A Prof G Media discussion translated by TechFlowPost says SpaceX joined the Nasdaq-100, collected 31 buy ratings from 32 analysts, and still saw its stock drop 12% last week. The piece frames that gap as a sign of entrenched optimism in Wall Street research, then extends the discussion to crypto’s fading appeal and mounting pressure in the U.S. housing market.

SpaceX entered the Nasdaq-100 and quickly drew bullish coverage

According to the article, SpaceX was formally added to the Nasdaq-100 last week. It qualified under a new fast-track listing rule that cut the required trading history from at least three months to 15 days and removed the minimum public float requirement. Before that change, Nasdaq-100 stocks needed at least 10% of shares in public float.

Research coverage turned heavily positive. Of the 32 analysts covering SpaceX, only one issued a sell rating. That call came from CFRA Research, which the article describes as an independent financial intelligence firm without investment banking, asset management, or trading operations.

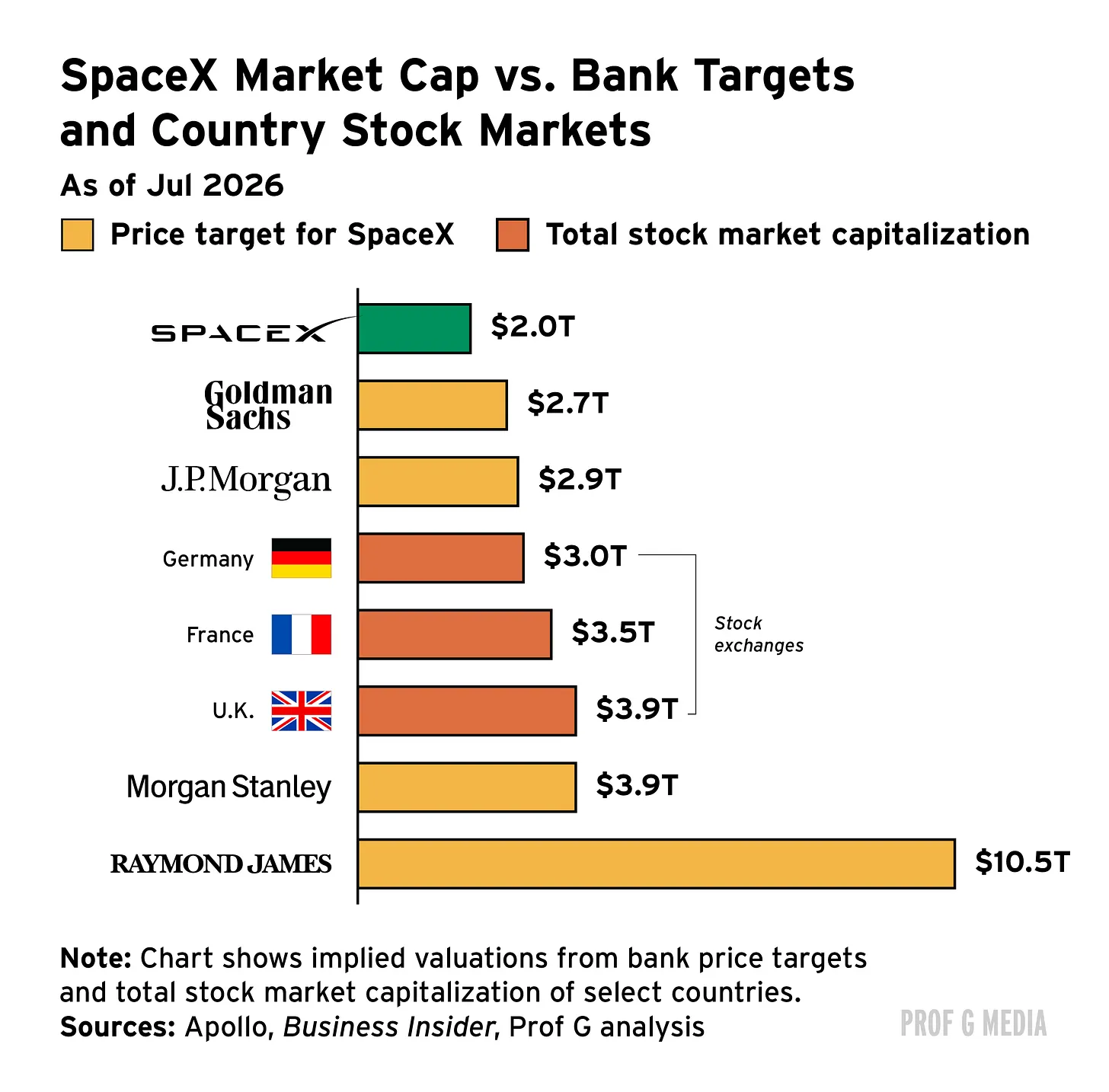

The article says target prices were notably bullish. Raymond James analyst Brian Gesuale forecast that SpaceX could reach $800 a share over the next 12 to 18 months. By the article’s math, that would require a gain of more than 400% and push the company’s market value to $10.5 trillion, roughly one-third of U.S. GDP and more than the combined stock markets of the U.K., France, and Germany.

Despite that wave of positive calls, SpaceX fell 12% last week and is down 36% from its peak.

The piece argues underwriting ties still matter in stock research

The article says academic work has long found an upward bias in analyst recommendations, especially when the bank employing the analyst has business ties to the company being covered. It points back to the dot-com era and cites Enron as a classic example: two months before Enron collapsed, 16 of 17 sell-side analysts covering the stock still rated it buy or strong buy, many of them at banks that did business with the company.

Investor protections were introduced after that period, and direct influence from investment banking divisions over bank analysts became illegal. Even so, the article says later research still found that affiliated analysts were reluctant to issue negative calls.

It adds that optimism appears to be rewarded inside the industry. Even after controlling for accuracy, more bullish analysts were more likely to move to top brokerage firms and more likely to be called on during company earnings calls. In the Global X Artificial Intelligence & Technology ETF, the article says only 2% of the 84 holdings carry a net sell recommendation.

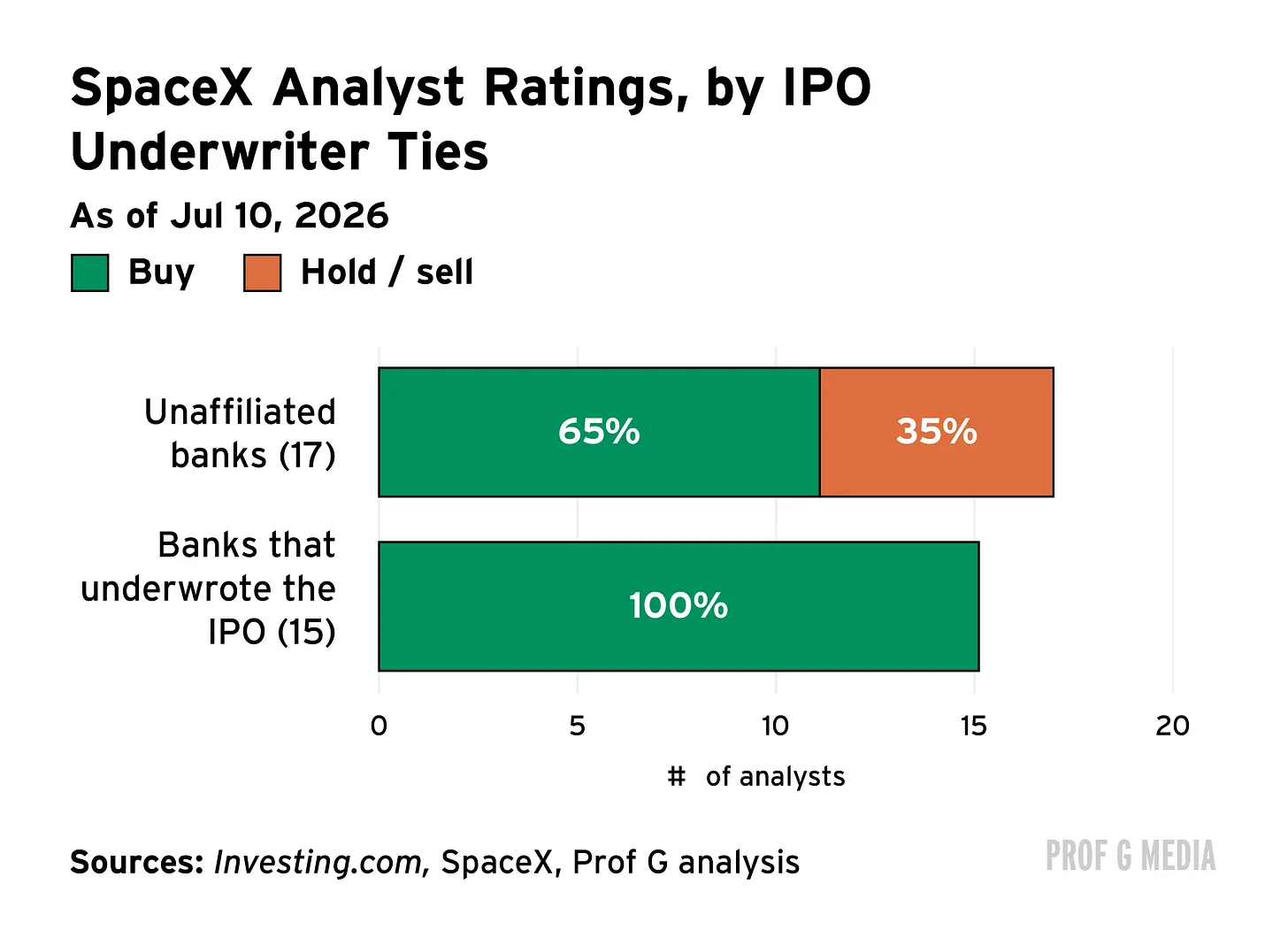

For SpaceX specifically, analysts at banks that underwrote the listing were more positive than the non-affiliated group. The article says 100% of affiliated analysts issued buy recommendations. Among the 17 analysts whose firms did not underwrite the listing, 65% did so.

Morgan Stanley’s price target is singled out

The piece takes direct aim at Morgan Stanley’s $300 price target, saying it was double the then-current stock price. At the same time, Morgan Stanley also outlined a $600 bull case and a $75 bear case. The article’s conclusion is blunt: if the stock could fall 50% or rise 300%, the forecast is not saying much at all.

It argues that structural conflicts in equity research remain hard to remove. If a bank assigns a sell rating to a company, that company may be less inclined to work with the bank on an initial public offering, where underwriting fees can reach 1%. In that setup, the article says, companies have every reason to prefer banks that are friendly to them.

The article also notes that the U.S. Securities and Exchange Commission introduced a rule in 2003 to separate research operations from the banking side that wins underwriting fees, and says that rule was terminated seven months ago. Former SEC chair Arthur Levitt later wrote a Wall Street Journal opinion piece titled “The SEC Could Let Wall Street Analysts Get Corrupt Again,” warning about the consequences of removing the rule.

At the same time, the article says analysts do not carry the same media power they did in the 1990s, when they were constant fixtures on CNBC. There are now many more places investors get information. Still, it describes some of today’s price targets as embarrassing.

On valuation, the piece questions whether extreme sales multiples make sense. It says no company trades at 100 times sales in a durable way, and that the firms that can sustain high price-to-sales ratios are usually software companies, where revenue converts to profit with less fixed cost. SpaceX, by contrast, is described as carrying huge expenses, including rockets and NVIDIA GPUs. The article also says the company’s growth rate is close to 15% and its market share is 3.5%, arguing that the AI label is mostly hype.

Crypto has lost value and, in the article’s view, cultural momentum

In a section titled “Bro Capital Rotation,” the article says the crypto market has erased more than half of its value over the past eight months, while Bitcoin ETFs have seen $8 billion in outflows over the past eight weeks. AI, it says, has replaced crypto as the technology theme drawing the strongest excitement and the same sense of disruption.

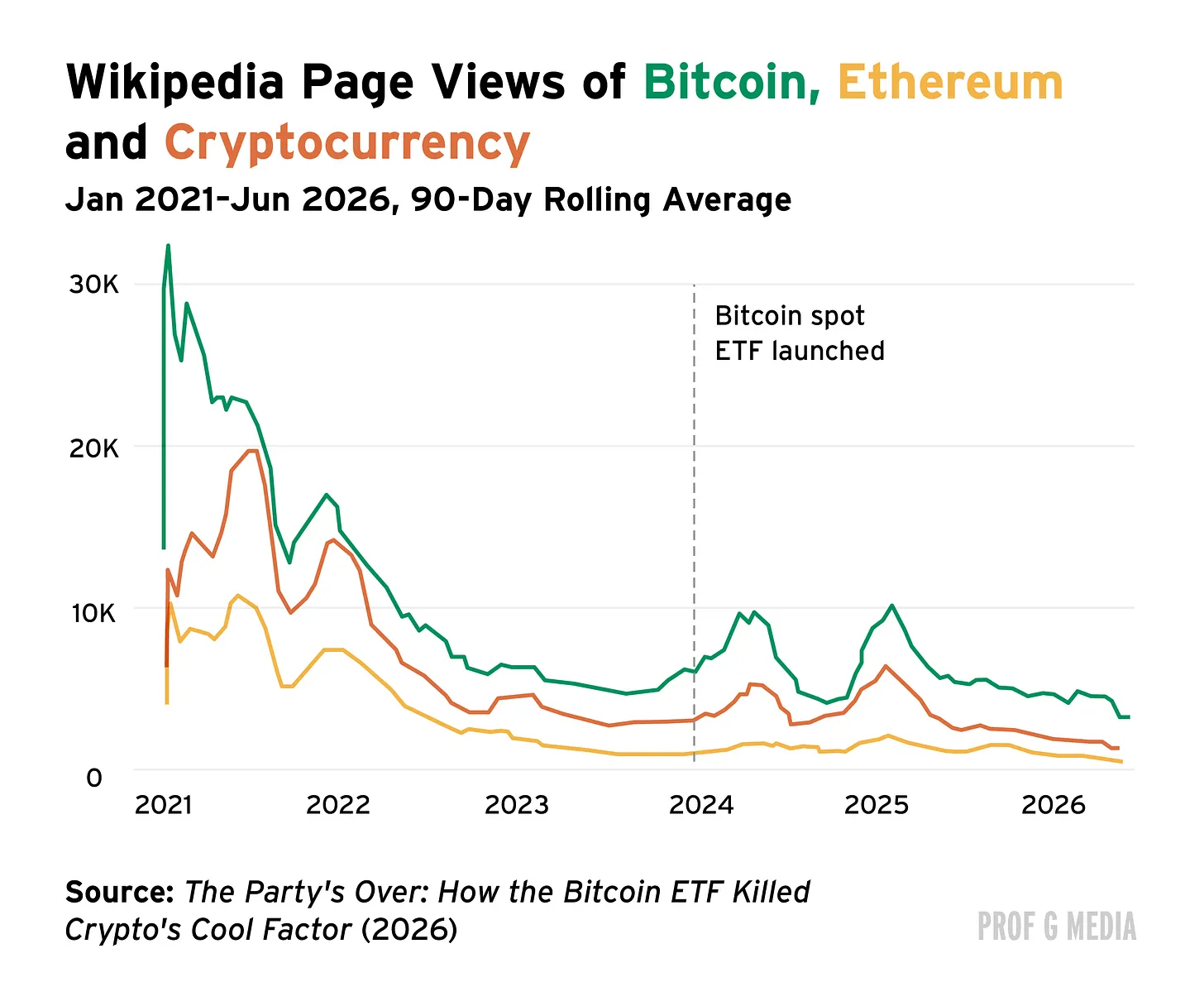

The piece cites a paper by Marquette University finance associate professor David Krause, who places the turning point for crypto’s loss of “cool factor” in January 2024, when the first Bitcoin ETF launched. His argument, as summarized in the article, is that once Wall Street made crypto simple and mainstream, it stopped feeling subversive.

Using search activity and Wikipedia traffic as proxies for public interest, Krause found sharp declines after the ETF launch. Through June 2026, the article says Google searches for Dogecoin were down 63%, searches for “cryptocurrency” were down 47%, and visits to the two related Wikipedia pages fell 76% and 56%, respectively.

The article also offers a broader cultural reading: once major political and business figures are openly aligned with crypto, Bitcoin no longer looks anti-establishment in the way it once did, and its use-case narrative has weakened.

U.S. housing shows the cost of belief in ever-rising prices

The final section turns to housing. Last month, the median U.S. home price reached a record $408,800. In April, the National Association of Realtors reported that first-time buyers accounted for 21% of purchases, the lowest share since the group began tracking the figure in 1981.

The article says 75% of homes on the market are now unaffordable for a typical household. For younger Americans, the picture is worse. From 2019 to 2024, inflation-adjusted median home values rose 30%, while inflation-adjusted median household income for people under 40 rose just 9%.

Demand, though, has not disappeared. The article says 56% of Americans view homeownership as part of the American dream, and nearly two-thirds of non-homeowners want to buy within five years. Affordability problems are also delaying other life decisions: nearly one in five prospective buyers say they are postponing marriage or having children until they own a home, while 17% are delaying career changes or getting a pet.

The piece cites a Moody’s comparison between two people earning $150,000 a year. One buys a $500,000 home with a 20% down payment and a 6.25% mortgage rate. The other rents for $2,500 a month, with rent rising 3% a year, and invests the difference at a 10% return. After 30 years, assuming average annual rent and home-price growth, the renter ends up with a net worth of $2.8 million versus $1.6 million for the homeowner. The analysis does not account for taxes.

The article’s closing point is that housing, much like crypto, is often supported by a simple belief: prices will keep rising. It argues that a house should only be expected to be worth more in five years if the owner improves it or if the specific neighborhood becomes more desirable.