KIS report triggers a sharp drop in SK Hynix shares

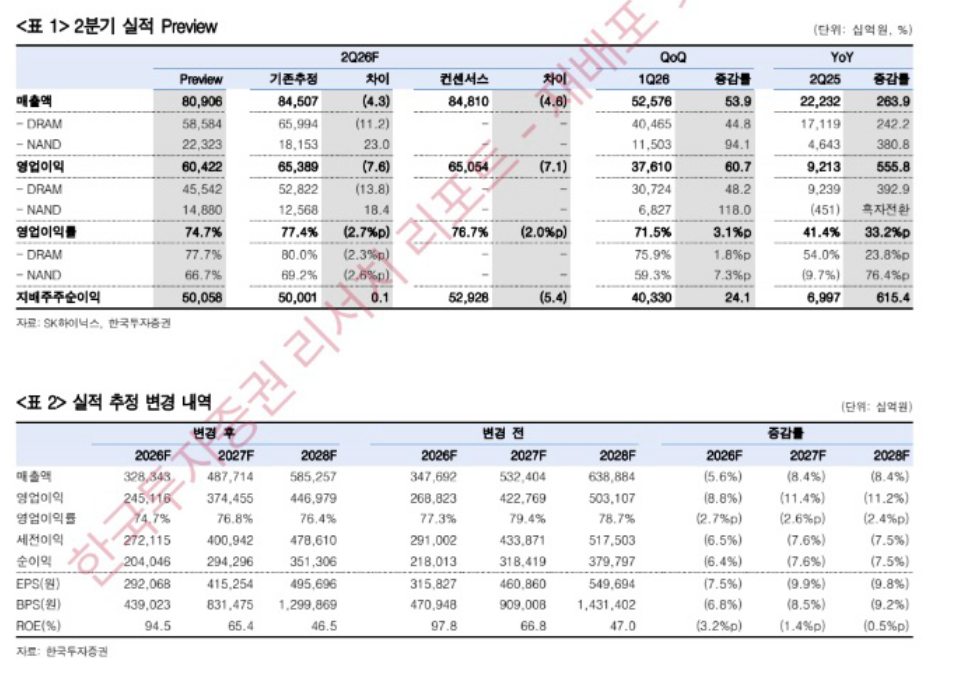

SK Hynix shares fell more than 10% after the Korean market opened on July 13, after local brokerage KIS issued a second-quarter earnings forecast that came in below market expectations. KIS projected Q2 revenue of KRW 80.9 trillion, up 54% from the prior quarter and 264% from a year earlier. It forecast operating profit at KRW 60.4 trillion, up 61% quarter over quarter and 556% year over year.

Those numbers were strong on their face. The market focus, though, was on the gap with consensus. Investors had been looking for KRW 65 trillion in operating profit, leaving the KIS estimate about 8% lower. After the report, SK Hynix fell below KRW 2 million per share. The stock was also down 33% from its June 25 record high over a three-week span.

Higher HBM exposure capped near-term ASP upside

KIS said the main reason its profit forecast fell short of consensus was SK Hynix’s higher revenue and shipment mix from HBM, or high-bandwidth memory. According to the brokerage, that mix left the company with slower average selling price, or ASP, expansion than the broader market.

The explanation rested on pricing structure. HBM is commonly sold through long-term agreements, known as LTAs, which keep prices relatively fixed for a period of time. Conventional DRAM and NAND products have more exposure to spot pricing, so their ASPs can move faster when the market rises.

In KIS’s view, SK Hynix’s heavier weighting toward HBM meant it captured less of the recent memory price rally than peers. The brokerage estimated that Q2 DRAM ASP rose about 30% quarter over quarter and NAND ASP rose about 50%, while SK Hynix’s overall ASP growth was held back by contract-based HBM pricing.

KIS says the cut reflects LTA assumptions, not weaker fundamentals

KIS explicitly said the revision was not a sign of deteriorating business conditions. It described the change as a result of recalculating its model after incorporating pricing assumptions tied to signed LTAs. The report said: "This is the result of adjusting the forecast to a more realistic level by incorporating signed LTAs into the pricing assumptions, and it is not due to concerns about earnings."

The brokerage also lowered its operating profit forecasts for 2026 and 2027 by about 9% and 11%, respectively. Even so, it argued that once HBM4 begins mass shipments in the third quarter, higher market prices should lift overall ASP and bring SK Hynix back in line with the broader market.

KIS forecast that SK Hynix’s operating margin would reach 74.6% in Q2 2026, a record high, and continue to rise each quarter after that. It kept its KRW 3.8 million target price and maintained a buy rating.

Strong growth still failed to clear the market’s bar

The report highlighted how market pricing can diverge from headline growth. Even with operating profit up 556% from a year earlier, the KIS forecast was still treated as a miss because the market had already priced in higher expectations. The difference between KIS’s KRW 60.4 trillion estimate and the KRW 65 trillion consensus was roughly KRW 4.6 trillion.

The original article said that raised two concerns for investors. One was the immediate hit from an earnings figure that did not meet expectations. The other was whether a high HBM mix could become a structural issue by limiting ASP flexibility during periods when contract prices are locked in. The article also said that SK Hynix had listed in the U.S. on the previous Friday, and some funds that had positioned for the ADR debut chose to take profits after listing, adding to selling pressure.

Sell-off spreads to Hong Kong ETFs and A-share memory names

The weakness in SK Hynix quickly spilled into related assets. In Hong Kong, the 2x long SK Hynix leveraged ETF fell more than 22% in a single day, while the 2x long Samsung Electronics ETF dropped more than 13%.

In China’s A-share market, memory-related stocks also moved lower. GigaDevice, Beijing E-Town Semiconductor, Longsys, and Biwin Storage were among the names that fell more than 7%.

The original article added that the broader memory semiconductor sector had already entered a correction over the past half month, with some stocks down more than 20%, a level it described as the line for a technical bear market. It also pointed to portfolio rebalancing across AI-related sectors and markets, including a rotation from chips into cloud plays and capital returning to Hong Kong during that market’s recent rebound.

KIS keeps a positive long-term stance

Despite the market reaction, KIS did not turn negative on the company’s longer-term setup. The brokerage said that as the memory industry shifts toward three- to five-year LTA structures, the main driver of valuation will move away from quarterly ASP swings and toward how long elevated profitability can be sustained.

KIS said in the report: "From now on, what needs attention is the sustainability of earnings. The expansion of LTAs is reducing the long-standing volatility of earnings in the memory industry."

It also argued that a larger share of contract-based revenue and supply pressure created by HBM capacity expansion could help SK Hynix sustain high profitability over time. On that basis, KIS maintained both its KRW 3.8 million target price and its buy rating.