Delphi Ventures lays out a 10-year framework

Delphi Ventures says three structural forces — automation, multipolarity, and demographic change — will reshape global asset pricing over the next decade, with intelligence becoming the scarcest resource. In the firm’s framing, these trends reinforce one another rather than move separately. Lower birth rates and aging populations create a stronger case for automation. Greater automation supports self-sufficiency. A smaller pool of young men points to more automated warfare.

The firm argues that rising spending on automation, self-reliance, rearmament, and healthcare will put more strain on government finances in the near term, leaving sharper productivity gains as one of the few credible offsets. Quarterly swings may be large, it wrote, but the underlying forces are unlikely to slow on a 10-year view.

Delphi also says that as capital replaces labor, wealth preservation and wealth creation will increasingly depend on having the right model of the world and investing with conviction. The firm describes the current moment as less than four years into the biggest technological revolution in human history, with billions of new economic actors expected to emerge first as agents and later in physical form.

It ties that thesis to broader political and macro stress. The note points to more than 85% of U.S. voters feeling frustrated with the opposing party, global debt above 300% of GDP, worsening inequality, and a U.S. retreat from its role as global hegemon.

AI and automation: demand for intelligence still outstrips supply

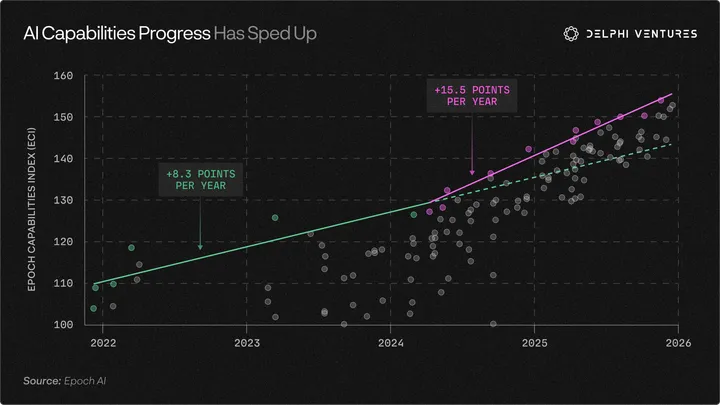

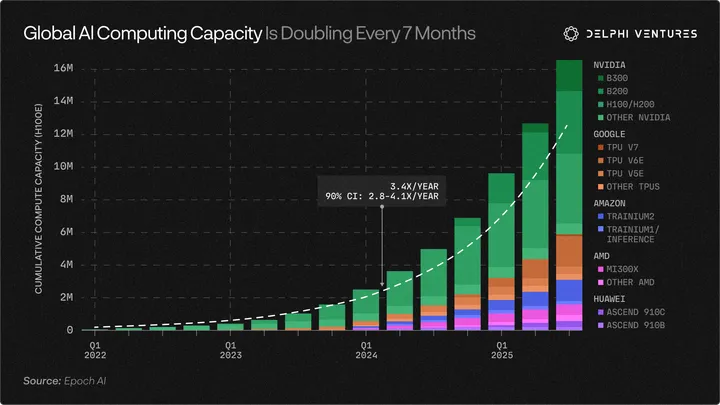

On AI, Delphi’s view is straightforward: the people who kept betting that the world still did not have enough compute have been right at major turning points. The report says silicon and energy can now be converted into intelligence, and while bottlenecks will emerge in compute, data, and power, those constraints are likely to be broken again.

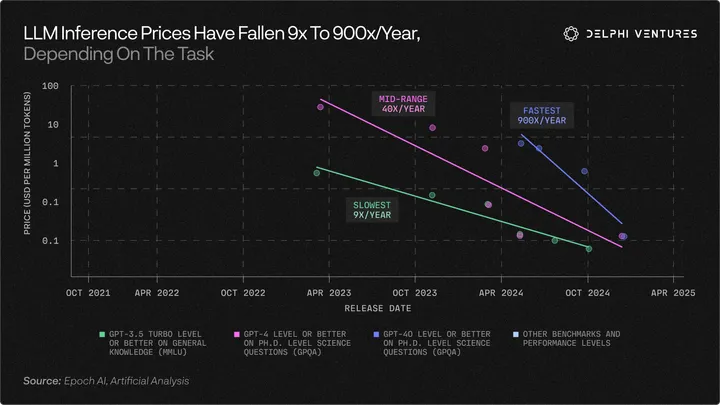

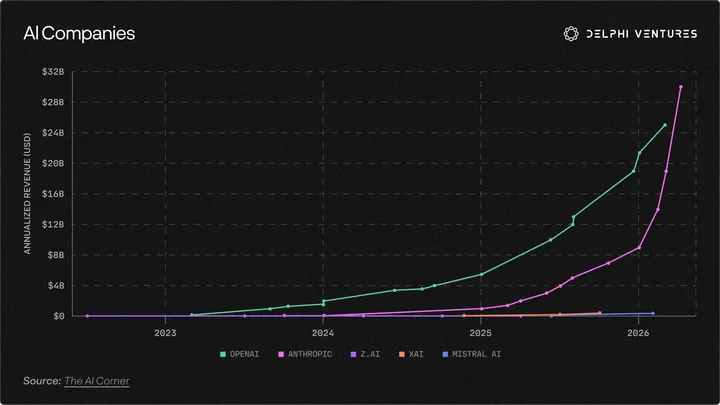

The firm’s central claim is that capability is still accelerating, compute keeps rising, inference costs keep falling, and market pull is reaching an inflection point. The addressable market, in its view, covers a large share of global white-collar services and could extend into physical labor.

Delphi writes that the market is still misreading one key point: lower costs have not shrunk the opportunity. It says DeepSeek was supposed to be the moment when the music stopped. Instead, every collapse in token costs pulled in workloads that had previously been uneconomic. The conclusion is blunt: there is no compute surplus, only a demand function that keeps getting hungrier.

The note also says investment outcomes are increasingly tied to how early allocators became truly “AGI-pilled.” Delphi traces that belief system back to San Francisco in 2022, then names circles that include Hayes Valley, readers around the Less Wrong forum, OpenClaw hosts in Liangzhu, and a growing number of large corporate boards.

Still, the firm sees the first wave of digital AI as constrained — too dependent on language, too digital, and too trapped in data centers. The next phase, it argues, will look more like Jarvis at global scale: distributed, environmental systems that combine cloud and edge, digital and physical infrastructure, and continuous learning. In that model, AI spreads beyond office workflows into the full production chain.

From that thesis, Delphi draws several investment themes. Agent economies are coming, and the internet will be redesigned for agents across indexing, discovery, payments, and commerce. Networks that coordinate data, compute, and intelligence effectively could become highly valuable. Demand for intelligence should continue to outrun supply for the foreseeable future. TSMC manufacturing capacity remains a bottleneck. Memory, power, EUV, fabrication capacity, photonics, and space-based networks all sit on the list of constraints worth watching.

The report also points to real-world APIs as the next frontier, with AI shifting toward hybrid edge-cloud systems that balance cost, latency, and privacy. That extends into 3D printing, new materials, precision manufacturing, and lower dependence on specialized global supply chains.

At the macro level, Delphi expects capital to become scarce again, with rates staying high in the short term. It sees a sharper K-shaped economy, warns against leveraged assets tied to service-sector consumption, and says anti-AI politics could push tax rates, surveillance, and capital controls higher. The price path it sketches starts with input inflation, then broad service deflation, then goods deflation.

Early-stage themes in this section include vertical data foundries, agent compliance, grid upgrades, and data flywheels in embodied AI.

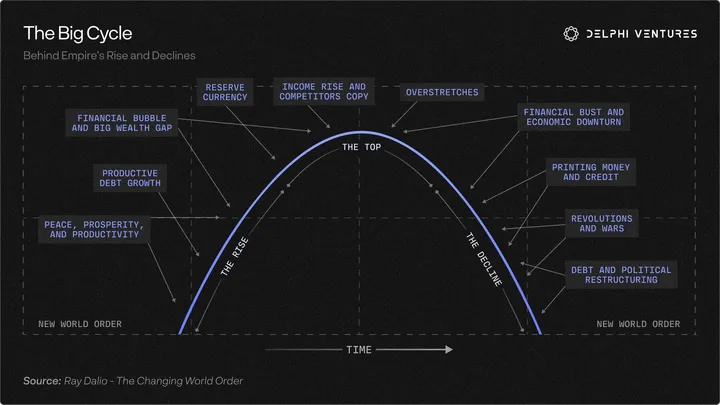

Multipolarity and the end of the old global order

In the geopolitical section, Delphi says Donald Trump’s second election in 2024 was a referendum by the U.S. public on the existing world order. It describes that order as one that began in 1945 and accelerated after 1989, built on global supply chains, free capital flows, and a demand engine centered on the U.S. consumer.

That order, Delphi argues, is now being rejected. The report says the post-Bretton Woods system delivered peace and abundance, but also contained tensions that made its own decline likely: liberalism versus national interest, meritocracy versus inequality, global capital versus domestic labor, and the Triffin dilemma.

As the U.S. steps back, countries are scrambling to reduce dependence on global supply chains and shore up energy security, technology sovereignty, and military capacity. Delphi says that setup supports the long-term case for fiscal deficits, commodities, and inflation, even as global debt is already at record levels.

The firm references Peter Zeihan’s framework to argue that globalization was always fragile. Optimized supply chains, low insurance costs, open energy flows, low conflict, and labor arbitrage all depended on U.S. hegemony. As that system is dismantled, Delphi sees clear mispricing over a 10-year horizon in commodities, energy, and hard money.

At the same time, it says the U.S. is the country best positioned to absorb the consequences of withdrawal. The country is bordered by friendly neighbors, has the world’s strongest military, is energy independent, is food independent, and leads in AI. The adjustment would be uncomfortable, Delphi says, but not catastrophic. For others, the problem is bigger. Outside China, the report says, few were actually prepared.

China, in Delphi’s telling, sits in a weaker natural position because of energy, food, and technology dependencies, but that is also why it has spent decades investing in renewables, semiconductors, military buildup, and food security. Many other countries have not.

The report argues that in a world with more hostile sea lanes, higher insurance costs, and elevated energy prices, countries rich in capital and compute will automate production at home. Cheap labor then turns from an advantage into a liability. Over the next decade, states with capital, elite technical talent, scale, and the political will to deploy AI and robotics could pull ahead again.

Delphi lists several startup themes tied to that shift: rare earth separation and magnet manufacturing, uranium enrichment and HALEU, de-DJI stacks in Western drones, lower-tier supply-chain mapping, bottleneck intelligence, friend-shoring procurement tools, services built around open-weight models, war and political-risk insurance technology, supply-chain disruption cover, and geopolitical pricing intelligence. It also says that even if official de-dollarization continues, street-level dollar demand in emerging markets may rise, supporting stablecoin dollar access and trade-finance rails.

Demographics and longevity

Delphi’s third pillar is demographics, paired with longevity. It notes that in 1950 only four countries had fertility rates below replacement. In 2024, that number had climbed to 136, representing 71% of the world. China’s total fertility rate is described as roughly 1.0. By 2050, more than one-third of the population in Italy, Portugal, Greece, Japan, and South Korea is expected to be older than 65. In the U.S., 10,000 baby boomers turn 65 every day, while the Social Security trust fund is projected to run out in the early 2030s.

The summary line is simple: people are living longer and having fewer children. Delphi says the implications for budgets, elder care, healthcare spending as a share of GDP, and labor-force participation are obvious. Welfare states built in the industrial era assumed fertility above replacement. That demographic base is now inverted.

The most likely answer, in Delphi’s view, is a mix of currency debasement and faster automation: printing, taxes, agent productivity, and robotics. But the firm also outlines a more optimistic path in which longer healthy lifespans keep people productive for more years and reduce some of the pressure from population aging.

The note points to signs of cellular age reversal around Yamanaka factors and says longevity companies including NewLimit, Altos Labs, and Life Biosciences have raised billions of dollars. By comparison with AI and robotics, market enthusiasm for AI-biology has remained muted until recently, it says, even as new compute helps unlock problems in protein folding, polygenic traits, and cellular mechanisms.

Delphi quotes Demis Hassabis directly: “If mathematics is the language of physics, then machine learning is the language of biology.” From there, the firm argues that better understanding of biology could drive much more spending in longevity, with GLP-1 representing only an early example.

In the medium term, Delphi says AI’s biggest gift to humanity could be longer life, boosting productivity later in life and helping maintain demographic balance before humanoid robots scale. Over the longer term, it says AI-driven deflation could support higher birth rates through embryo screening, fertility technology, artificial wombs, lower child-rearing costs, and a 50% reduction in work hours.

Seed themes in this section include biomarker and biological-age companies, at-home multi-omics sampling, implantable biosensors, human augmentation, brain-computer interfaces, AI tools for skilled trades, fertility technology, and products built for the 60-80 age cohort.

Why crypto remains central in Delphi’s framework

The report then turns to a broader tension. Without faster technology, Delphi says, the world risks getting trapped in a doom loop of demographics, deficits, and stagnation. With acceleration, the risks shift toward instability and deeper inequality. Even so, the firm says technological acceleration is the only real option.

It repeats the macro backdrop: debt-to-GDP above 300%, inverted population pyramids, rising deficits, and major spending needs tied to reindustrialization, national security, climate transition, and grid capacity. Delphi cites Ray Dalio’s warning that governments print in debt crises denominated in their own currency, then adds the Keynes quote attributed to Lenin on currency debasement as a way to undermine the foundations of society.

That, in Delphi’s argument, is where crypto matters most. The firm says a world shaped by population inversion, larger deficits, political division, and weaker money needs a parallel system for exchange, coordination, and wealth preservation. It frames hard assets on one side and internet-native stores of value on the other as a barbell approach. The note explicitly names commodities, energy, and defense on one end, and Bitcoin, Zcash, and distributed agent economies on the other.

Those positions, it says, can hedge against debasement and confiscation, especially outside the G2 and in fiscally stressed local governments. Delphi also says that since the “intelligence revolution” emerged in November 2022, the odds have improved that a productivity boom in the next decade could outweigh the pressures from demographics, deficits, and currency debasement.

The note ends on that optimistic view. Delphi says the world is still facing debt, widening deficits, polarization, a global cost-of-living crisis, war, great-power politics, and uncontrolled AI risk. But by 2035, it expects accelerating compute to fill the world and low Earth orbit, while agents, robotics, launch systems, advanced materials, and new therapies reach inflection points. Its closing line is direct: “The future belongs to optimists. Invest accordingly. We certainly will.”