coverage, geopolitical risk intelligence, vertical farming, gene-edited crops, and stablecoin-based dollar access and trade finance rails. It describes a split where central banks may be de-dollarizing even as street-level dollar demand in emerging markets remains strong.

Demographics and longevity: aging as a fiscal problem and a biotech opportunity

The third section focuses on aging populations. Delphi says only four countries had fertility below replacement in 1950. By 2024, that number had reached 136, or 71% of the world. It puts China’s total fertility rate at about 1.0. It also says more than one-third of the populations of Italy, Portugal, Greece, Japan, and South Korea will be older than 65 by 2050. In the US, 10,000 baby boomers turn 65 each day, and the Social Security trust fund is expected to run out in the early 2030s.

The summary line is blunt: people are living longer and having fewer children. Delphi argues the industrial-era welfare state was built on birth rates above replacement, and that model breaks when demographics invert.

The most obvious answer, in the report’s view, is some mix of currency debasement and faster automation, combining money printing, higher taxes, agent-driven productivity, and robotics. But Delphi also outlines a more optimistic path: extending healthy life and productive years.

Here the report points to Yamanaka factors as evidence of cellular aging reversal and notes that companies such as NewLimit, Altos Labs, and Life Biosciences have raised billions of dollars. Because of the US Food and Drug Administration framework, the report says these companies target specific organ diseases first, though the larger ambition is to treat aging itself.

Delphi also says AI-biology has not drawn the same level of market enthusiasm as AI and robotics until recently. It argues that growing compute capacity is opening new insight into protein folding, polygenic traits, and cellular mechanisms. The report quotes Demis Hassabis: “If mathematics is the language of physics, then machine learning is the language of biology.”

It adds that GLP-1 is only the beginning. If genome editing and cellular age reversal become practical, a large share of discretionary spending in a post-scarcity economy could flow toward life extension. In the medium term, Delphi says it hopes AI’s biggest gift to people will be longer life, helping offset demographic pressure before humanoid robots arrive at scale. Over the longer term, it hopes AI-led deflation, fertility technology advances, artificial wombs, lower child-rearing costs, and a 50% reduction in working hours could support a recovery in birth rates.

Seed opportunities listed in the report include aging clocks and longitudinal multi-omics data, biomarker and biological age companies, at-home multi-omics sampling, implantable biosensors, human enhancement, brain-computer interfaces, AI for skilled trades, fertility technologies, and products for the 60-80 age cohort, which Delphi describes as historically wealthy but still underserved.

The acceleration dilemma and why crypto remains central

Delphi closes by framing the next decade as a tug-of-war created by technological acceleration. Without faster technology, it says, economies risk getting trapped in a loop of worsening demographics, deficits, and degrowth. With acceleration, the world faces higher tail risks and sharper inequality.

Its conclusion is that acceleration is the only real option, but one that must be managed carefully and paired with broader distribution of gains. The report notes that debt-to-GDP is already above 300%, demographic pyramids are inverting, deficits are high, and reindustrialization, national security, climate transition, and grid capacity all demand major investment. In domestic-currency debt crises, Delphi argues, governments tend to print.

It quotes Keynes quoting Lenin: “There is no subtler, no surer means of overturning the existing basis of society than to debauch the currency.”

From there, Delphi lays out four interacting futures: techno-feudalism, a more China-like model of technologically enabled control, a flight to network-based systems, or a narrow path where societies accelerate just enough to escape the doom loop while distributing gains widely enough to preserve support inside existing institutions.

That is where crypto enters the thesis most clearly. Delphi says its framework depends heavily on crypto as a cleaner parallel system for exchange, coordination, and wealth preservation in a world of demographic inversion, rising deficits, political fracture, and currency debasement.

Its preferred hedge remains a barbell between hard assets and internet-native alternative stores of value: long commodities, energy, and defense; short fiat and bonds; and use Bitcoin, Zcash, and the distributed agent economy to hedge against debasement, confiscation risk, fragile municipalities, and non-G2 emerging-market stress.

Delphi also says the productivity boom opened by the intelligence revolution in November 2022 may still overpower the drag from demographics, deficits, and debasement. The firm says it will continue backing founders building outside current institutions while also investing in top talent rebuilding the existing system from within. Its final message is direct: by 2035, the world and low Earth orbit will be filled with accelerating compute, and inflection points are already visible in agents, robotics, launches, advanced materials, and new therapies.