China’s commercial space stocks surged on the back of the Long March 10B recovery milestone, then sold off just as quickly.

On July 13, the commercial space segment spiked and then reversed lower, ending in a broad decline. Dianke Lantian fell by more than 10%, while Aerospace Power, Xinwei Communication and Tongyu Communication also retreated. The Shenzhen Component Index and ChiNext Index both dropped by more than 2%. At the same time, previously hot AI names staged a rebound, and capital rotated out of aerospace.

That move came only days after July 10, when Long March 10B made its maiden flight and completed what the source called the world’s first rocket net-recovery operation. The announcement had lit up the entire sector. More than 30 stocks hit limit-up, and two large-cap names, China Spacesat and China Satcom, were pinned at the upper limit almost immediately.

A limit-up wave on Friday. Heavy selling by Monday. The swing was extreme.

The Long March 10B launch changed the technical picture

The article says Long March 10B was far more than a routine launch. At 12:15 pm on July 10, the rocket lifted off from the Hainan commercial launch site. It was 63 meters long and had liftoff thrust of 890 tons. Around six minutes after stage separation, the first stage returned vertically and was caught by a flexible barrier net on the “Navigator” recovery platform. According to the source, this marked China’s first controlled recovery of a heavy-lift rocket first stage and the first net-based recovery of its kind globally, making China the second country after the United States to master the technology.

Yet that development supported market enthusiasm for only one weekend. Discussion quickly shifted to why the sector rolled over, and the article places most of the emphasis on quantitative trading and the ownership structure of the board.

Who is really setting the price

Citing Securities Times, the piece says mutual funds and social security funds have long been underweight, or even absent, in commercial space stocks. It points to Sri New Material and Information Development, both up more than 100%, noting that no mutual funds appear among their top 10 floating shareholders. Aerospace Power and Aerospace Development do have some institutional participation, but overall positioning remains limited.

In the article’s telling, that leaves the sector without a broad, systematic long-only base. The shareholder structure is still fragmented. Without long-term capital anchoring prices, stocks can rise in a rush and then fall with little support underneath them.

The source says quant funds account for 20% to 30% of A-share turnover. In sectors that lack institutional base positions, that influence gets amplified. The article describes the core quant logic as volatility arbitrage: algorithms benefit from movement itself. A limit-up day and a selloff day are simply two sides of the same playbook. When a hot theme appears, algorithms move ahead of retail flows and push prices up; after retail money follows in, the models reverse and sell.

The article argues that this process has worked especially smoothly in commercial space because there are not enough long-term counterparties to absorb the selling. In a sector where public funds are largely missing, reshuffling becomes more violent.

It gives Aerospace Development as an example. On the company’s July 10 Dragon Tiger list, the top five buyers included Shenzhen-Hong Kong Stock Connect, institutions and speculative trading desks. The fifth-largest seller was East Money’s Lhasa Tuanjie Road No. 1 branch. On the limit-up day, institutions were net buyers of 85.71 million yuan, while retail traders associated with the Lhasa branch were net sellers of 18.06 million yuan.

The same stock appeared on the Dragon Tiger list eight times over the past six months. After those appearances, the average five-day decline was 10.66%, according to the article. In other words, money that entered on a board-sealing day went on to lose more than 10% on average within five trading days. The source says this is not an isolated case but part of a broader pattern in a sector where long-term capital still does not anchor pricing.

Primary capital is still betting on the sector

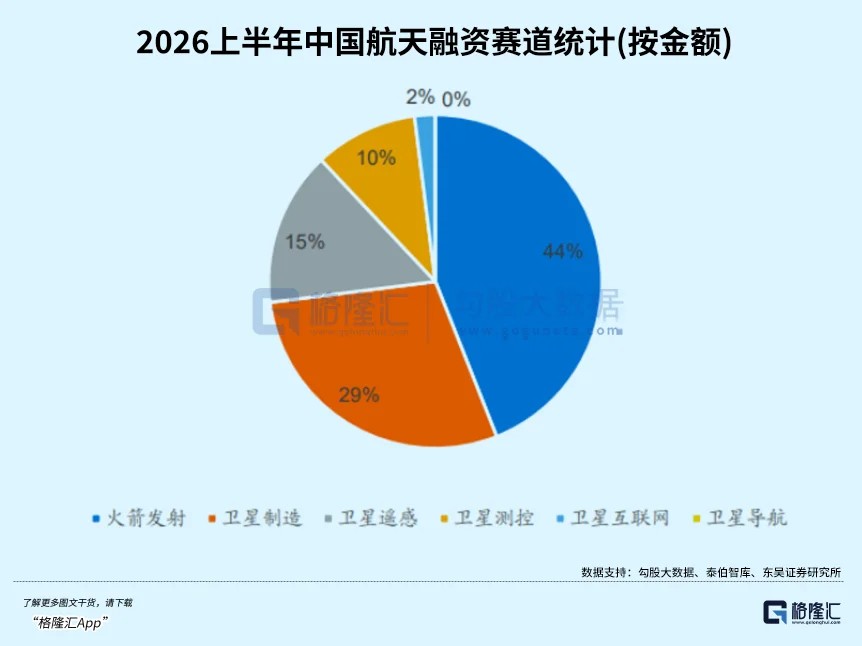

The article draws a sharp contrast between secondary-market turbulence and continued primary-market commitment. According to Taibo Think Tank, China’s commercial space industry recorded 89 publicly disclosed financing events in the first half of 2026, with total financing of 15.13 billion yuan. Rocket launch businesses accounted for 44% of that amount, the largest share among all subsectors. National and local government-guided funds, the piece says, are the main source of patient capital, and the industry is moving from “spontaneous exploration” to “state-led system guidance.”

The article then uses SpaceX as a comparison point. It says the company reached a market value of $1.77 trillion after listing this year despite a net loss of $4.94 billion in 2025. The message is straightforward: primary capital is pricing long-term space-economy potential, not near-term earnings alone.

That framework, according to the source, is tied to a projected 2.83 trillion yuan market size cited from CCID Think Tank, expected demand for tens of thousands of satellite launches within five years, and the first-come, first-served reality of orbital resources. In that logic, the income statement can wait. Orbit slots cannot.

The problem, the article argues, is that the secondary market is still operating on a different time horizon. With retail flows and quant strategies in the lead, short-term trading can drown out actual industrial progress.

Three waves over the past two years

The source says the recent drawdown looks like a quant-driven harvest if one focuses on a single trading day. Over a two-year view, though, the sector has moved through several distinct cycles.

The first wave came in early 2025, when China filed with the International Telecommunication Union for frequency and orbital resources covering 203,000 satellites across 14 constellations. The article says China had never before applied for orbital resources on that scale. The market responded by trading a “China’s SpaceX” narrative. China Spacesat’s price-to-earnings ratio climbed to 2,400x, and China Satcom issued a statement warning that a “passing the parcel effect” had become very obvious. For the author, the more lasting impact was not the price surge itself but the way it planted the idea that space is a scarce resource.

The second wave arrived in late 2025. China’s National Space Administration set up a commercial space department, which the article describes as the first dedicated national-level regulator for the field. At the same time, the fifth listing standard on the STAR Market gave unprofitable rocket companies a clearer path to financing, and LandSpace began pursuing what was framed as the first A-share listing by a commercial space company. The driver shifted from concept to policy.

That rally faded after recovery tests involving Zhuque-3 and Long March 12A failed. The policy tailwind was there, but the technology had not yet cleared validation.

The third wave came in spring 2026. Reusable rockets entered a dense testing window. Zhuque-3 Yao-2 completed a static fire. Lijian-2 completed its maiden flight. Long March 10B had originally been expected to make its maiden flight in April. At the same time, first-quarter earnings gave the market a clearer look at profit distribution across the supply chain: upstream companies were making strong money, while downstream names were deeply in the red. The driver had moved again, this time toward technical verification.

But Tianlong-3 suffered a flight anomaly after ignition, and its maiden mission failed. The April 3 explosion cooled the market again. In the three trading sessions before the latest rebound, the commercial space board had already fallen 8%, with Shenjian Co. hitting limit-down and multiple names dropping by more than 10%. Only after Long March 10B lifted off from Hainan on July 10 and completed the full loop of orbital launch plus controlled recovery did sentiment turn.

Why reusable rockets matter for valuation

The article stops short of saying a new bull phase has definitely begun. It does say the progression in market narratives is now clear: concept, then policy, then technical validation. Over the same stretch, pricing power in the secondary market appears to have shifted from speculative desks, to a mix of speculative and retail money, and now increasingly toward quant models.

That disconnect, the article argues, cannot last forever because the industrial logic is becoming simple enough to express in arithmetic. The first stage alone accounts for more than 70% of total rocket cost. Recover it, and most of the manufacturing bill can be spread out. The source says SpaceX’s Falcon 9, after 34 reuses, has reduced cost to orbit to 19,000 to 28,000 yuan per kilogram. Current launch quotes in China are 50,000 to 100,000 yuan per kilogram. LandSpace’s target for Zhuque-3 is below 20,000 yuan per kilogram. If reusability fully matures, industry estimates in the article suggest cost could eventually fall below 1,000 yuan per kilogram.

Supply and demand are also part of the case. The article lists 12,992 satellites in the GW constellation plan and 13,904 plus 1,296 in the Qianfan constellation plan, taking the total planned count above 50,000 satellites. Against that, China has only 18 commercial launch pads in operation and seven more under construction, with an average wait time of one month. Too many satellites, too few rockets. Launch capacity, in that reading, is a strategic resource.

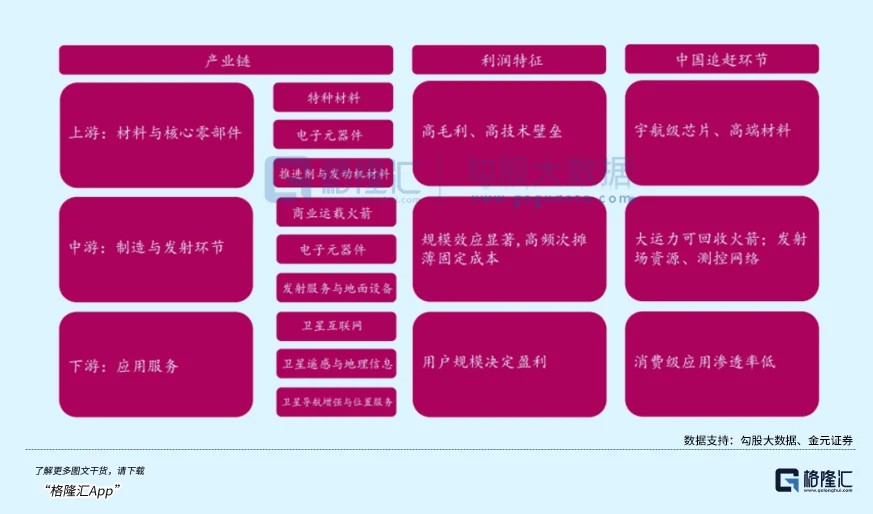

The source also cites Yuanhe Chenkun’s Research Report on the Low-Earth Orbit Satellite Internet Industry, which ranks investment priorities as complete rockets first, then satellite operators, then complete satellites, then satellite components. The logic is that whoever solves recovery first and cuts launch cost first controls the main valve of the constellation market. The article adds that China’s private rocket market may ultimately support only two or three leading companies.

Second-half catalysts will test the thesis

The sector’s industrial case will face a concentrated test in the second half of the year, according to the article. Zhuque-3 Yao-2’s recovery experiment is one of the nearest milestones. If it succeeds, it would become the first privately developed liquid rocket in China to achieve orbital-class recovery. Zhishenxing-1 is approaching its maiden launch. Tianlong-3, after its April setback, is also set to fly again in the second half. Long March 10B is expected to attempt its first reused flight before year-end. The article notes that the jump from “recoverable” to “reusable” may be no easier than the maiden success itself.

Capital-market milestones are moving in parallel. SpaceX’s post-listing valuation of $1.77 trillion, the article says, has given the global commercial space sector a benchmark line. LandSpace’s STAR Market IPO has entered the inquiry stage, and CAS Space is following behind. If those listings progress, China’s rocket companies will face a more direct public-market valuation test for the first time.

Earnings are another checkpoint. On July 12, China Spacesat released a first-half profit forecast of 30.5 million yuan to 36.5 million yuan, returning to profit year on year. The article highlights the contrast: a satellite manufacturing leader with a market capitalization in the hundreds of billions of yuan is generating only a little over 30 million yuan in half-year profit.

Upstream suppliers look different. Zhenlei Technology posted more than 400 million yuan in revenue in the first quarter, with a profit margin of 31%. BLT’s first-quarter revenue rose 40.5%, and net profit doubled. Downstream player Piesat, by contrast, saw first-quarter revenue plunge 86% and has already been placed under *ST status. The article presents this as evidence that the upstream-profit, downstream-loss split remains very much in place.

Industrial progress and market recognition are still out of sync

The piece closes on a simple distinction: a rocket launch and a capital inflow do not run on the same countdown.

Long March 10B’s successful recovery is described as a historic breakthrough for China’s commercial space industry. The key technical hurdle in reusable rocketry has been crossed, and the pathway toward lower launch costs is now clearer. From an industrial standpoint, the signal is plainly positive.

But a positive industrial signal does not guarantee instant recognition in the stock market. Volatility remains severe. A Friday limit-up frenzy followed by a Monday plunge shows that quant-led pricing has not gone away, and the profit divide between upstream and downstream companies has not narrowed either.

The article’s conclusion is that anyone looking to position for the sector needs to accept one thing first: the turning point in the industry and the turning point in pricing power are not the same event, and there is still distance between them.