China’s commercial space stocks surged on the Long March 10B launch and then gave it all back within days, putting quantitative trading back at the center of the debate.

On July 13, the commercial space sector jumped and then reversed lower across the board, according to the source article. It said CETC Lantian fell more than 10%, while Aerospace Power, Sunway Communication and Comba Telecom-linked names also dropped. The Shenzhen Component Index and ChiNext Index each fell more than 2%, while money rotated back into previously popular AI stocks.

The reversal came just after the July 10 debut flight of the Long March 10B, which the article described as a landmark event. The 63-meter rocket, with liftoff thrust of 890 tons, lifted off from the Hainan commercial launch site at 12:15 p.m. About six minutes after stage separation, the first stage returned vertically and was caught by a flexible net on the recovery platform Navigator. The report said this was China’s first controlled recovery of a heavy-lift rocket first stage and the world’s first net-based rocket recovery. It also made China the second country after the U.S. to master the technology.

Why the move reversed so quickly

The article says the answer lies in capital structure rather than in the headline itself. It cites Securities Times as saying public mutual funds and social security funds have long stayed underweight, or even absent, in commercial space equities. For example, it says stocks such as Sirui Advanced Materials and Information Development, both up more than 100%, still had no public funds among their top 10 tradable shareholders. Aerospace Power and Aerospace Development had some institutional participation, but total holdings remained limited.

Without a deep long-term institutional base, the sector behaves like a market with no anchor. Prices can rise fast when money rushes in and fall just as fast when selling starts.

The piece says quantitative strategies account for 20% to 30% of A-share turnover. In sectors where long-only institutions do not hold meaningful core positions, that share translates into greater influence. The article frames the strategy around volatility arbitrage: algorithms chase momentum on the way up and reverse into selling once follow-on buyers arrive.

It uses Aerospace Development as one example. On the July 10 trading leaderboard, the article says the top five buyers included Shenzhen-Hong Kong Stock Connect, institutions and speculative trading desks, while the fifth-largest seller was Eastmoney’s Lhasa Tuanjie Road No. 1 branch. On the limit-up day, institutional net buying was 85.71 million yuan, while retail flows associated with the Lhasa branch were net sellers of 18.06 million yuan.

The same stock had appeared on the leaderboard eight times in the past six months, according to the article, and the average decline over the five trading days after those appearances was 10.66%. In other words, buyers who entered on the breakout day historically lost more than 10% on average within five days.

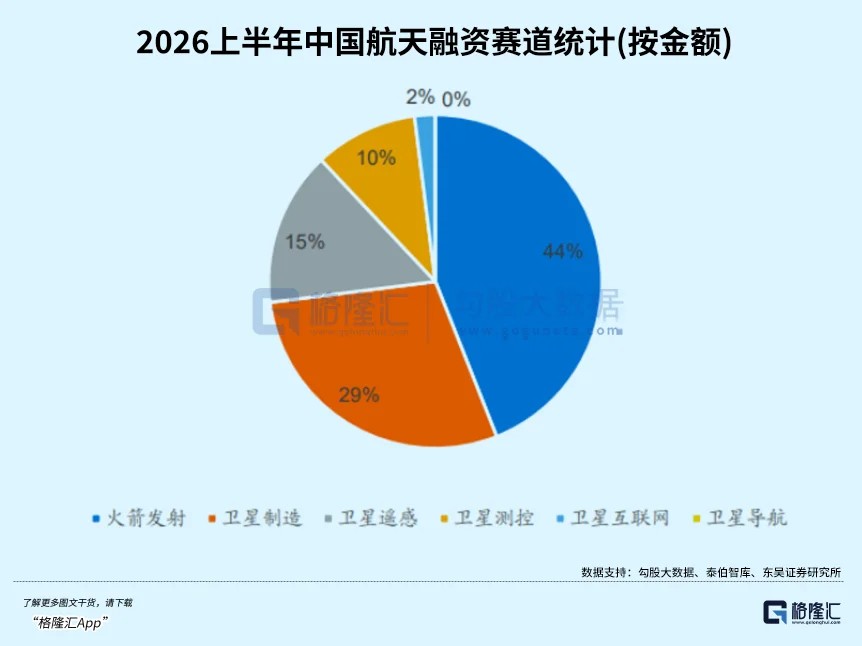

That stands in contrast with the primary market. Citing Taibo Think Tank, the article says China’s commercial space sector recorded 89 publicly disclosed financing events in the first half of 2026, totaling 15.13 billion yuan. Rocket launch companies accounted for 44% of the financing amount, the largest share among subsectors. National and local government-guided funds were described as the main source of patient capital.

Primary market pricing and secondary market pricing are not aligned

The article points to SpaceX as the clearest example of this gap. It says SpaceX reached a market capitalization of $1.77 trillion after going public this year, despite posting a net loss of $4.94 billion in 2025. The argument is that primary-market capital prices the long-term size of the space economy, including a 2.83 trillion yuan market opportunity cited from CCID Think Tank, demand for tens of thousands of satellite launches over five years, and a first-come, first-served race for orbital resources.

By that logic, investors can tolerate years of losses if a company is building launch capacity, recovery capability, user scale or orbital positioning. The secondary market, in the article’s telling, still runs on a much shorter clock and is more vulnerable to retail flows and quant-driven turnover.

The sector’s rally logic has evolved over the past two years

The source breaks the past two years into three phases.

The first came in early 2025, when China filed for frequency and orbital resources covering 203,000 satellites across 14 constellations with the International Telecommunication Union. The report says the market immediately embraced the idea of a “China version of SpaceX.” China Spacesat’s price-to-earnings ratio climbed to 2,400 times, and China Satcom later warned in a company statement that a “pass-the-parcel effect” was obvious.

The second phase arrived at the end of 2025. The National Space Administration created a commercial space division, described by the article as the first dedicated national-level regulator for the segment. At around the same time, the fifth listing standard for the STAR Market was introduced, opening a funding route for unprofitable rocket companies. LandSpace then began pushing toward an A-share listing as a would-be first commercial space stock. But failed recovery tests involving Zhuque-3 and Long March 12A cut that run short.

The third phase started in spring 2026, when reusable rockets entered a dense testing window. Zhuque-3 Yao-2 completed a static fire test, Lijian-2 made a successful maiden flight, and Long March 10B had originally been scheduled for a first launch in April. At the same time, first-quarter earnings gave a clearer look at the industry’s profit structure, with strong upstream profitability and heavy downstream losses.

That momentum was interrupted after Tianlong-3 suffered a flight anomaly on ignition and failed on its debut. The article says the April 3 explosion forced the market to turn cautious again.

Before the Long March 10B launch, the commercial space sector had already fallen 8% over the previous three trading sessions, with Shenjian Co. hitting limit down and multiple names dropping more than 10%. The July 10 launch from Hainan changed the headline flow again, as the rocket completed what the source called the first full closed-loop demonstration of orbital launch plus controlled recovery.

Valuations now face a new round of tests

The article does not say a new bull run is guaranteed. What it does say is that the sector’s drivers have upgraded in a clear sequence: concept, then policy, then technical validation.

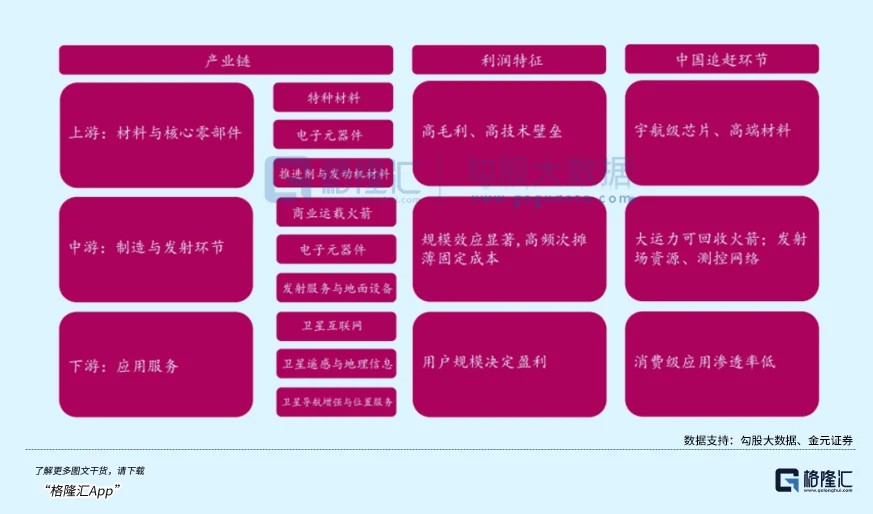

Reusable launch economics sit at the center of that framework. The piece says the first stage accounts for more than 70% of rocket cost. Recovering it means recovering that manufacturing value. It adds that SpaceX’s Falcon 9, after 34 reuses, reduced launch-to-orbit cost to 19,000 to 28,000 yuan per kilogram. Current quoted prices in China are 50,000 to 100,000 yuan per kilogram, while LandSpace’s Zhuque-3 is targeting less than 20,000 yuan per kilogram. If reusability matures, the industry estimate cited in the article puts eventual cost below 1,000 yuan per kilogram.

Demand is also large on paper. The GW constellation is planned for 12,992 satellites. The Qianfan constellation is planned for 13,904 plus another 1,296. Total planned capacity exceeds 50,000 satellites, according to the article. Supply is tighter: China has 18 commercial launch pads in operation and seven more under construction, with average waiting times of one month.

Citing Yuanhe Chenkun’s research report on low-Earth-orbit satellite internet, the piece ranks investment priorities in this order: complete rockets, satellite operators, complete satellites, then satellite components. The reasoning is simple. Whoever cracks recovery first and pushes launch cost down first controls the main valve of the constellation market. The report says the private rocket industry may ultimately have room for only two to three leaders.

The second half of the year is expected to put that thesis under pressure. The article points to the upcoming Zhuque-3 Yao-2 recovery test, the maiden flight of Zhishenxing-1, Tianlong-3’s planned return after its April failure, and Long March 10B’s first attempted reuse before year-end.

Capital markets are moving at the same time. The article says SpaceX’s $1.77 trillion valuation has already set a benchmark for the global sector. LandSpace has entered the inquiry stage of its STAR Market IPO, and CAS Space is moving in the same direction. Those listings could become the first direct public test of how China’s market values rocket companies.

Interim earnings are another checkpoint. China Spacesat disclosed a first-half earnings preview on July 12, forecasting net profit of 30.5 million yuan to 36.5 million yuan and a return to profit year over year. Upstream supplier Zhuhai Jieli Technology, by contrast, posted more than 400 million yuan in first-quarter revenue with a 31% profit margin, while BLT reported 40.5% revenue growth and a doubling of net profit in the first quarter. Downstream player Piesat saw first-quarter revenue plunge 86% and has already been marked *ST, according to the source.

Industrial progress and market pricing still run on different clocks

The article ends on a straightforward point. Long March 10B’s recovery was a historic breakthrough for China’s commercial space industry. It crossed a key technological threshold and made the path to lower launch costs more concrete.

That does not mean the stock market has accepted the sector on the same terms. Volatility remains extreme. Quant-led pricing has not gone away, and the gap between profitable upstream suppliers and loss-making downstream operators is still wide. For now, the source argues, the industry’s inflection point and the market’s pricing inflection point are not yet the same event.