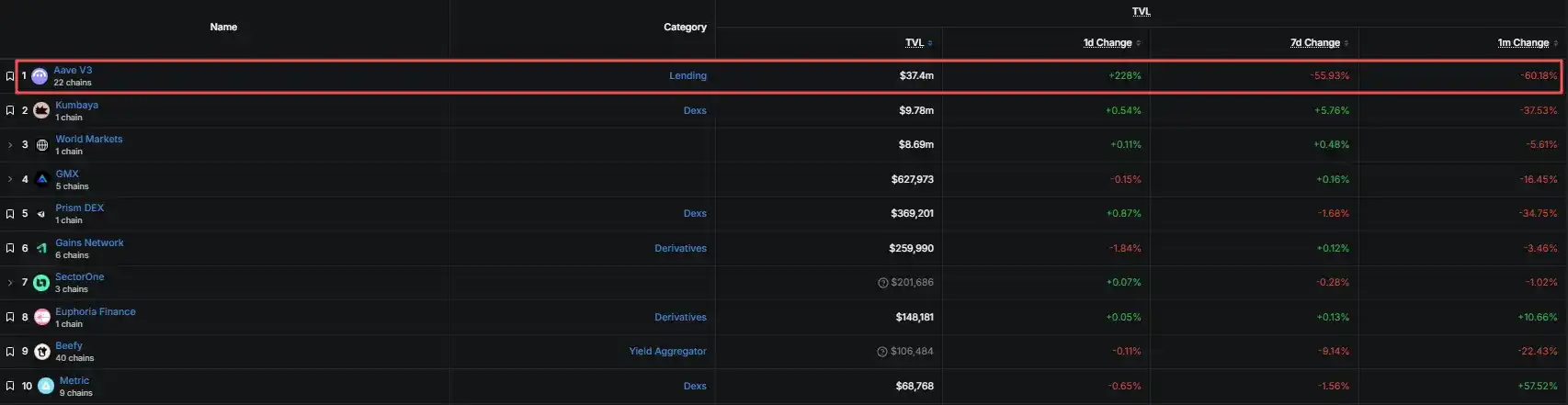

TVL swings sharply as Aave pulls liquidity

MegaETH’s total value locked saw a violent move between July 9 and 10, according to DefiLlama data cited in a report by ChainCatcher author Zhou published by MarsBit. TVL briefly fell to a little over $30 million, down nearly 60% in 24 hours and about 70% from its May peak. Aave V3, the chain’s leading protocol, removed 80% of its liquidity within a day.

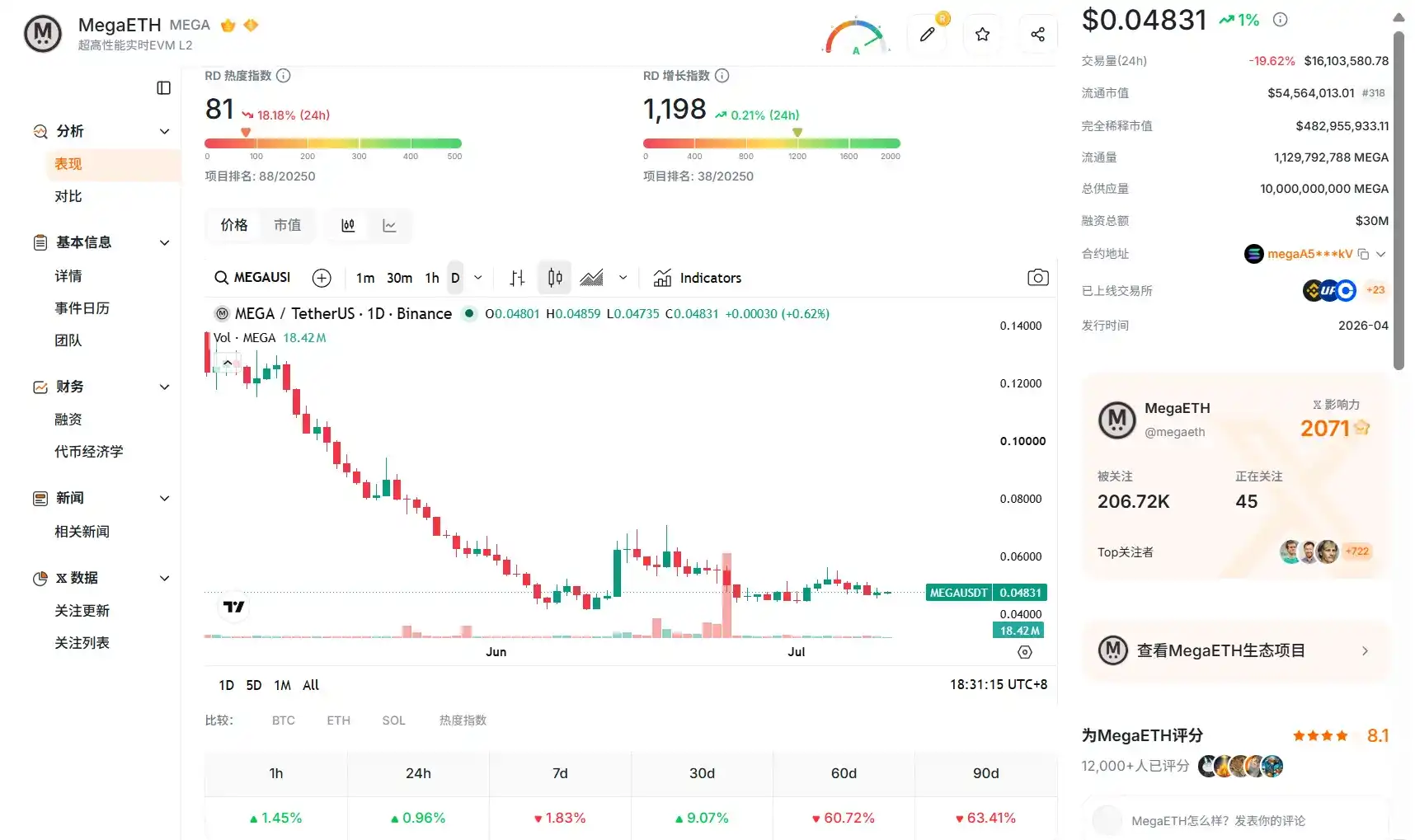

MEGA fell to around $0.048, leaving the token with a market capitalization of about $54 million and a fully diluted valuation of roughly $480 million.

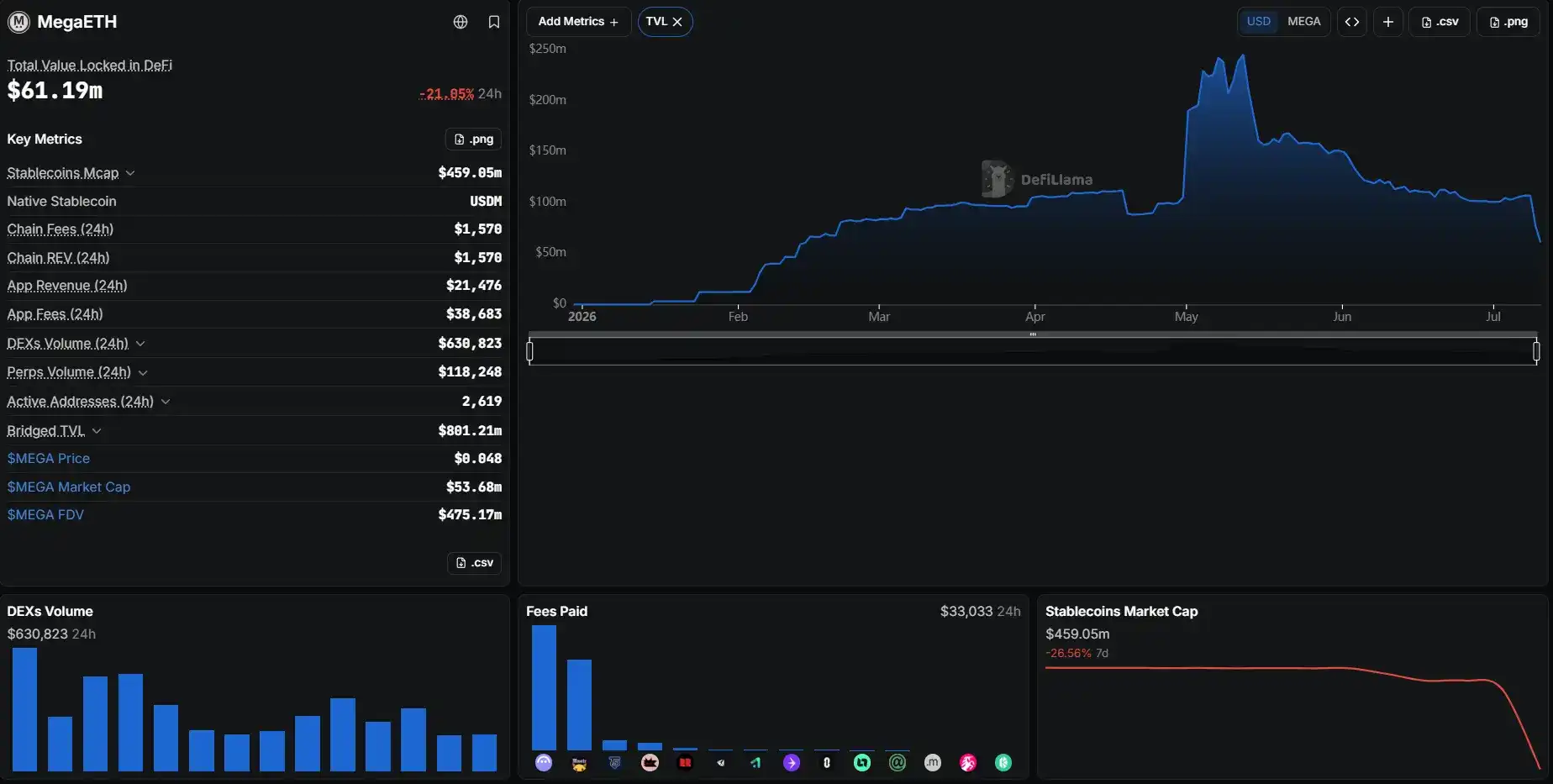

MegaETH had been one of the most anticipated new Layer 1-style public chains in this cycle. At launch, it benefited from strong venture capital backing and heavy KOL-driven participation, with FDV at one point reaching about $2 billion. In May, its DeFi TVL climbed to $245 million, briefly placing it 11th among public chains by TVL.

That rise has reversed quickly. Within a few months, MegaETH went from a highly favored new chain to one facing a steep pullback in on-chain capital, raising fresh questions about what now anchors its valuation.

TVL concentration and looped strategies come into focus

At its peak, Aave accounted for roughly 90% of MegaETH’s TVL. Total TVL is now fluctuating around $60 million, and Aave still represents about 65% of that amount.

Two months earlier, the biggest source of TVL was different. On the day MEGA listed, native DEX protocol Kumbaya held $59.03 million of the chain’s $98.43 million TVL, or about 60%.

Aave V3, GMX and Chainlink Scale went live around the same period, and Aave later became the dominant TVL driver.

Risk assessment firm LlamaRisk had previously said MegaETH’s TVL was heavily dependent on Aave, while its stablecoin base was concentrated in USDm and USDe. In LlamaRisk’s view, once native assets are excluded, a relatively large share of external assets entering MegaETH comes through third-party and specific-asset channels, leaving funding sources, asset types and protocol routes concentrated and raising questions about stability.

The report says market participants have widely questioned how much of this TVL came from Ethena-related stablecoin looping strategies, where users repeatedly post stablecoins as collateral, borrow against them, and re-pledge the borrowed assets to increase leverage and inflate headline balance-sheet figures.

Under that setup, if USDe yield drops below Aave borrowing costs, the spread disappears. The looping trade unwinds, and capital leaves with it. The report notes that whether capital came for listing-point incentives or spread capture, such flows are yield-driven by nature and usually depart once returns fade.

The bigger issue, it argues, is what remains on MegaETH after that high-concentration capital exits, and whether what is left can support the token’s valuation.

Three gaps between valuation and fundamentals

1. Valuation versus actual usage

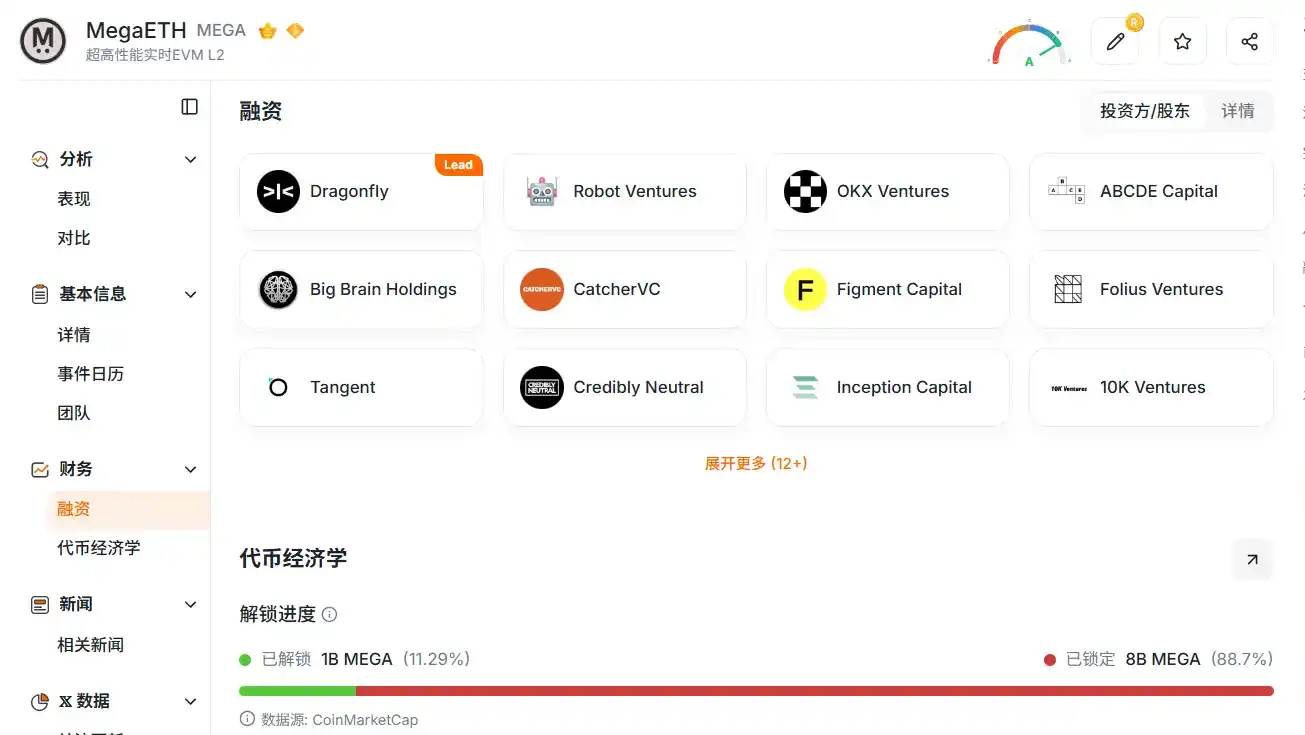

As of publication, MEGA had a market cap of about $54 million and an FDV of about $470 million, according to the report. RootData shows that 88.7% of the token supply is still not circulating, and many holders remain subject to a one-year lockup, leaving potential sell pressure ahead.

Usage looks much smaller than the valuation implies. The chain’s protocols generated less than $900,000 in real revenue over the past 30 days, or around $10 million annualized, while daily active addresses stood at 2,619.

That works out to about $180,000 in FDV per daily active address. Monthly real protocol revenue per address was still below $350. The report’s conclusion is that MEGA is not currently anchored by present economic activity on the chain, but by expectations for future growth, and that expectation is weakening.

2. Token narrative versus ecosystem quality

Buyers were paying for a high-performance DeFi chain story. The revenue breakdown tells a different story.

DefiLlama data in the report shows that Monster, a physical trading card game, was the highest-revenue protocol on MegaETH, generating about $670,000 over 30 days and accounting for nearly 80% of all protocol revenue on the chain. Aave, despite carrying the DeFi narrative and once representing about 90% of chain TVL, generated only about $90,000 over the same period.

A similar mismatch appears in stablecoin activity. Native stablecoin USDM had an outstanding supply of about $460 million on MegaETH, yet daily DEX volume was only about $630,000, and one-day perpetual futures volume was just about $120,000. That stock is also shrinking: USDM market capitalization fell more than 26% over the past seven days, which the report says may say more about real capital outflows than TVL alone.

A long-term participant identified as @OlricOnlyfornft said MegaETH had a strong early community, but the team stayed more focused on technology and applications and did not communicate enough with users. In that account, several promising projects later moved to other chains, and only a small number are still building there today.

The report stops short of treating those comments as proof on their own. Still, it says MegaETH needs clearer examples of successful applications if it wants to demonstrate ecosystem quality after the hype has faded.

3. Short-term expectations versus long-term delivery

At launch, MegaETH carried very high expectations. TGE, blue-chip protocol deployments, KOL-led buying and a surge in TVL all fed the early valuation anchor. Months later, the report says, on-chain delivery has not kept pace.

In February, Uniswap deployed v2, v3 and v4 on MegaETH. By publication time, Uniswap TVL on MegaETH had dropped to less than $20,000, down about 97% over seven days. Aave V3 saw its TVL rebound more than 240% in a single day, but on a seven-day basis it was still down more than 50%.

Those large inflows and outflows suggest the TVL was driven more by arbitrage capital than by durable user demand, the report said.

Not an isolated case as markets discount headline TVL

The report says MegaETH is not alone. Monad, another heavily promoted new-chain token from this cycle, has also fallen sharply. MON was trading around $0.022, down more than 50% from its November 2025 high, with a market capitalization of about $269 million.

Monad’s TVL has recently recovered on inflows into lending protocols, but the market reaction has remained muted. The report uses that comparison to argue that markets are becoming less willing to price these chains on headline TVL alone and are paying more attention to concrete value support.

In that view, the MegaETH pullback is not just a chain-specific stumble. It may also reflect a broader shift away from paying premiums for inflated TVL and star-driven narratives, and toward actual trading activity, revenue and ecosystem retention.

Competition in public chains is also getting tougher. The report notes that new entrants, including Robinhood, are continuing to draw attention and capital away from existing projects.

Users question communication as the team stays silent

Even after the sharp drop, the report says any rebound in MEGA would more likely come from a short-term recovery in market sentiment than from a meaningful improvement in fundamentals.

Taken together, the three mismatches leave MegaETH without a firm value anchor between its current market capitalization and its on-chain fundamentals.

Market mood has already turned more cautious. One view cited in the report sees the decline as a normal valuation reset after incentive capital faded. Once point incentives ended and looping arbitrage spreads disappeared, capital outflows became inevitable. MegaETH, in that framing, simply ran this model with more leverage than others and saw a more violent unwind.

On the community side, some users have kept raising questions about communication and transparency, saying Discord discussion channels have been closed, Telegram access is limited to large token holders, and the team appears in public less often than before launch.

The report also notes that these claims are largely one-sided user accounts and have not been confirmed by the project. As of publication, the MegaETH team had not publicly responded.

The next key question is whether the team can turn short-term liquidity into real usage and convert previously raised capital into visible ecosystem results. Until that happens, the report says it is hard to identify a solid reason for valuation to stabilize beyond a sentiment-driven bounce.