Bitwise Head of Research Ryan Rasmussen picked five charts from the firm’s second-quarter crypto market review to explain a market that looked divided in 2026. Business revenue, real-world asset tokenization and institutional positioning all improved, while major crypto asset prices moved lower.

The review, according to the article, includes more than 50 charts covering market performance, on-chain fundamentals and institutional adoption. Rasmussen said these five were the most important if readers wanted the core takeaways quickly.

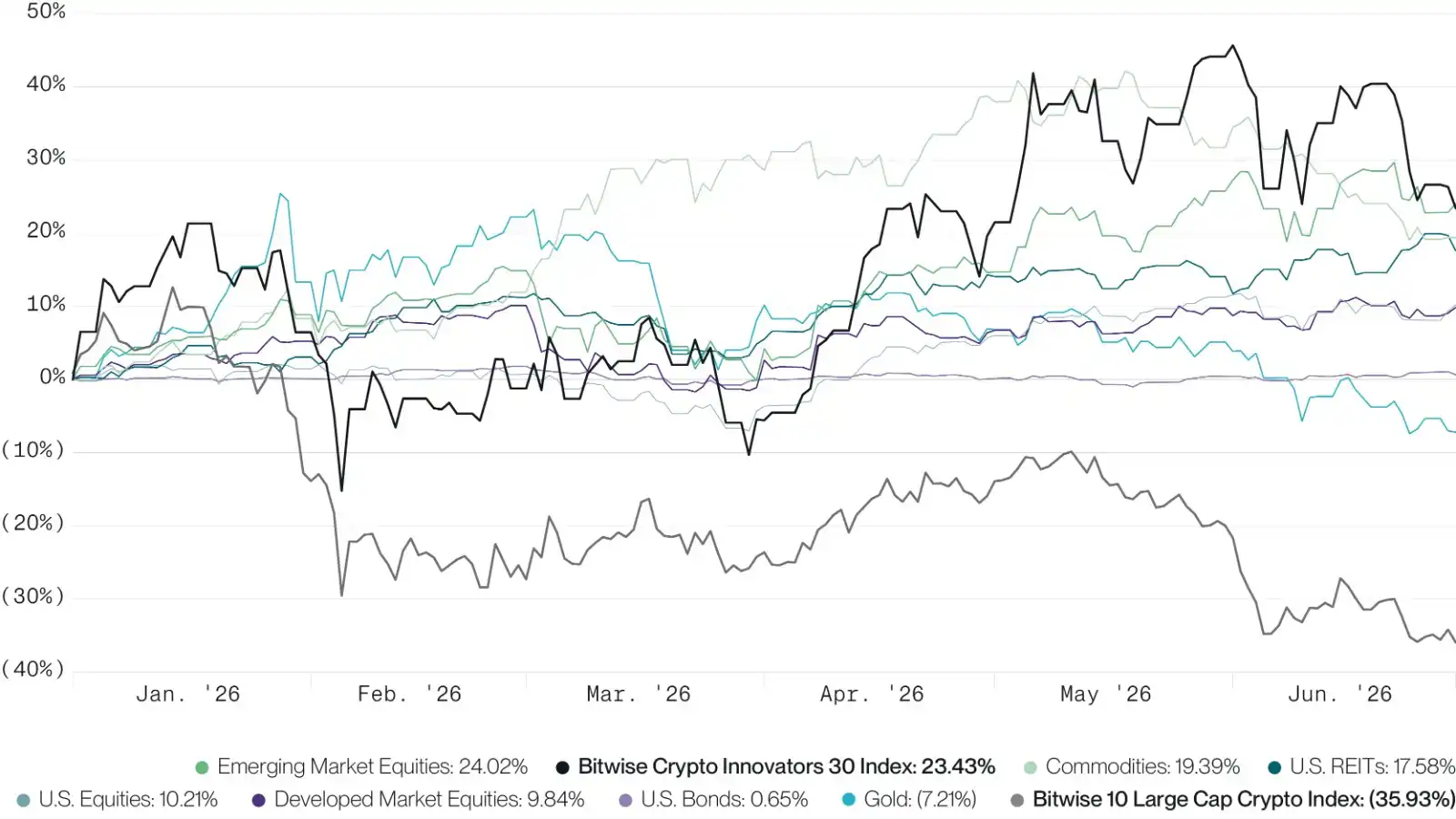

Crypto equities rose while crypto assets fell

In the first half of 2026, the broader crypto asset class fell 36%. Gold was the only other major asset class that also declined, down 7%, while the rest posted gains. Rasmussen said that helps explain why this bear market has felt especially difficult: pressure has been concentrated in crypto itself.

Crypto-related equities moved in the opposite direction. They gained 23% in the first half, outperforming every major asset class except emerging market stocks. The Bitwise Crypto Innovators 30 Index, which tracks 30 leading publicly listed crypto companies, returned more than twice as much as the S&P 500.

Rasmussen said the data points to a clear message. Even in a bear market, the crypto industry still offers investable opportunities. He cited bitcoin mining companies benefiting from the AI boom, stablecoin issuers and tokenization platforms taking on Wall Street business, and a deeper overlap between traditional finance and crypto markets.

He added that he expects a recovery in crypto prices in the second half of the year, though the first-half performance already showed that crypto is not a single asset category. It is a broad field with multiple tracks and different growth drivers, he wrote.

The comparison was based on data from Bitwise and Bloomberg through June 30, 2026.

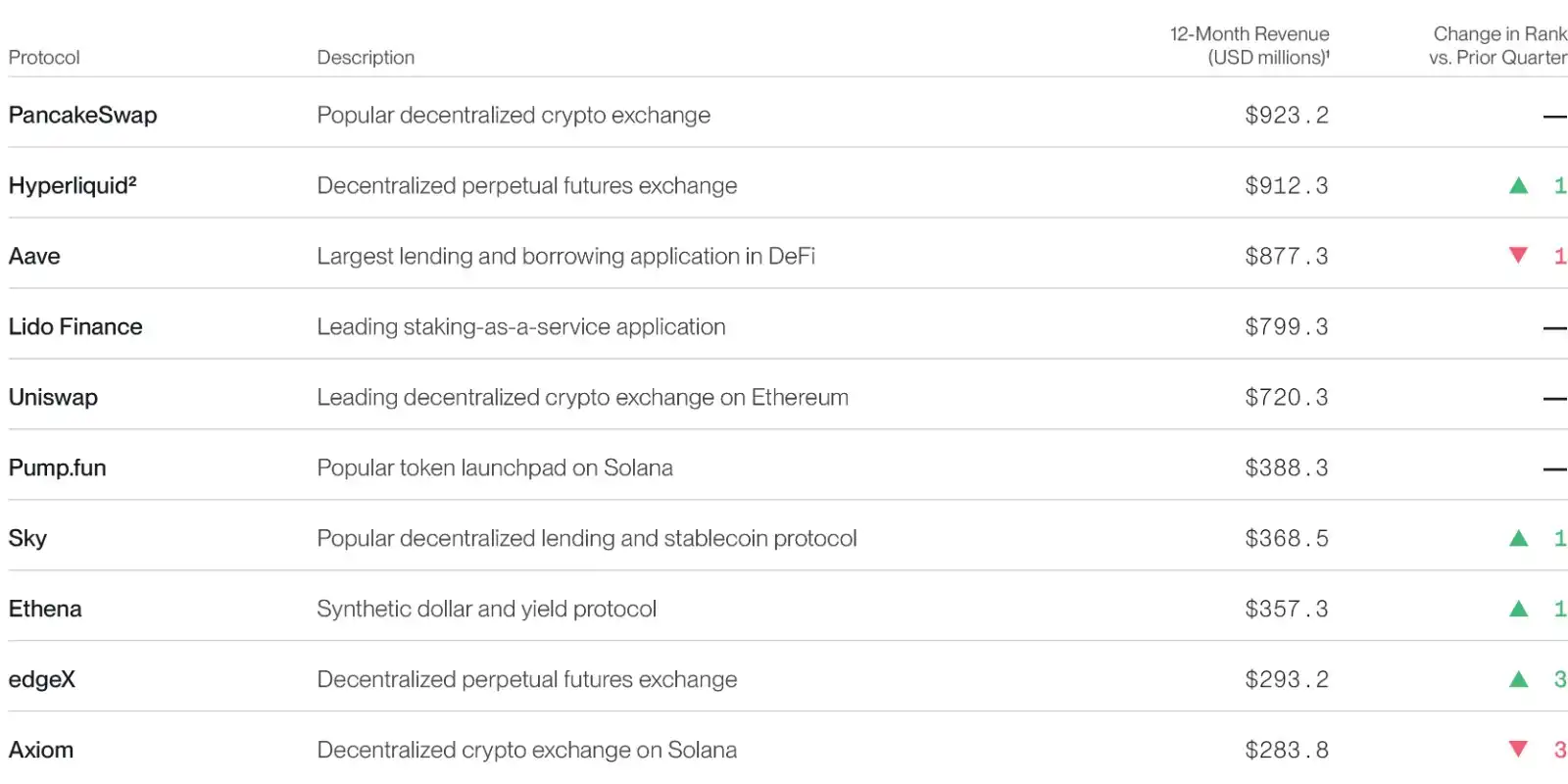

Top crypto apps produced $5.9 billion in revenue

The second chart focused on application-layer revenue. Over the past 12 months, the top 10 crypto applications globally generated a combined $5.9 billion in revenue. PancakeSwap, Hyperliquid and Aave ranked in the top three, with each producing close to $1 billion, the article said.

Rasmussen described these products as real businesses with durable cash flow even during a bear market. Their income comes from trading fees, lending interest and staking yield. Whenever someone argues that crypto has no real fundamentals, he wrote, this is the chart he points to.

The revenue ranking used data from Bitwise and Token Terminal and covered the period from Jan. 1, 2025 to June 30, 2026.

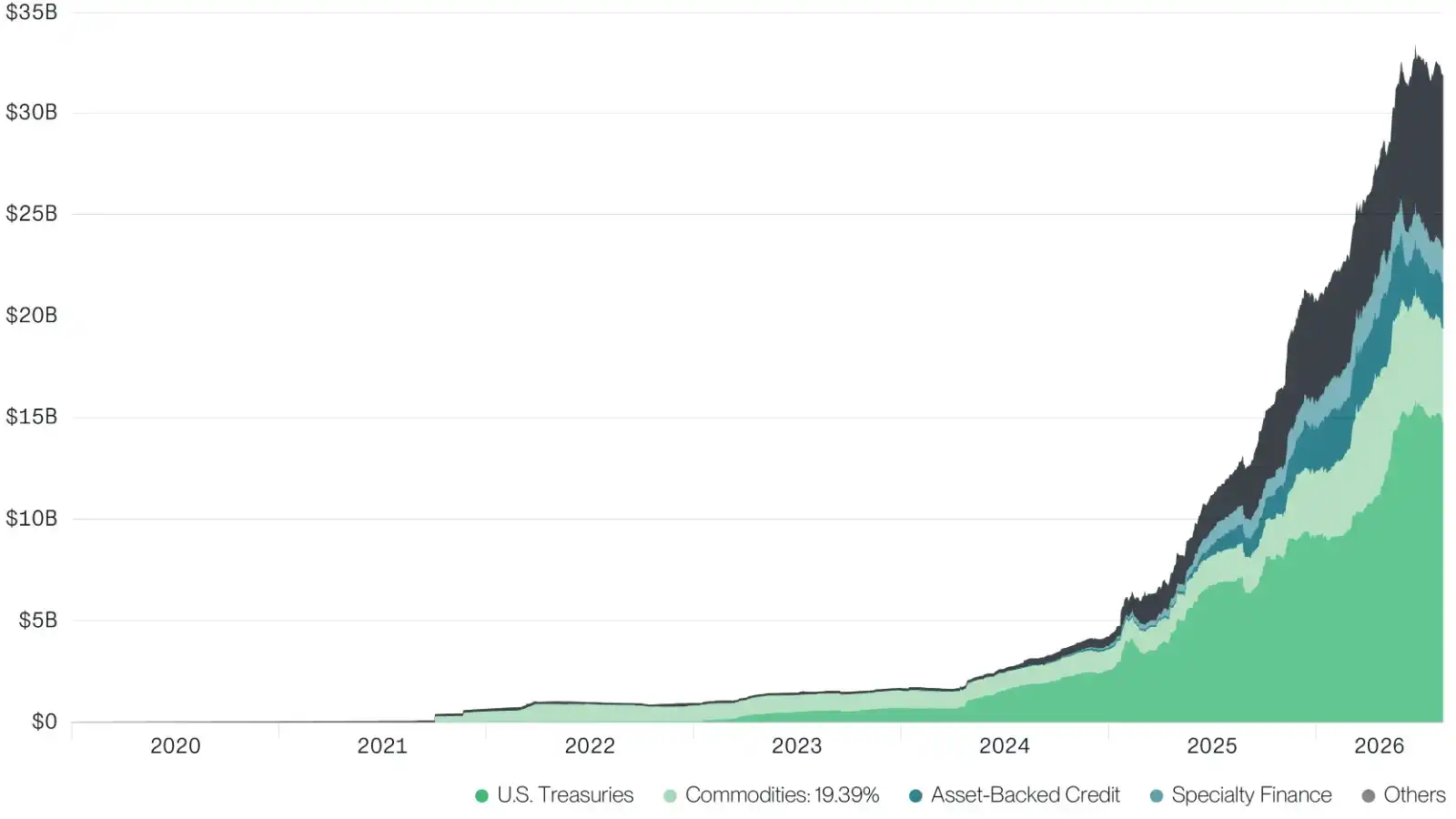

Tokenized real-world assets reached a record $33 billion

The third chart covered real-world assets, or RWA. The article quoted U.S. Treasury Secretary Scott Bessent, who said several weeks earlier that “digital assets, stablecoins, asset tokenization, and new payment systems will together shape the future of the monetary system.”

Rasmussen said that future is already taking shape. In the second quarter, the total value of tokenized real-world assets rose to a record $33 billion. That was up 12% from the previous quarter and 45% year to date. Growth came mainly from tokenized U.S. Treasuries, corporate credit, equities and venture capital fund interests.

He said the chart showed large global asset managers are moving real-world assets onto blockchains at scale, making the trend one to keep watching.

The data came from Bitwise Asset Management and RWA.xyz and covered Jan. 1, 2020 through June 30, 2026.

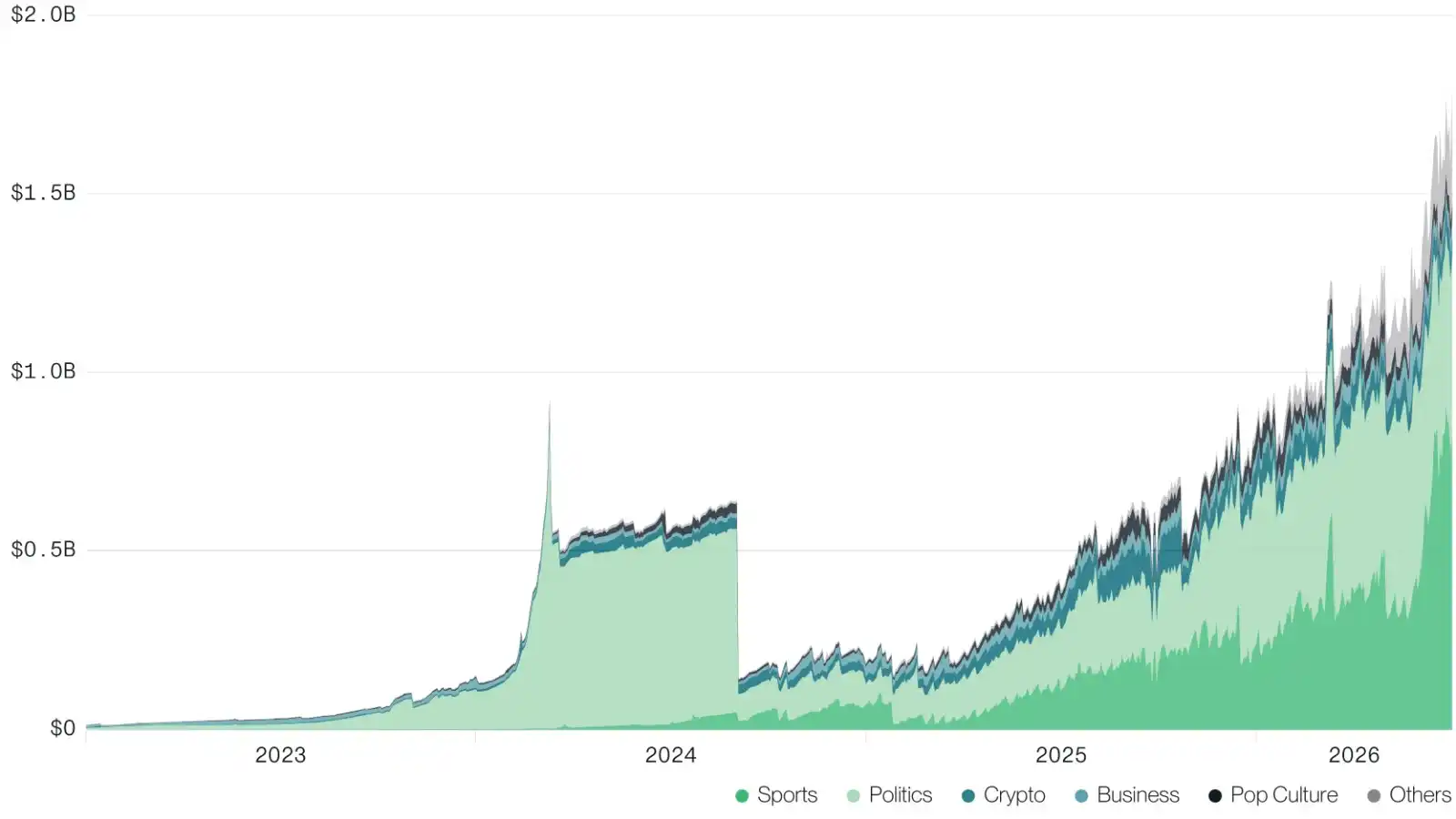

Prediction markets set records in open interest and volume

The fourth chart tracked the growth of prediction markets. Open interest hit a record $1.8 billion in the second quarter, with sports emerging as the main trading category. Quarterly volume also reached a new high at $43 billion.

Using Polymarket as an example, the article said these platforms reveal a less visible side of retail crypto adoption. Millions of users are using crypto-based infrastructure to bet on real-world outcomes, but most of them do not know, or do not care, that blockchain is the technology underneath.

Rasmussen wrote that with the U.S. midterm elections getting closer, he expects prediction market volume and open interest to set fresh records multiple times this year. He also noted that prediction markets entered the public spotlight during the 2024 election cycle, after which the sector tripled in size.

The figures were based on data from Bitwise and Blockworks from Jan. 1, 2023 to June 30, 2026.

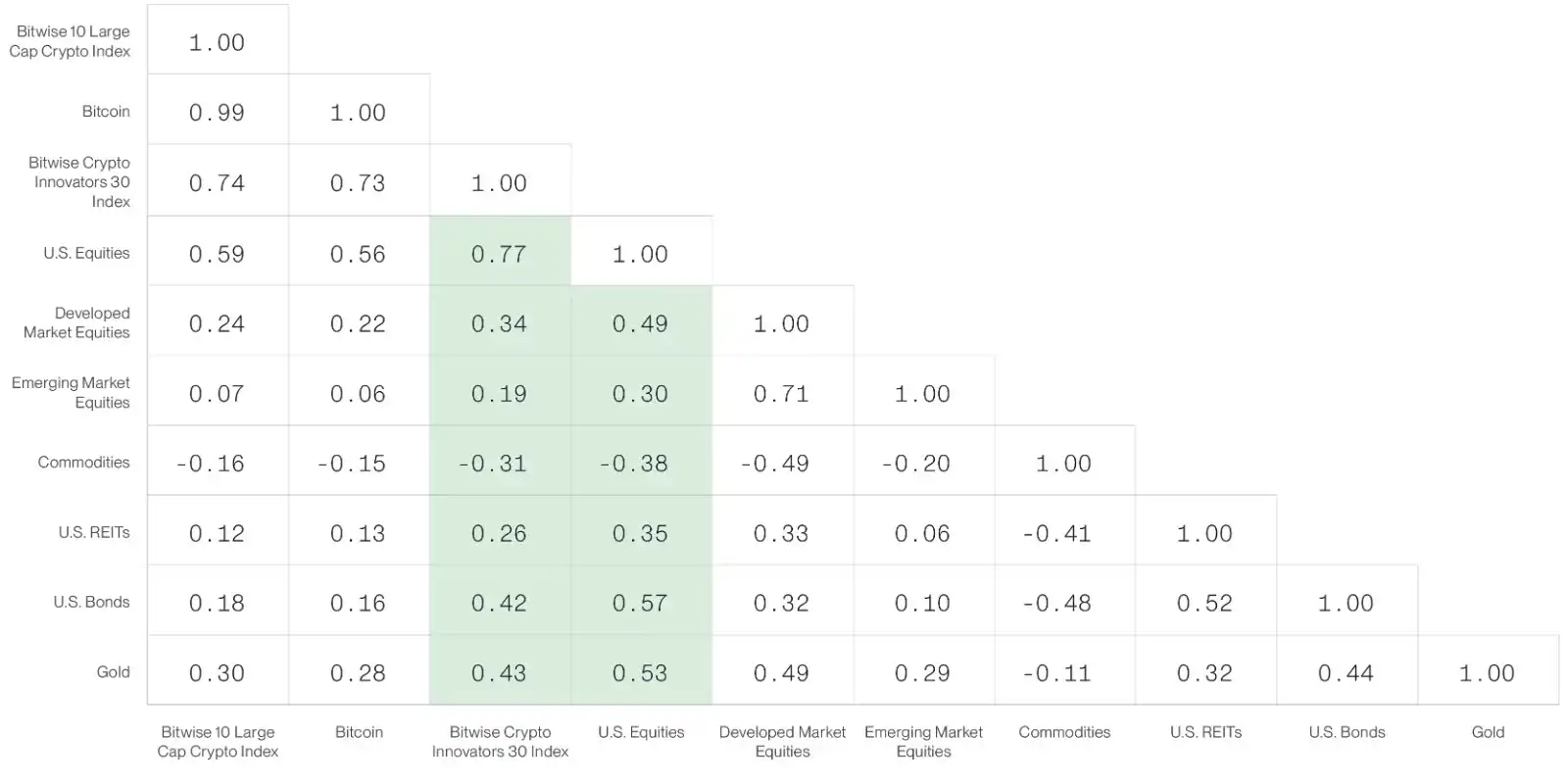

Crypto equities showed low correlation with most major assets

The fifth chart returned to crypto-related stocks. It showed the 90-day rolling correlation between the Bitwise Crypto Innovators 30 Index and other asset classes. Rasmussen said the index had lower correlation than the broader U.S. equity market with most assets, including developed market equities, emerging market equities, U.S. REITs, U.S. Treasuries and gold. Commodities were the only exception, with negative correlation readings.

His summary was simple: in the first half of 2026, crypto equities returned twice as much as the broader U.S. stock market while remaining weakly correlated with most assets in a portfolio. That combination of higher returns and diversification is what makes the segment attractive to institutional investors, he wrote.

This comparison also used data from Bitwise and Bloomberg through June 30, 2026.

Fundamentals kept improving despite weak prices

In the conclusion of the original piece, Rasmussen said the more than 50 charts in the report cannot directly answer the question the market cares about most: whether crypto prices have already bottomed. What the data does show, he said, is that the industry’s fundamentals remain resilient even in a bear market. User activity, business revenue and institutional adoption are still growing.

He described the current stage of the industry as highly worth studying and as part of the foundation for the next bull market.

The piece was written by Ryan Rasmussen, translated by Foresight News, and published by MarsBit.