Daily payouts did not stop SATA from sliding

Strive switched SATA from monthly distributions to business-day payouts on June 16 and described it as the first listed U.S. security to pay on that schedule. SATA’s annualized dividend rate is currently 13%. For July 2026, the company declared a daily payment of $0.0493 per share across 22 business days, for a monthly total of $1.0846 per share.

The change did not hold up the secondary-market price. SATA closed at $97.38 on June 22 and at $87.75 on June 26, down about 9.9% over four trading sessions. At a stated annual dividend of $13 per share, that price decline wiped out the equivalent of about 8.9 months of coupon income.

BTC holdings rose, but SATA expanded faster

The article uses a June 28 BTC spot price of about $60,005. Company holdings and share counts come from Strive’s latest SEC filing, dated as of June 18 and submitted on June 22. It notes that coverage calculations are snapshot estimates because market prices and disclosure dates are not perfectly aligned.

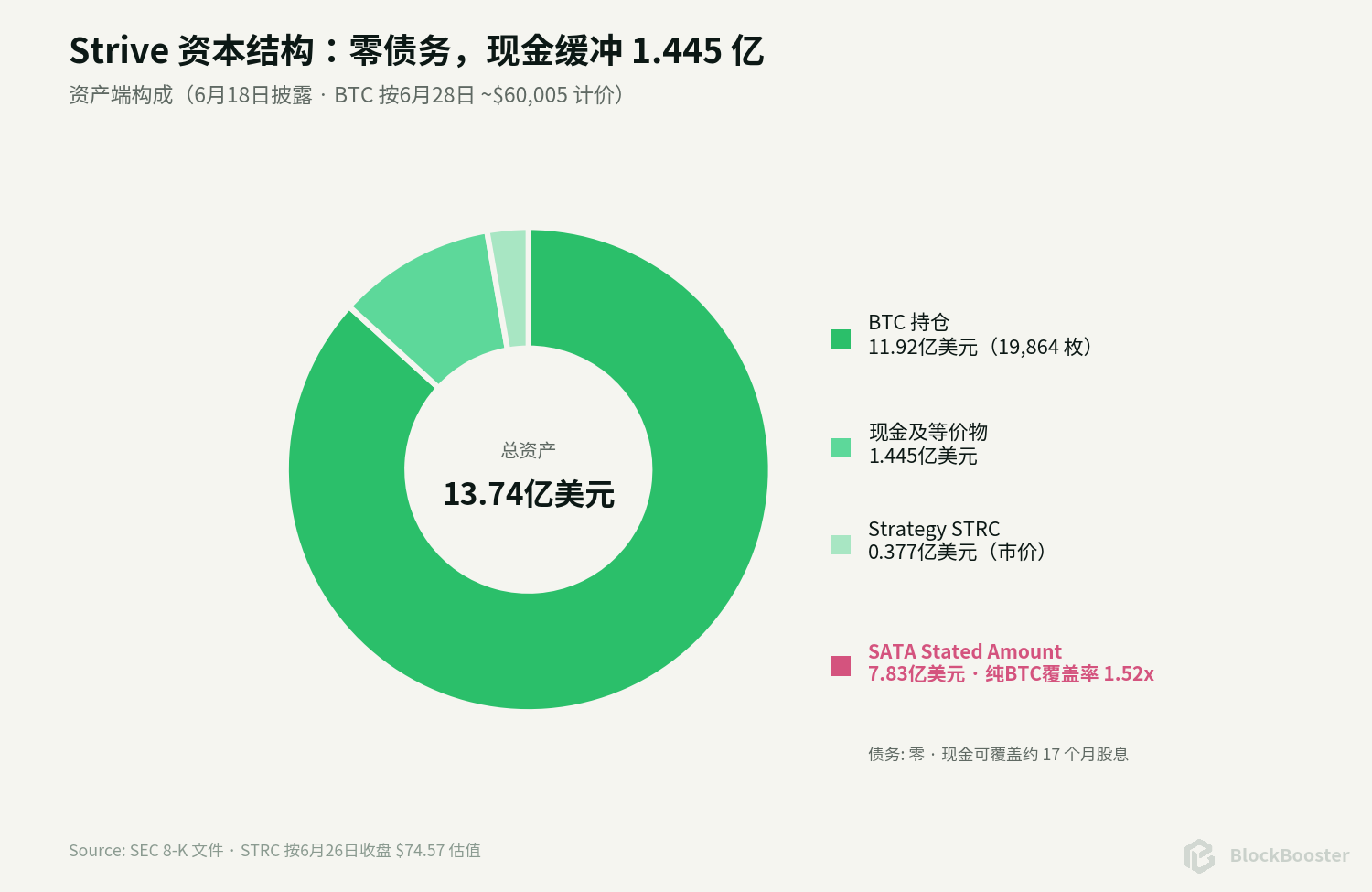

As of June 18, Strive held 19,864 BTC, $144.5 million in cash and 505,000 shares of Strategy’s STRC preferred stock. With BTC at about $60,005 on June 28, the bitcoin position was worth roughly $1.192 billion. SATA had 7,829,502 shares outstanding, which implies about $782.95 million of preferred principal using the $100 stated amount per share.

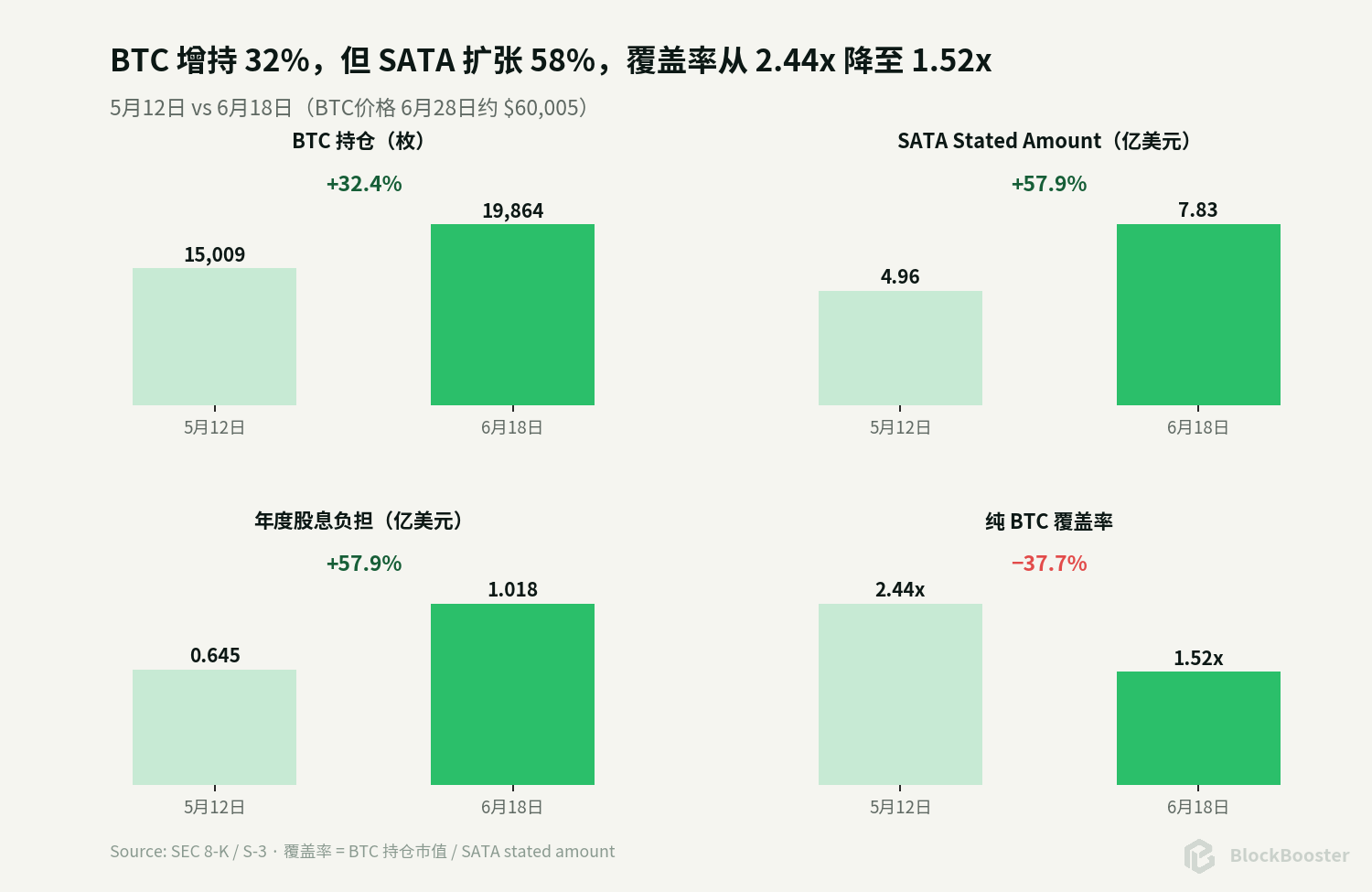

The problem is that a larger BTC count did not translate into a higher dollar value for the BTC balance sheet. From May 12 to June 18, BTC holdings increased from 15,009 to 19,864, a gain of about 32.4%. Over the same period, SATA shares outstanding climbed from 4.9595 million to 7.8295 million, up about 57.9%, while BTC fell from about $80,624 to about $60,005.

That pushed pure BTC coverage of SATA’s stated amount down from about 2.44x to about 1.52x. If BTC falls another 34.3% to about $39,416, pure BTC coverage would drop to 1.0x.

SATA is senior to common equity, but it is not a BTC-backed bond

The piece describes SATA as a perpetual preferred claim with no maturity date and dividends that can be deferred but still accumulate. It ranks ahead of common stock in liquidation, but behind corporate creditors, and it does not carry a direct lien on any specific pool of BTC.

On that basis, the article says SATA is exposed to Strive’s corporate credit and to the risks tied to a BTC-heavy balance sheet. It is not presented as a debt instrument secured by bitcoin collateral.

Cash helps, but it is not the same as collateral

Strive’s latest disclosure showed $144.5 million in cash. Using STRC’s June 26 close of $74.57, the company’s 505,000 STRC shares were worth about $37.66 million. Adding those figures to BTC, liquid assets covered SATA’s stated amount by about 1.76x.

The article draws a line between that broader liquidity view and legal collateral. Cash is not segregated for SATA holders, and STRC could also lose value during a BTC selloff or a tighter credit environment. The cash buffer lowers the odds of a forced BTC sale in the short term, but it does not remove reliance on capital markets.

At a stated amount of $782.95 million and a 13% annual dividend rate, SATA’s annual cash dividend burden comes to about $101.8 million. Looking only at dividends and ignoring operating expenses and future issuance, the $144.5 million cash balance would cover about 17.0 months. Including the STRC position at current market value would extend that period somewhat.

What daily payouts actually changed

The article treats the daily distribution schedule as a real product change. Breaking a monthly payout into business-day payments can reduce the size of each ex-dividend adjustment, cut down dividend-capture trading around a single date, smooth cash inflows and make reinvestment or spending easier for holders who want more frequent cash flow.

For July 2026, the formal declaration is $0.0493 per share each business day across 22 business days, or $1.0846 for the month. Using the current 7,829,502 share count, that works out to roughly $8.49 million of cash dividends for July if the share count stays unchanged throughout the month.

Still, the report argues that daily payouts do not remove price risk. Between June 22 and June 26, SATA dropped from $97.38 to $87.75. Over the same period, STRC fell from about $88.79 to $74.57, a decline of about 16.0%. SATA’s smaller relative drop may suggest that its higher coupon, cleaner balance sheet and novelty still command some premium, but the schedule of cash payments did not stabilize the credit price.

The market has already repriced SATA

SATA closed at $87.75 on June 26, a 12.25% discount to its $100 stated amount. Using the $13 annual dividend, its static current yield was about 14.81%. Against the latest SOFR level of about 3.64%, the market current-yield spread was about 1,117 basis points.

The article says the market is no longer treating SATA as an income product trading near par. It is now being priced more like a deeply discounted, higher-risk perpetual credit instrument.

That matters for issuance economics. If the company sells one SATA share around $87.75, it raises only about $87.75 of gross proceeds while adding $100 of stated amount and taking on a $13 annual dividend obligation. Based only on issue proceeds, the cash funding cost is about 14.81%. If the money is used mainly to buy BTC, each additional $87.75 of assets comes with $100 of preferred stated amount, which dilutes pure asset coverage.

How lower BTC prices would change the margin of safety

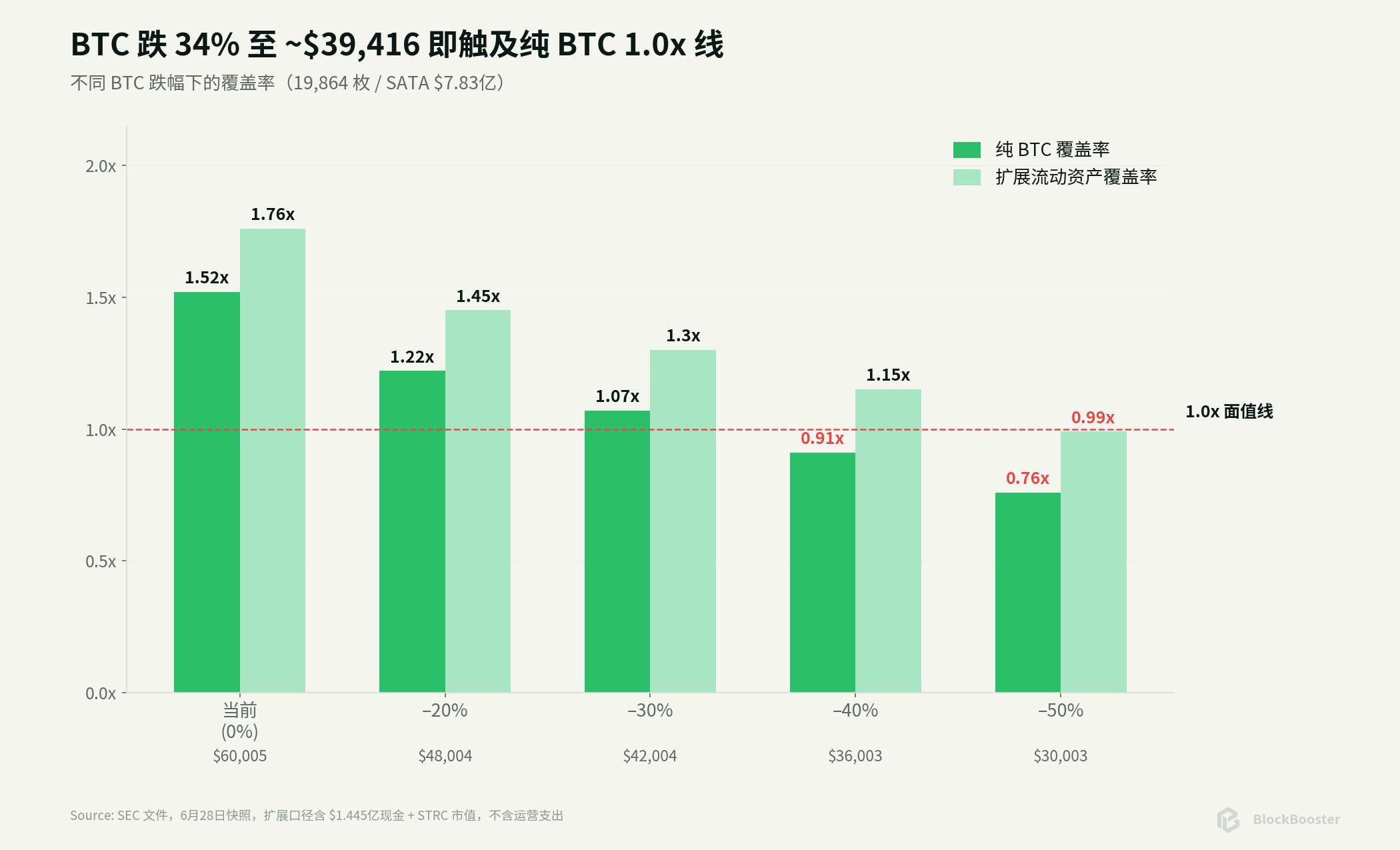

The stress test in the article starts from the current snapshot: 19,864 BTC, a BTC price of about $60,005, SATA stated amount of about $782.95 million, cash of $144.5 million and a STRC position worth about $37.66 million at current market prices.

“Pure BTC coverage” compares only the BTC position with SATA’s stated amount. “Expanded liquid-asset coverage” mechanically adds cash and the current market value of STRC, but the article says that does not represent legal collateral and does not assume STRC moves in line with BTC. It also warns that keeping cash and STRC values unchanged during a sharp BTC drawdown is optimistic.

On that basis, pure BTC coverage would fall to 1.0x at about $39,416 per BTC, or roughly 34.3% below the current $60,005 reference level. The report says that means a 1.52x coverage ratio should not be treated as a thick layer of tail protection.

It also stops short of calling that level a mechanical default line. SATA is preferred stock, not a bond with a maturity date. Even if BTC drops toward that area, the company would still have cash, other assets, access to financing and room to adjust capital allocation. The more likely path, according to the article, is earlier pressure through lower SATA market prices, weaker ATM efficiency, a higher coupon to support pricing, reduced BTC purchases, asset sales, or in an extreme case, deferred dividends.

Core risks: reflexivity, funding pressure and governance

Issuing below par

When SATA trades near or above $100, issuance is relatively efficient. At $87.75, continued issuance means taking in cash below stated amount while increasing preferred principal and dividend obligations. The article sketches a negative loop: SATA falls, funding costs rise, cash raised per share drops, coverage weakens, the market demands a higher yield, and SATA falls again.

Strive could pause or slow the ATM to avoid mechanical dilution, but that would also slow BTC purchases, weaken the market narrative and increase reliance on existing cash.

Cash flow and market access

Current cash covers about 17 months of static dividends, but that excludes operating costs and future SATA issuance. If capital markets are no longer available, the company would eventually need to choose among buying less BTC, selling securities, selling BTC, or deferring dividends.

Coupon-setting risk

The board can adjust the coupon monthly, but a weak market price limits room to move it lower. The article frames this as an internal credit reflexivity problem: a lower price pushes investors to demand more yield, and a higher coupon increases the company’s cash burden.

Preferred stock is not debt

Accumulating deferred dividends offer some protection, but a dividend suspension is not the same as a bond default. Holders may not receive timely cash and may not have creditor-style remedies. In liquidation, creditors and other senior claims are still paid first.

SATA versus STRC: no simple winner

The article puts static current yield at about 14.81% for SATA and about 15.42% for STRC, a gap of roughly 61 basis points.

It argues that the spread has to be viewed in context. Strategy is larger, has deeper funding channels and more dollar liquidity, but it also carries about $6.7 billion in convertible notes and roughly $15.5 billion in preferred stock notional, making its capital structure more complex. Strive’s latest full disclosure shows no debt, but the company has a shorter history, smaller scale and weaker liquidity. SATA offers a higher coupon and daily payouts, yet its coverage has compressed quickly. Both securities still face perpetual-duration risk, issuer call risk and BTC tail risk.

The conclusion is that investors cannot say SATA is automatically better just because Strive has no debt, nor can they say STRC is clearly cheaper just because its yield is higher. The choice depends on which risk matters more to the buyer: complex leverage at a larger issuer or funding and liquidity risk at a smaller one.

The final point

The article’s main takeaway is that the story is not really about “13% paid daily.” It is about slicing a BTC treasury company’s balance sheet into two layers: common shareholders absorb the residual volatility, while preferred holders get priority cash flow but still bear issuer credit, perpetual duration, funding-channel risk and BTC valuation pressure.

In that sense, daily distributions change the frequency of cash flow, not the risk itself. The risk remains, only expressed through coverage ratios, financing costs, duration and corporate governance rather than through spot BTC price alone.