TechFlowPost has published a roundup of several recent research notes that have become reference points for investors watching crypto, AI, privacy infrastructure and tokenized real-world assets. The piece, written by ChainFeeds and translated by TechFlow, frames them as practical questions for this cycle: whether ETH still deserves a place in portfolios, how much runway AI equities have left, whether privacy AI solves a real problem, and what on-chain RWA needs to do next beyond simple tokenization.

Ethereum is not losing relevance, but its old investment case is weakening

The first research note revisits Ethereum through a macro and financial lens. Nick Researcher argues that the latest data from the second quarter of 2026 points to a more complicated picture than a simple bull or bear case. Revenue improved slightly from the prior quarter, but Layer 1 fee capture remained far below last year’s level. On-chain yield moved close to historic lows. DeFi activity softened. The Layer 2 ecosystem kept expanding, and projects including Robinhood continued building on Ethereum-related infrastructure, yet that activity still did not feed enough value back to the base layer. At the same time, ETH dilution stayed near Bitcoin-like levels.

The core dispute around ETH, in this framing, is not whether Ethereum has become uncompetitive. It is whether the investment logic that used to support ETH still works. For a long time, the bullish case was straightforward: more users on Ethereum would drive up L1 activity, increase fees, burn more ETH, and strengthen value capture at the token level. That model is now under pressure. Users have been moving to L2s, and some have left the ecosystem because the L2 experience has not fully met expectations. Transaction fees have fallen. Blob supply has been growing faster than demand. L2s process a large share of user activity, but the fees they pass back to Ethereum mainnet remain limited.

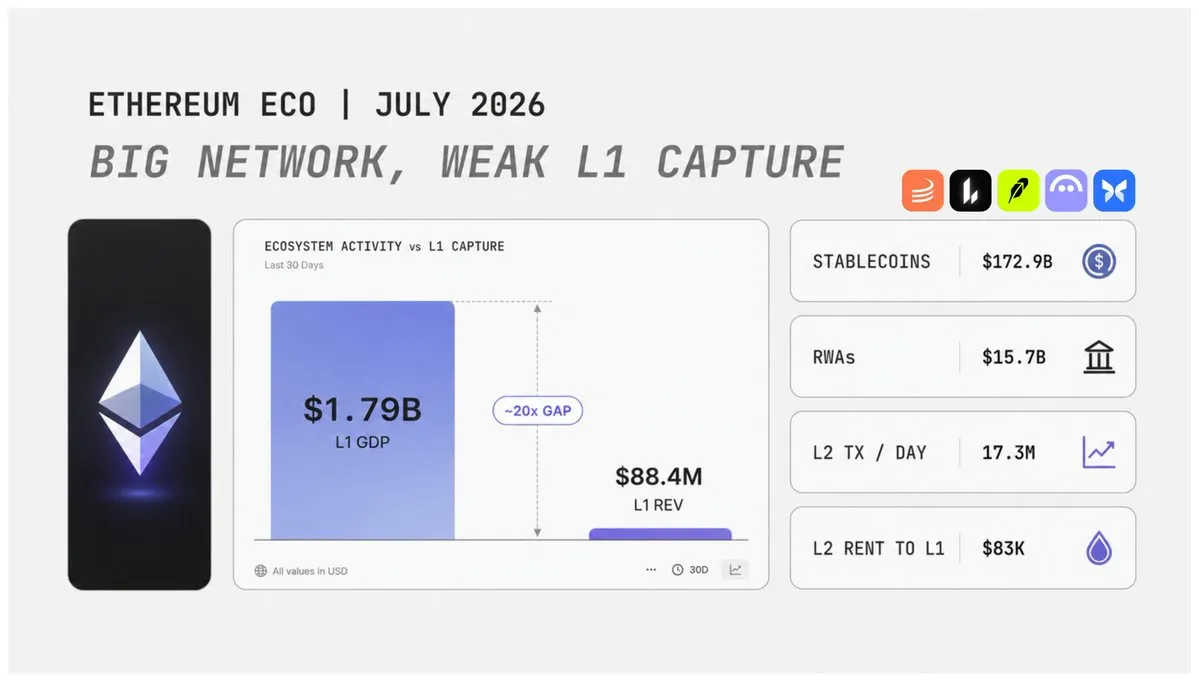

The most important data point is from the second quarter of 2026. Ethereum L1 generated $88.4 million in Real Economic Value, up 7% quarter over quarter but down 68% year over year. Over the same period, applications on Ethereum L1 generated about $1.79 billion in fee revenue. The takeaway is not that the ecosystem lacks economic activity. It is that the application layer is still producing meaningful value while the base layer captures only a small portion of it. That is the central contradiction in the ETH investment case today.

Ethereum still hosts a large share of critical on-chain finance. The report points to Tether, Circle, Lido, Aave and Uniswap as major participants in the ecosystem. Stablecoins remain one of Ethereum’s strongest advantages. In Q2 2026, stablecoin supply on Ethereum L1 reached $172.9 billion. That was down about 4% from the previous quarter, but still large by any measure. Size alone, however, is not enough. The speed at which capital moves matters too. If stablecoins sit on-chain without being used in trading, settlement or collateralized finance, they do not create much economic value. The problem, in that sense, is not a shortage of assets on Ethereum. It is weak capital velocity.

Real-world assets may become the next major growth driver for ETH. The report says on-chain RWA on Ethereum L1 has already surpassed $15.7 billion, up about 90% year over year, including tokenized Treasuries, commodities and equities. But a bigger TVL does not automatically mean better value capture. In Q2 2026, Solana’s average daily RWA trading volume exceeded Ethereum’s despite Solana having lower RWA TVL. That suggests Ethereum’s edge lies more in institutional depth, while Solana’s edge shows up in turnover and transaction flow.

Under this framework, ETH needs three conditions to hold at the same time if a stronger upside case is to re-emerge:

- more institutional assets need to enter the Ethereum ecosystem;

- more financial settlement activity needs to happen on Ethereum;

- on-chain assets need to generate meaningfully higher real transaction frequency.

The token model still offers some support. The annualized net dilution rate in the second quarter was about 0.85%, close to BTC. But the report also flags a clear risk. Total on-chain yield has fallen to 2.68%, the lowest on record, and 94% of that yield comes from ETH issuance rather than real user fees. In other words, whether ETH can be re-rated from here may depend on whether Ethereum can function as a settlement layer for institutional finance.

BlackRock sees the AI rally around the “midpoint” of the dot-com comparison

The second note comes from BlackRock, which uses Morningstar data to compare the current AI-driven market cycle with the late-1990s internet boom.

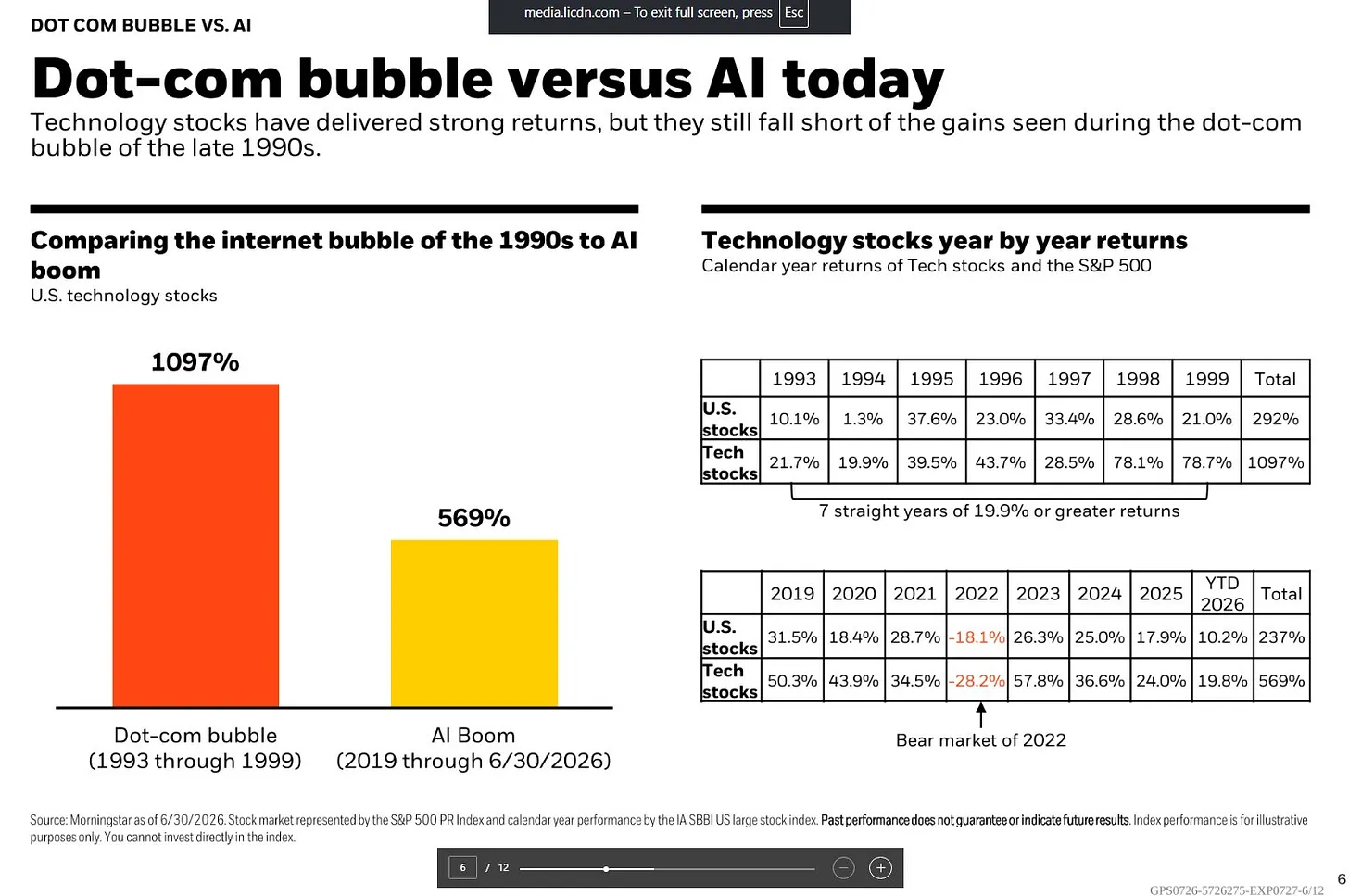

From 1993 to 1999, US technology stocks rose 1,097% cumulatively, while the broader US stock market gained 292%. Annual returns for tech stocks stayed above 19.9% for seven straight years. The final stretch was especially dramatic, with gains of 78.1% in 1998 and 78.7% in 1999.

By contrast, from 2019 through June 30, 2026, technology stocks in the AI cycle rose 569% cumulatively, compared with 237% for the broader US market. The move has also been powerful, but the path has been different. Tech stocks fell 28.2% in 2022, then rebounded 57.8% in 2023, gained 36.6% in 2024, added 24.0% in 2025, and rose another 19.8% in the first half of 2026.

The clearest difference appears in the back half of the cycle. During the dot-com boom, the market accelerated sharply in the final two years, with gains near 200% combined across 1998 and 1999. In the AI cycle, there was a visible burst higher in 2023, but gains narrowed after that. The move has looked steadier than the internet bubble, yet the market is still split on whether a final blow-off phase could develop.

Valuation is where the debate becomes most intense. The S&P 500’s Shiller CAPE has climbed to around 40x, back near levels last seen during the dot-com era. Because that metric uses inflation-adjusted average earnings over the past decade, a 40x reading implies investors are willing to pay $40 for each $1 of long-run average profit. Historically, levels like that have appeared only around 2000.

BlackRock argues that long-duration valuation measures do not tell the whole story. The 12-month forward P/E gives a different read. The S&P 500 is trading around 21x forward earnings, largely because profit expectations have also risen with stock prices. Consensus data cited in the report shows second-quarter earnings for the S&P 500 are expected to grow 23% year over year, marking a seventh straight quarter of double-digit growth. BlackRock says that kind of earnings expansion has been rare in market history. The Magnificent Seven, meanwhile, are trading at roughly 26x earnings, with profit growth expected to exceed 30% and blended earnings growth around 27.6%.

That leaves the market with a visible tension. Long-term valuation gauges are flashing a warning, but earnings growth is still giving investors a reason to pay up.

As of May 31, 2026, Morningstar data showed technology stocks accounting for 37.5% of total US equity market capitalization, above the level reached during the late-1990s internet bubble. If companies such as Alphabet, Meta and Amazon are included on the basis of their deep AI exposure even though they are not formally classified inside the tech sector, actual AI concentration may be even higher.

Leadership is also broadening beyond the traditional Mag 7. The report points to a newer market label, MANGOS, standing for Meta, Anthropic, Nvidia, Google, OpenAI and SpaceX. Morningstar’s Global Next-Generation Artificial Intelligence Index rose about 45% combined in April and May 2026 before pulling back in June.

Market concentration is one of the strongest similarities between this cycle and the dot-com period. In late 1999, a handful of companies including Cisco, Intel, Microsoft and Oracle drove the Nasdaq’s last major leg higher. Today’s AI leaders have much stronger earnings power, but if that growth falls short of what the market now expects, highly concentrated portfolios could still face a rapid correction.

BlackRock’s broader point is that calling AI a bubble is itself a major claim, because it implies AI will fail to deliver a lasting productivity boost. For investors, the key question has shifted. It is less about how much farther AI can rise, and more about how long the earnings growth behind the rally can continue.

Multicoin’s case for Solana, Hyperliquid and Zcash

The third note centers on comments from Multicoin Capital managing partner Tushar Jain, who laid out how he is thinking about the current crypto market and why he continues to like Solana, Hyperliquid and Zcash.

Jain said he still sees Solana as the right technical architecture for internet capital markets. In his view, the market needs a permissionless open network that can bring everything onto a single platform, and Solana still fits that role because of its performance and design.

At the same time, he said derivatives volume is moving toward Hyperliquid. He holds large positions in both assets and remains constructive on each. In his framework, Solana leads in spot trading and may carry spot trading for tokenized securities, while Hyperliquid is clearly ahead in derivatives. His conclusion is not to become an ideologue around one chain or one position, but to think in probabilities and own both.

Looking into 2026, he described Zcash as an especially obvious pick. Because of liquidity and market-cap constraints, the position is smaller than others, but he said Multicoin has accumulated a meaningful share of the total supply. He likes Zcash’s momentum, use case and community, saying it reminds him of Bitcoin in its earlier days. He added that when he spoke with long-time supporters during last year’s rally, many of them held on even after price fell back, which suggested to him that the move was not driven by short-term hot money.

He also made the case that Zcash, lacking cash flow or revenue, is almost pure social consensus. In his view, that does not weaken the opportunity; it increases the potential upside because, as a store-of-value asset, scale itself matters.

Multicoin also holds a HYPE position. Jain said investors should review the firm’s assumptions and draw their own conclusions, but he outlined four key inputs behind the thesis:

- a 35% compound annual growth rate for crypto derivatives, versus 45% over the past five years;

- a 32% market share for DEXs in derivatives, up from nearly zero in 2022 and 16% now;

- a 30% share of decentralized derivatives for Hyperliquid, which he described as conservative because reported volume can be inflated, while Hyperliquid’s 59% share of real open interest across the market is harder to fake;

- USDC collateral growing linearly with trading volume, assuming traders’ leverage preferences do not materially change.

What stands out in this view is not just one token call. It is the portfolio structure behind it: separate spot-market leadership from derivatives leadership, and keep room for a privacy-oriented asset with a different kind of social narrative.

Privacy AI comes down to where plaintext exists and who can see it

The fourth note shifts to privacy AI. Its starting point is simple: privacy AI is not one narrow technical path but a shared attempt to answer the same question. When a prompt leaves a user’s device, travels over a network, reaches the server running the model, and comes back as a result, where does plaintext exist, who can read it, and how can the user verify that the data is actually protected?

Most privacy mechanisms on the market are solving that same problem through different trust models.

Protocol-level privacy depends on promises from service providers. In enterprise zero-retention offerings, for example, the provider can know the user’s identity and process the prompt but promises not to store the data, with enforcement resting mainly on contracts and reputation. Anonymous proxies hide identity but not input content, so the downstream model provider can still read plaintext. TLS protects data in transit between machines, but the receiving party can still access everything once the message arrives.

Oblivious HTTP, or OHTTP, goes a step further by splitting knowledge of identity from knowledge of content. The relay can know where the request came from without being able to read it, while the receiver can process the request without knowing who sent it. OHTTP has already become an IETF standard and is starting to be used in production by some companies. But for closed-weight flagship models, the report says this may already be close to the practical limit of protocol-level privacy, because model weights themselves are the most valuable asset held by AI companies. Training a frontier model can cost tens of billions of dollars, and labs protect valuations by preserving that capability gap rather than opening up weights or full service code.

Structural privacy approaches try to replace soft trust with hardware isolation, cryptography or physical separation. Trusted execution environments, or TEE-based confidential computing, are described as one of the most commercially viable paths so far. In this design, model inference runs inside a hardware enclave, effectively a sealed region inside the chip. Even the server operator cannot directly inspect the data there. The chip then produces attestation, a form of remote proof, so the user can verify that a specified model and codebase are what actually ran.

TEE still has limits. The prompt is only protected after it enters the enclave. Before that, proxy and relay stages may still expose readable content. End-to-end encryption closes more of that gap by letting the user device encrypt the prompt directly with the enclave key, leaving intermediaries to handle only ciphertext. The tradeoff is engineering complexity, because every function that depends on plaintext has to be redesigned.

Fully homomorphic encryption, or FHE, and multi-party computation, or MPC, push the idea even further by trying to remove trusted parties altogether and let servers compute directly on encrypted data. The difficulty is cost. Transformer models involve heavy and complex computation, and FHE inference remains far more expensive than ordinary inference. The report says encrypted inference costs can run tens of thousands of times higher than plaintext computation. Specialized hardware is advancing, but large-scale commercial use still appears some distance away. Local inference is the most complete privacy model because the model runs on the user’s own device, avoiding servers, relays and external leakage altogether. Its downside is model capability and hardware cost.

The research then expands the problem from chat to agent workflows. Current privacy inference systems mainly protect data between a prompt and a model. But AI agents need to call outside tools such as calendars, databases, search engines and enterprise systems. Each of those calls creates a fresh point where plaintext may be exposed. Even a fully local agent still has to query external services if it needs information outside its training data, and those services often cannot fulfill the task without seeing the query in readable form.

Today’s mainstream solutions remain largely protocol-based, such as routing tool calls through a central gateway that strips identity details, controls permissions and records behavior before requests are sent onward. That still depends on trusting the service provider, because the tool server usually has to read the plaintext query. Structural approaches attempt to run tools such as MCP servers inside a TEE and let users verify privacy claims through attestation. But that protects transport and execution boundaries, not necessarily the final service provider’s ability to inspect what it receives. Open-ended search and complex agent workflows remain especially difficult because encrypted search still runs into performance and cost constraints.

The report argues that the next big value-capture opportunities in privacy AI may sit in unresolved areas: training loops that can run inside enclaves, end-to-end protected tool calls, and search systems that do not require exposing query content. Solving any one of those hard problems could create infrastructure that is much harder to commoditize.

After tokenized gold, RWA is being pushed toward real yield

The final section looks at tokenized real-world assets and asks what comes after getting assets on-chain in the first place. Most on-chain RWA remains concentrated in low-risk assets such as US Treasury bills, though expansion into equities and other categories is underway. Gold stands out as the largest tokenized commodity and one of the clearest case studies in how traditional assets move on-chain. Total on-chain gold has already exceeded $4.9 billion.

But the report says most existing tokenized gold products remain basic. They largely allow users to hold spot gold on-chain, without creating mechanisms that turn those holdings into productive assets. That leaves an efficiency gap between on-chain RWA and many TradFi products, and it limits how much practical value tokenized assets can deliver.

Under that view, the next stage for RWA is not simply more tokenized supply. It is about making those assets productive and income-generating. In gold markets, traditional finance already offers covered-call ETFs and related strategies that let investors earn option premium or hedge risk. Those products often come with higher barriers to entry, higher fees, KYC requirements, custody arrangements and broker involvement. The article cites GLDI, a more established covered-call gold ETF, as charging about a 0.65% management fee that is deducted from investor returns.

On-chain products, by contrast, can use smart contracts and structured strategies to lower access barriers and try to turn non-cash-flow assets into yield-bearing ones. Gold is used as the lead example because it is a roughly $30 trillion asset class, one of the earliest commodities to be tokenized on-chain, and one where more than $4.9 billion is already on-chain today even though most of that capital remains idle.

The article says protocols such as Enhanced are trying to bring covered-call logic on-chain to improve the capital efficiency of tokenized RWA. Gold is seen as an especially suitable starting point for three reasons: it has long been treated as a store of value; its price has recently reached fresh highs and attracted more investor demand; and it tends to move less violently than high-volatility assets, making it better suited to stable premium collection through covered-call strategies.

The logic of the strategy is simple. Investors hold spot gold and sell call options against that position to collect premium. If the gold price stays below the strike, they keep the underlying asset and the option income. If gold rises above the strike, they give up part of the upside. That makes the structure a better fit for investors who remain constructive on gold over time but do not expect a one-way explosive rally.

Enhanced’s PAXG Volatility Income Vault is described as the first product in its Thesis Vault line. It is designed to generate yield from gold volatility. Built on PAXG, the vault uses a covered-call strategy so users can continue holding tokenized gold while earning option premium.

The mechanism runs through an RFQ, or request-for-quotes, system. In the background, deposited assets are offered to market makers in batch auctions, prices are quoted, and the options trade is executed on-chain, allowing users to receive premium income up front. Participants can also sell covered calls directly against their own assets and customize parameters such as strike, tenor and direction. The model could later be extended to ERC-20 assets beyond gold.

The PAXG vault uses European-style options, which can only be exercised at expiry, and capital is locked during each cycle. Users can deposit either PAXG or USDC, with the system converting USDC into PAXG automatically. Option cycles run every two weeks, or about 26 times a year, and expected strike levels are set roughly 3% to 7% above the current gold price.

Users can choose between two return modes. In the compounding mode, premium earned in USDC is automatically converted back into PAXG and rolled into the next cycle, making it more suitable for long-term gold holders. In the income mode, proceeds are kept separately so users can withdraw USDC whenever they want, which may better suit larger holders looking for cash flow from idle gold exposure.

The problem this model tries to solve is straightforward: tokenization alone is not enough. RWA needs to create actual economic value after it moves on-chain.

Across these notes, the market is asking the same thing in different forms

Ethereum, AI equities, Solana, Hyperliquid, Zcash, privacy infrastructure and tokenized gold are very different subjects, but the research roundup ties them together through one common shift. Markets are spending less time on simple narrative momentum and more time asking where value is really captured.

For Ethereum, that means whether the base layer can capture enough of the economic activity generated across its ecosystem. For AI, it means whether earnings growth can continue to justify elevated valuations. For privacy AI, it means whether trust assumptions can be replaced by mechanisms users can actually verify. For RWA, it means whether on-chain assets can move from passive representation to productive use.

That is the broader allocation question the roundup leaves investors with: which assets or protocols can actually own settlement, preserve durable margins, or convert scale into real economic output.