Robinhood’s blockchain push is really about legal structure

Robinhood’s new Layer 2 network and tokenized stock offering can be read two very different ways. On the surface, the pitch is straightforward: a large retail brokerage has launched a public Ethereum-compatible chain built on Arbitrum, with wallet support, ETH gas, bridge access, tokenized market exposure, and DeFi integration.

The analysis says the harder question sits below that interface. The assets that make the chain strategically interesting are not permissionless financial objects in the ordinary crypto sense. They are legally wrapped claims that still rely on issuers, prospectuses, custodians, authorized participant networks, sanctions and KYC controls, jurisdictional exclusions, and oracle design.

That is the core tension. The chain may be open to deploy on, and the tokens may move between supported wallets, but the instruments carrying economic meaning remain tightly tied to legal and operational rails. In that framing, Robinhood Chain is less about removing traditional financial structure than packaging it in a way that feels simpler to the end user.

Robinhood is layering infrastructure onto an existing business

The piece argues that Robinhood is not launching Robinhood Chain from a position of weakness. Instead, it is adding a new interface to a business that is already producing revenue through more established brokerage economics.

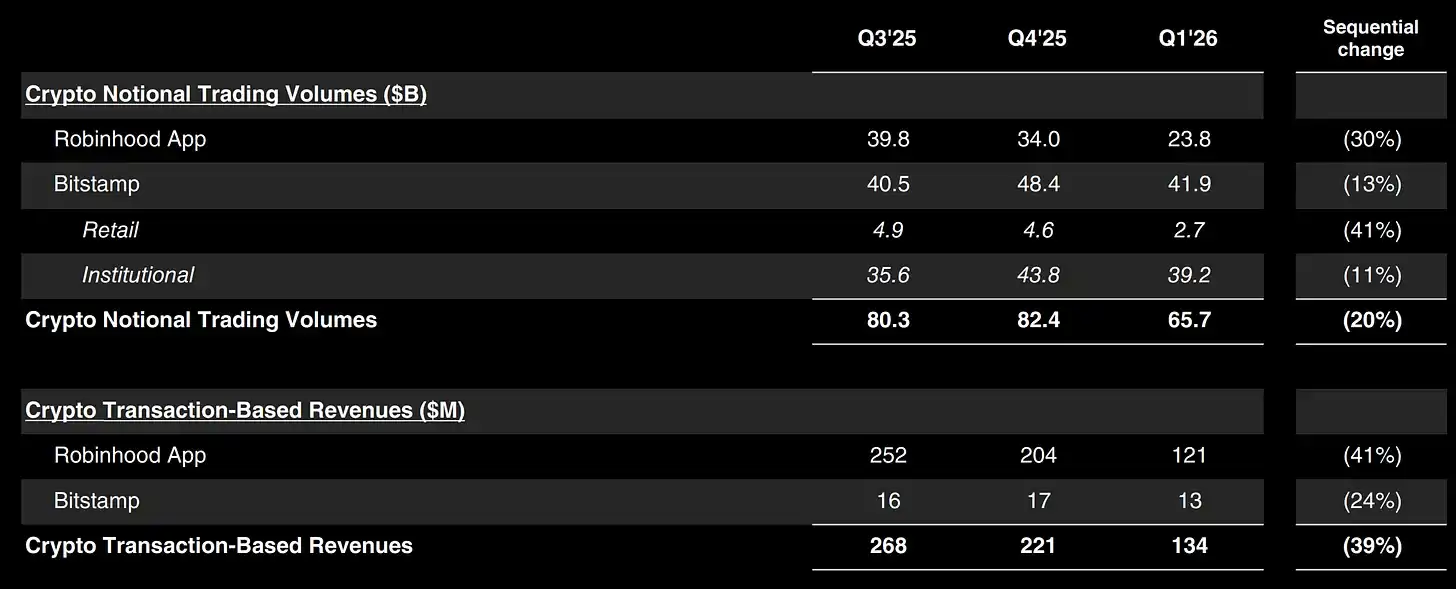

Robinhood, listed on Nasdaq under HOOD, plans to report second-quarter 2026 results after the close on Wednesday, July 29, 2026. Its first-quarter 2026 revenue mix shows where the company is making money today: options generated $260 million in transaction revenue, equities brought in $82 million, event contracts produced $104 million, other transaction revenue totaled $43 million, and crypto contributed $134 million.

The sharpest shift came from event contracts, which rose from $3 million a year earlier to $104 million. Crypto revenue moved the other way, falling from $252 million to $134 million. The analysis uses that contrast to make a simple point: Robinhood Chain is not rescuing the business. It is being built on top of a company whose earnings still come mainly from active retail trading, higher-margin products, and balance-sheet monetization.

Other operating data points in the same direction. Robinhood disclosed a $17 billion margin book, $16.7 billion in cash and deposits, $27.4 billion in retirement assets under custody, and $66 billion in crypto notional trading volume in the first quarter of 2026. Of that crypto notional volume, $42 billion came from Bitstamp and $24 billion from the Robinhood app. In the article’s reading, that makes Robinhood’s digital-asset footprint look more like infrastructure than a stand-alone retail crypto feature.

From brokerage app to financial super app

The report places Robinhood Chain inside a broader operating model that has become easier to see in the company’s recent materials. Rather than describing a set of disconnected product additions, Robinhood is now sketching a stack that includes brokerage, options, futures, event contracts, banking, Gold, retirement, crypto, wallets, private-market access, AI tools, global licenses, tokenized assets, and DeFi-linked yield.

In that stack, each business line plays a specific role. Banking and cash engagement deepen deposit relationships. Gold supports subscription take rates and premium packaging. Retirement extends the life of assets and reduces pure trading cyclicality. Futures and event contracts raise engagement and monetization intensity. Crypto offers 24/7 markets, self-custody rails, and globally portable capital. Bitstamp broadens institutional and international reach. The wallet creates a non-custodial interface. Robinhood Chain, in principle, becomes the programmable settlement layer where more of those financial actions could converge.

The company’s international moves fit the same pattern. The article points to Robinhood’s expansion into Canada through WonderFi, its disclosed regulatory progress in Singapore, and its stated UK crypto plans. Those jurisdictions matter not only as new markets, but as places where wallet-native products and tokenized wrappers may be introduced more easily than inside the regulated core of the US retail brokerage app.

What Robinhood Chain is, and what public disclosures still do not settle

Robinhood’s documentation describes Robinhood Chain as an Arbitrum Layer 2 built on Ethereum, using Ethereum blobs for data availability and ETH as the native gas token. Robinhood Wallet supports it natively, and other EVM wallets can add it manually. Assets can be bridged onto the chain through the canonical Arbitrum bridge or partner routes.

In release materials from July 2026, Robinhood said the chain was built on the Arbitrum platform to an “institutional standard,” named Uniswap as the day-one AMM, and identified Pleiades as a proprietary AMM and principal trading venue. Its technical documents add that Stock Tokens are standard ERC-20 tokens, each linked to a Chainlink price feed, with corporate actions reflected through on-chain multipliers rather than balance resets.

Still, the article says the public record is not equally complete on every infrastructure question. It finds clear documentation on connectivity, gas, bridging, token format, and oracle design, but says there is less explicit public detail on sequencer decentralization, governance path, fraud-proof status, and the exact current production roles of each named infrastructure partner.

The result is a measured conclusion. Robinhood Chain is real infrastructure, and it already has live products and named partners. What it does not yet have, the article says, is proof of durable liquidity, broad developer adoption, seamless regulatory portability, or meaningful revenue contribution.

Stock Tokens are not on-chain shares

The most important line in the analysis is also the plainest one: Robinhood’s Stock Tokens should not be described as on-chain stocks. They are tokenized economic exposure to securities delivered through a legal wrapper.

According to the public materials and prospectus documents cited in the piece, the on-chain Stock Tokens are issued by Robinhood Assets Jersey Limited and are structured as tokenized debt securities. They give users economic exposure to reference stocks or ETFs, but not direct legal ownership of the underlying securities, not beneficial ownership of those shares, and not ordinary shareholder rights such as voting.

The article contrasts that with Robinhood Europe’s earlier “Classic Stock Tokens,” which it says were legally structured as derivative contracts between users and Robinhood Europe, UAB. Those products could not be transferred to external wallets and could only be entered into or terminated through the Robinhood Europe platform. In that earlier format, the legal boundary was even more obvious: users were dealing with derivatives exposure, not tokenized holder rights.

The newer on-chain product is more aggressive in distribution while staying more conservative in legal design. Tokens can behave like crypto assets at the interface layer: transferable on-chain, held in compatible wallets, referenced in DeFi, and priced through oracles. Underneath, the claims remain prospectus-governed, Jersey-issued, secured, limited-recourse debt securities tied to reference shares.

The structure also depends on named service providers. The underlying materials reviewed in the article identify Robinhood Assets Jersey Limited as issuer and tokenizer, Bitstamp Global Ltd. as an authorized offeror in the relevant terms examined, and Alpaca Securities LLC as custodian and broker for the reference series. The point is hard to miss: the promise of portable tokenized exposure still runs through conventional financial plumbing.

Backing, securities lending, dividends, and transfer limits all matter

Robinhood’s materials say each token is backed 1:1 by the underlying stock. The analysis says that phrase is less simple than it sounds. The prospectus framework describes segregated accounts for each series, but it also allows securities lending. During the life of a securities loan, the issuer’s economic exposure may run through collateral and contractual rights rather than untouched shares sitting in custody.

That difference could matter in stressed conditions, the article argues, because it introduces borrower, collateral, operational, and recovery-value risks that many retail users would not naturally associate with a product called a stock token.

Dividends and corporate actions are also handled indirectly. Robinhood’s materials say dividends are addressed through a multiplier mechanism that adjusts the token’s reference economics, rather than through direct shareholder distributions to users. The prospectus also flags withholding-tax treatment and Section 871(m) considerations for dividend equivalents.

Transferability is real, but conditional. Robinhood says on-chain Stock Tokens can be held and transferred on supported blockchains and in compatible wallets. At the same time, the documentation allows suspensions, freezes, and restrictions in some circumstances, while purchases and redemptions remain subject to KYC, AML, sanctions compliance, and jurisdictional exclusions.

The commercial takeaway in the article is narrow but clear: the product is ambitious in distribution and conservative in legal architecture. That combination may be the only workable route to market, but it also means these tokens should be judged as an experiment in making economic exposure portable, not as a blockchain-native replacement for actual share ownership.

Crypto is becoming infrastructure, not just a revenue line

The report argues that Robinhood’s digital-asset strategy is now too broad to fit inside the old label of crypto trading revenue. Crypto still matters as a source of revenue, but its function as infrastructure is becoming more important.

That shift shows up clearly in Bitstamp. Robinhood completed its acquisition of Bitstamp in June 2025 for about $200 million in cash and framed the deal as a way to secure global exchange capability, institutional clients, white-label infrastructure, staking, institutional lending, and broader licensing coverage. In later materials, Robinhood described Bitstamp as a path into exchange lending, over-the-counter settlement, post-trade settlement, and institutional perpetuals.

The article makes the same point through Robinhood Earn. Public materials describe a simple flow: users buy USDG on Robinhood Crypto, move it into a self-custodial wallet, and then lend through Morpho. Robinhood says the wallet is non-custodial and that withdrawal timing depends on pool liquidity, while Morpho describes Robinhood Earn as a phased rollout for eligible US users. In the article’s reading, that is not just about adding yield to idle balances. It is a way of teaching Robinhood users to interact with DeFi rails through a familiar front end.

Why Lighter matters

Lighter is presented as one of the clearest examples of Robinhood’s infrastructure positioning. It gives the company access to advanced on-chain trading design without forcing it to build a crypto-native perpetuals exchange from scratch.

Public materials described in the article characterize Lighter as a custom zero-knowledge rollup with order-matching and liquidation proofs, price-time-priority execution, and an emergency exit design for cases where some operations are not processed in time. Robinhood Wallet materials also describe in-wallet perpetuals, including liquidation mechanics and funding-rate dynamics, with the underlying decentralized protocol handling liquidations.

Strategically, that helps Robinhood widen wallet engagement, test high-frequency and high-participation trading demand in a self-custodial environment, shorten product time to market, and gain exposure to the economics and user behavior of 24-hour global trading without moving the full burden back into a regulated US brokerage structure.

But it also brings risk closer to the brand. Perpetuals involve leverage, liquidation, incentive-sensitive liquidity, and retail loss risk. The article notes that Lighter’s own materials say RWA markets trade around the clock and use margin mechanisms. That may be commercially attractive, but it is also the kind of product layer that can create political, regulatory, and reputational friction for a mass-market broker.

The conclusion stays restrained. Lighter does not prove that Robinhood owns a perpetuals trading economy on the model of Hyperliquid. It shows that Robinhood can plug crypto-native trading infrastructure into its consumer wallet funnel. That is strategically meaningful, but it is not the same thing as owning the venue itself.

A simple interface still rests on a complex financial machine

The article’s final judgment is that Robinhood Chain is neither a pure crypto experiment nor a straightforward extension of a brokerage app. It is an attempt to create a new consumer-financial layer in between, one that feels intuitive at the surface while relying on highly structured, tightly controlled, jurisdiction-specific machinery underneath.

Whether that model expands depends less on the chain alone than on how users, developers, and regulators react to the gap between product language and legal reality. If users hear “tokenized stock” and assume they own stock, the distance between those two ideas could become a product-liability issue. If regulators decide the wrapper is clearly disclosed and fairly presented, the structure may grow. If they think the packaging invites confusion, the limits may appear at the exact point where the story becomes most interesting.