Investors Focus on Samsung’s July 7 Guidance as Q2 Profit Forecast Nears Historic High

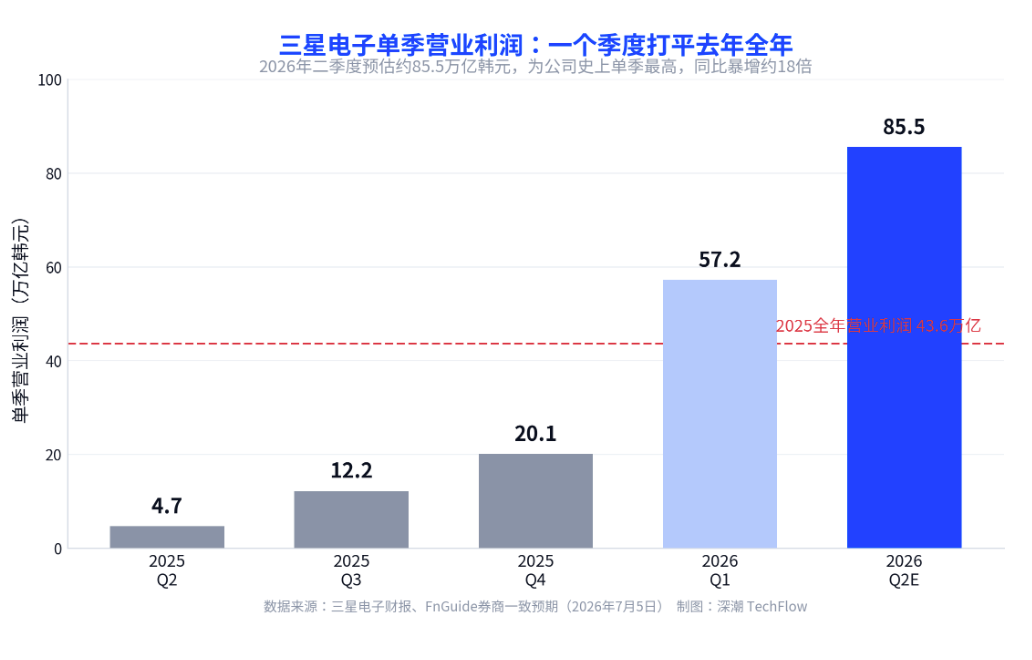

Samsung Electronics is scheduled to release its preliminary earnings for the second quarter of 2026 on July 7, and market expectations are centered on what could become a record-setting print. According to consensus estimates compiled by FnGuide, Samsung is expected to report revenue of KRW 169.4 trillion and operating profit of KRW 85.5 trillion, or roughly $55.9 billion. That would be up about 18 times from KRW 4.7 trillion in the same period last year and around 49.5% higher than the KRW 57.2 trillion reported in the first quarter.

If those estimates are confirmed, Samsung would not only post the highest quarterly operating profit in its own history, but also surpass Apple and Nvidia for the same period, potentially marking the strongest single-quarter operating profit ever reported by a global technology company. The scale of the expected earnings jump has made the July 7 preview a major event for investors tracking semiconductors, AI hardware, and upstream memory suppliers.

Looking beyond the quarter, brokerages now broadly expect Samsung’s full-year 2026 operating profit to exceed KRW 100 trillion, more than double the KRW 43.6 trillion recorded in 2025. The pace of this expansion is notable: Samsung’s first-quarter operating profit alone already exceeded its full-year 2025 total. For investors familiar with previous memory supercycles, the current uptrend is standing out not just for its magnitude, but for the speed at which profitability has inflected upward.

Semiconductor Division Drives Nearly All Earnings as AI Memory Demand Tightens Supply

Samsung’s profit mix has shifted sharply in this cycle. In the first quarter, the company reported KRW 57.2 trillion in operating profit, of which the Device Solutions, or DS, division contributed KRW 53.7 trillion. That amounts to roughly 94% of group operating profit and represented an increase of about 48 times from a year earlier. The semiconductor unit’s operating margin reportedly exceeded 70%, higher than the contemporaneous margins posted by Nvidia and TSMC.

By contrast, Samsung’s mobile and home appliance businesses saw profit decline by nearly 40% year over year, leaving the semiconductor operation as the overwhelming source of earnings. This divergence highlights how strongly the current cycle is tied to AI infrastructure spending rather than broad-based consumer demand recovery.

The immediate driver is a shortage of AI-related memory and a corresponding surge in pricing. Large technology companies continue expanding AI data centers, pulling memory supply away from traditional end markets such as smartphones, PCs, and gaming devices. Samsung memory executive Kim Jae-jun said on the company’s first-quarter call that customer demand fulfillment had fallen to the lowest level in the company’s history. Some customers, concerned about future shortages, have reportedly moved to secure capacity allocations as far out as 2027.

Prices have followed that supply pressure higher. Contract DRAM prices rose about 50% sequentially in the first quarter. In the second quarter, contract prices for DRAM and NAND flash reportedly jumped another 40% to 65%. Samsung is also said to be seeking an additional 20% increase in third-quarter DRAM contract pricing, underscoring how much negotiating leverage major memory suppliers currently hold.

Rising Memory Prices Boost Chips but Also Pressure Samsung’s Downstream Businesses

For Samsung, the pricing boom is not an unqualified positive. The company sits on both sides of the memory value chain. As a top chip producer, it benefits directly from stronger DRAM and NAND pricing. But as a major smartphone and consumer electronics manufacturer, it also absorbs higher component costs. The same price increase that appears as profit in the semiconductor division can show up as cost pressure in the mobile business.

That internal tension has become more visible as the memory rally has accelerated. Samsung’s mobile division has reportedly issued internal warnings that 2026 could become its first full-year loss since the unit was established. Core component costs now account for more than 40% of total handset manufacturing cost, according to the report. This dynamic is important because it shows that while group earnings are exploding, not all of Samsung’s business lines are participating in the upside.

The broader implication is that Samsung’s current earnings strength is highly concentrated. Investors evaluating the stock therefore need to focus less on consolidated headline profit alone and more on whether the semiconductor cycle can stay elevated long enough to offset weakness elsewhere in the group.

Bonus Accruals Could Mask Underlying Profit Power Above KRW 100 Trillion

The current consensus estimate of KRW 85.5 trillion is not necessarily the ceiling for Samsung’s operating performance. One of the biggest variables behind sell-side forecast dispersion is employee bonus accruals. Last month, Samsung management and labor reportedly reached an agreement to establish a special performance bonus for the semiconductor DS division, with accruals set at 10.5% of the division’s operating profit.

Brokerage estimates suggest the first-half bonus accrual could amount to KRW 19 trillion to KRW 25 trillion. Because that cost is recognized in reported earnings, it directly reduces headline operating profit even if the company’s underlying business momentum remains unchanged. This accounting effect has led analysts to revise estimates lower despite continued strength in pricing and shipment trends.

Korea Investment & Securities cut its second-quarter operating profit estimate from KRW 95.85 trillion to KRW 86.05 trillion based on the bonus impact. Shinhan Investment lowered its forecast from KRW 89.86 trillion to KRW 82.1 trillion. According to Shinhan analyst Kim Hyung-tae, Samsung’s actual earning power may already have moved past KRW 100 trillion if the bonus accrual is excluded.

That means investors reading Samsung’s July 7 preview may need to separate reported profit from adjusted operating profitability. The gap between the two could run into the tens of trillions of won, making the headline number less informative on its own than in a typical quarter.

Memory Upcycle Still Has Momentum, but Equity Market Is Trading Peak-Cycle Anxiety

Industry conditions suggest the pricing cycle has not yet peaked. Samsung reportedly believes the current AI-driven memory shortage could last through 2027 or even longer. As more manufacturing capacity is steered toward AI infrastructure projects, consumer electronics producers may continue to face tighter supply and elevated input costs. This has become one of the key assumptions supporting bullish expectations for Samsung’s earnings over the next two quarters.

Micron has already provided a read-through on the strength of the cycle. For the fiscal quarter ending in May, the U.S. memory maker reported operating profit of $33.32 billion, or about KRW 51 trillion, up roughly 15.4 times year over year. That result reinforced the view that the current profitability surge is not unique to Samsung, but rather reflects a broader memory market re-rating driven by AI demand.

Even so, record earnings expectations have not translated into stronger share performance. Samsung shares closed last Friday at KRW 309,500, down 4.18% over the week and roughly 17.36% below the 52-week high of KRW 374,500 reached on June 19. In early July, weakness in U.S. semiconductor benchmarks triggered a broader technology sell-off worldwide. South Korea’s Kospi at one point dropped nearly 8% in a single session, dragging both Samsung and SK Hynix into a deeper correction.

This divergence between rising profits and falling stock prices is one of the clearest signals investors are now trying to interpret. The market’s hesitation appears to reflect concern that the current memory supercycle may already be moving toward a future peak, even if reported earnings are still climbing sharply in the near term.

Two Near-Term Catalysts Could Shape Sentiment Across the Semiconductor Sector

There are at least two immediate events that may influence how the market prices Samsung and the broader Korean semiconductor complex. The first is Samsung’s July 7 earnings preview itself. Investors will be looking not only for confirmation of the record profit level, but also for guidance on the third quarter, especially any indication that memory pricing strength remains intact.

The second is the planned Nasdaq listing of SK Hynix ADRs on July 10. The offering is reported to be worth around KRW 45.5 trillion and could have a broader impact on investor sentiment toward Korean memory names. A strong reception could reinforce confidence in the sector, while a weak one might amplify concerns about cycle fatigue.

There is also a potential valuation catalyst outside memory. Reports have suggested that AI company Anthropic is in talks with Samsung over custom hardware, a development that could add a new narrative around Samsung’s chip manufacturing capabilities beyond commodity memory. Whether that story gains traction may matter if investors begin to look for reasons to support multiples even as the memory cycle matures.

For now, the market appears to be balancing two competing ideas: near-term earnings momentum remains exceptional, but the higher prices go, the more sensitive valuations become to any slowdown in AI data center spending. That is why the next several days could be critical in determining whether Samsung’s pullback is simply a mid-cycle correction or the beginning of a broader peak-cycle repricing.